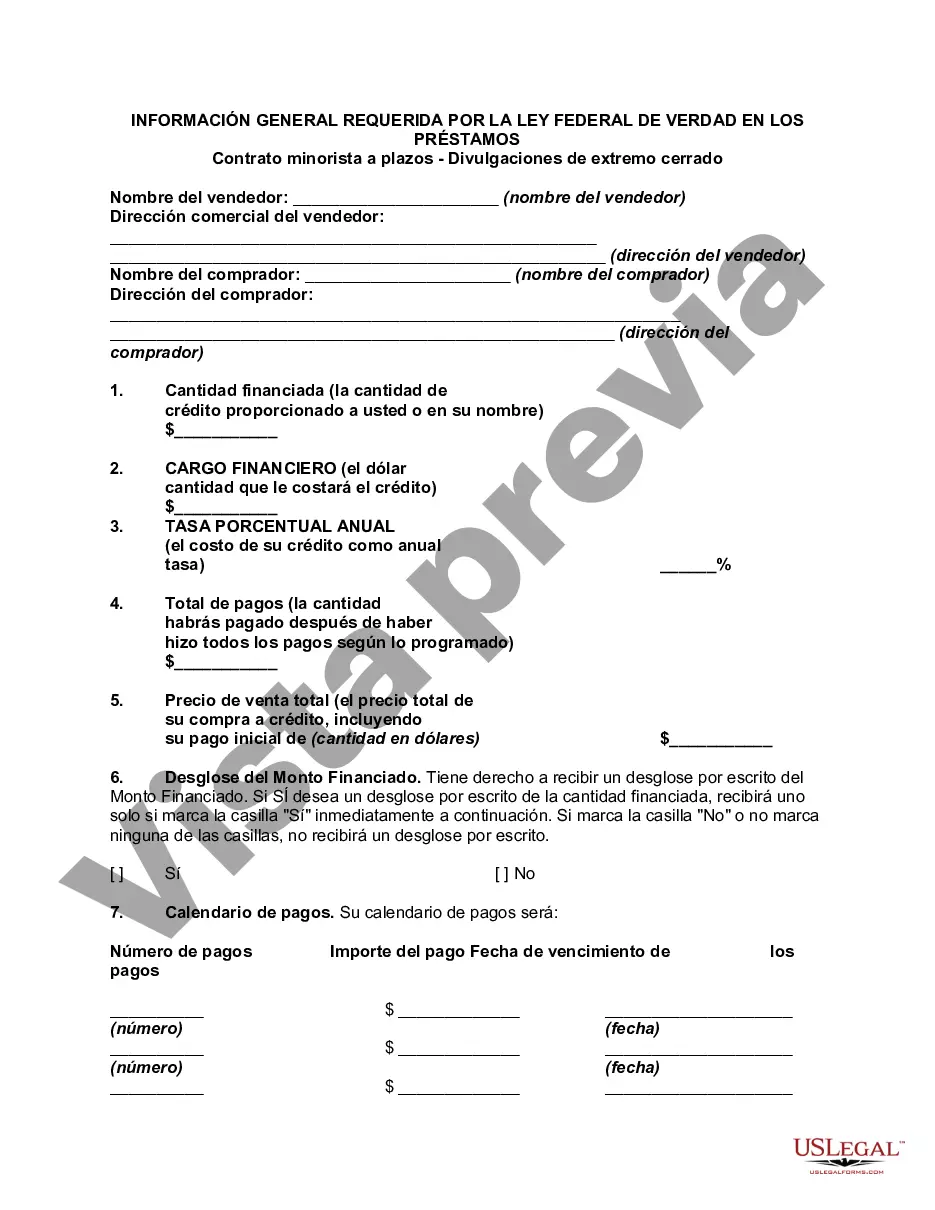

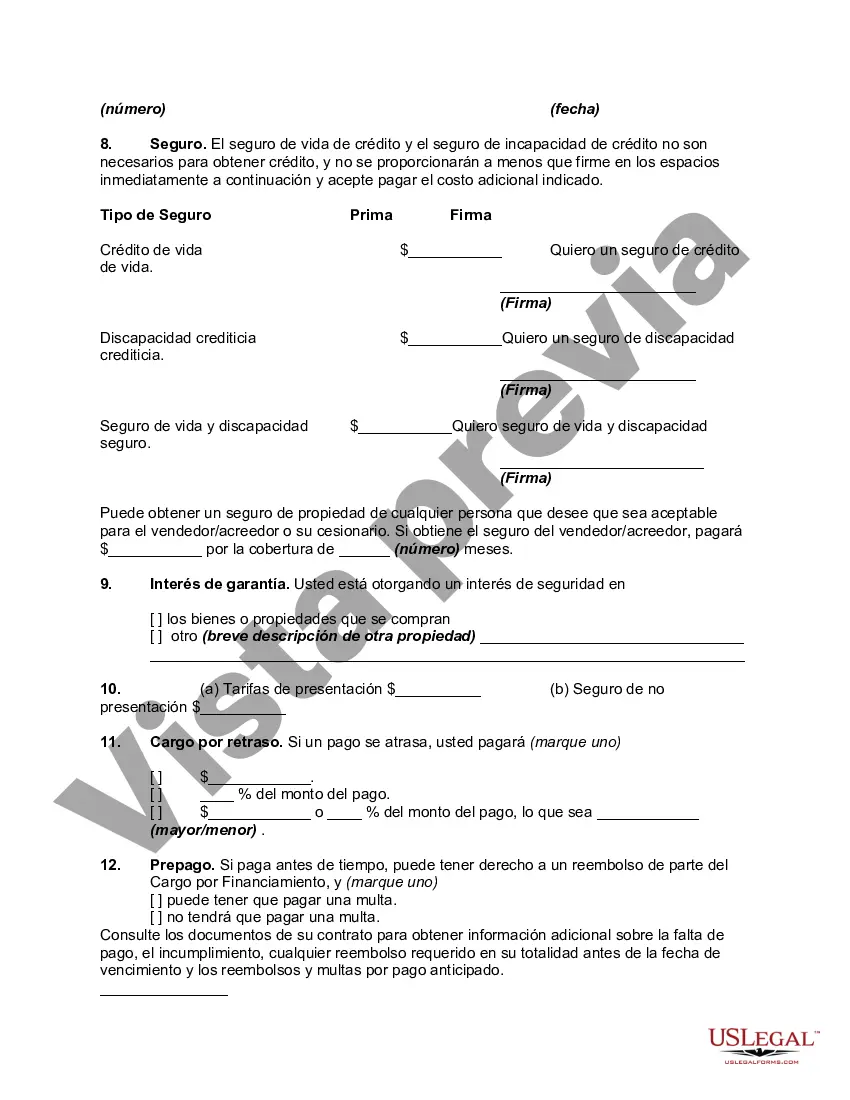

Oakland County, Michigan is a vibrant county located in the southeast part of the state. It is the second-most populous county in Michigan, known for its diverse communities, thriving economy, and picturesque landscapes. This bustling county is home to numerous towns and cities, including the city of Rochester, Farmington Hills, Troy, and Nova. When it comes to financial transactions in Oakland County, it's essential to follow the regulations set forth by the Federal Truth In Lending Act (TILL). Under TILL, various general disclosures are required for retail installment contracts, specifically in closed-end transactions. These disclosures aim to enhance consumer protection by ensuring transparency and full disclosure of loan terms and conditions. Some general disclosures required by the Federal Truth In Lending Act in Oakland County include: 1. Annual Percentage Rate (APR): The APR represents the total cost of credit, expressed as an annual percentage rate. It includes not only the interest rate but also any additional fees or charges associated with the loan. 2. Finance Charges: This disclosure includes the total amount of charges imposed on the transaction, including interest, origination fees, and any other applicable fees. 3. Amount Financed: The amount financed is the actual loan amount that the borrower will receive, after deducting any prepaid finance charges. 4. Total Payments: This disclosure represents the total sum of all payments the borrower will make over the course of the loan term, including principal and interest. 5. Total Sales Price: The total sales price is the sum of the amount financed and the finance charges. It gives the borrower a clear picture of the overall cost of obtaining credit. 6. Payment Schedule: This disclosure outlines the repayment schedule, detailing the number of payments, their due dates, and the amount of each payment. 7. Late Payment Fees: If applicable, this disclosure states the fees charged for late or missed payments. 8. Prepayment: This disclosure informs borrowers whether prepayment penalties apply if they choose to pay off the loan early. 9. Security Interest: If the loan is secured by any collateral, this disclosure clarifies the rights of the lender, including potential repossession or foreclosure. 10. Right to Rescind: For certain types of loans, borrowers may have the right to cancel the contract within a specified timeframe without penalty. This disclosure highlights such rights, if applicable. These general disclosures provide essential information to borrowers in Oakland County, Michigan, ensuring they understand the terms and costs associated with their loans. By adhering to these requirements, lenders uphold the principles of transparency and accountability, promoting fair lending practices and protecting consumers' interests. It is crucial for both lenders and borrowers to familiarize themselves with these disclosures to ensure a smooth and legally compliant lending process.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Oakland Michigan Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Description

How to fill out Oakland Michigan Divulgaciones Generales Requeridas Por La Ley Federal De Veracidad En Los Préstamos - Contrato Minorista A Plazos - Divulgaciones Cerradas?

Laws and regulations in every area vary throughout the country. If you're not an attorney, it's easy to get lost in various norms when it comes to drafting legal documents. To avoid expensive legal assistance when preparing the Oakland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, you need a verified template valid for your county. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's a great solution for professionals and individuals searching for do-it-yourself templates for various life and business occasions. All the documents can be used multiple times: once you purchase a sample, it remains available in your profile for further use. Therefore, if you have an account with a valid subscription, you can simply log in and re-download the Oakland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from the My Forms tab.

For new users, it's necessary to make a couple of more steps to get the Oakland General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures:

- Take a look at the page content to make sure you found the right sample.

- Take advantage of the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to get the document once you find the appropriate one.

- Opt for one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Fill out and sign the document in writing after printing it or do it all electronically.

That's the simplest and most economical way to get up-to-date templates for any legal purposes. Find them all in clicks and keep your documentation in order with the US Legal Forms!