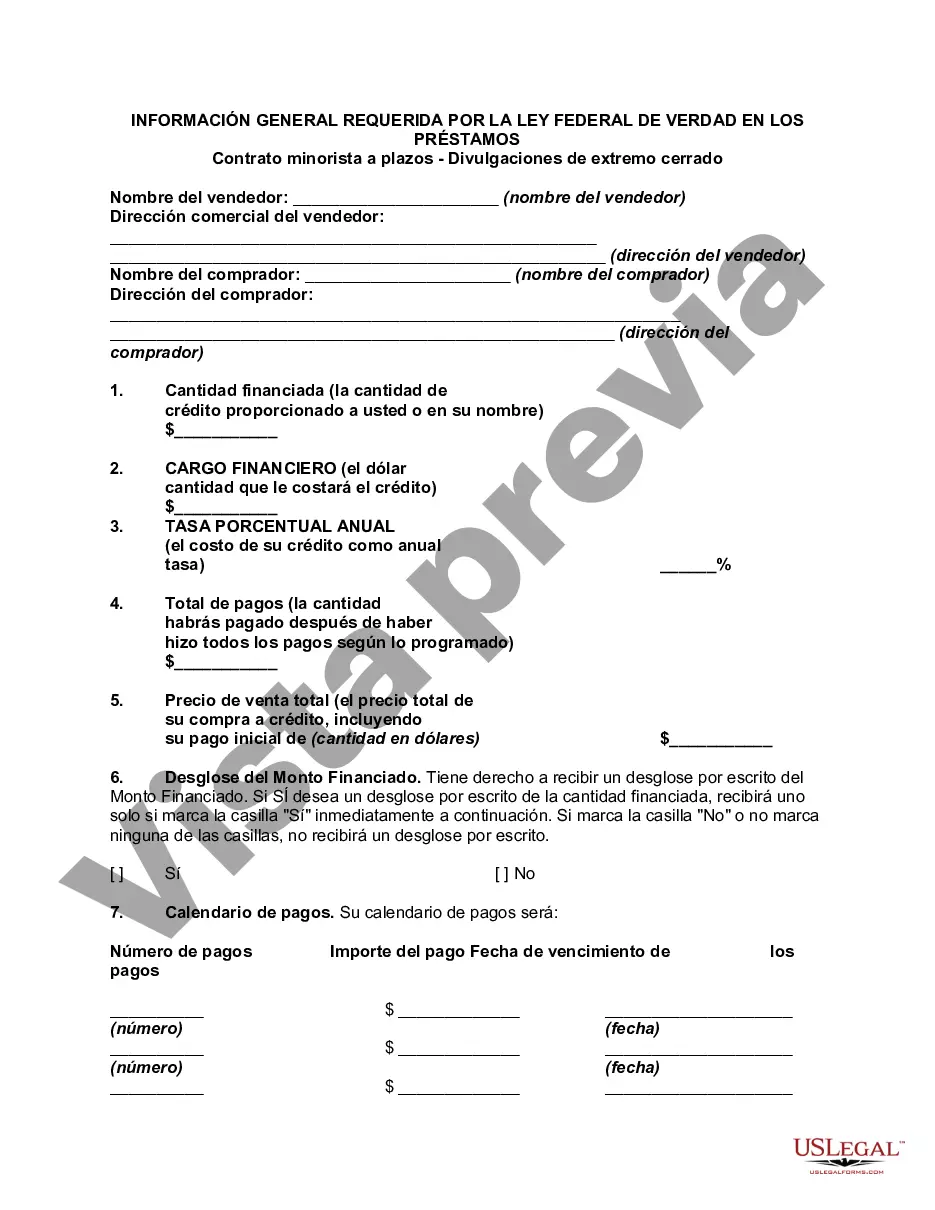

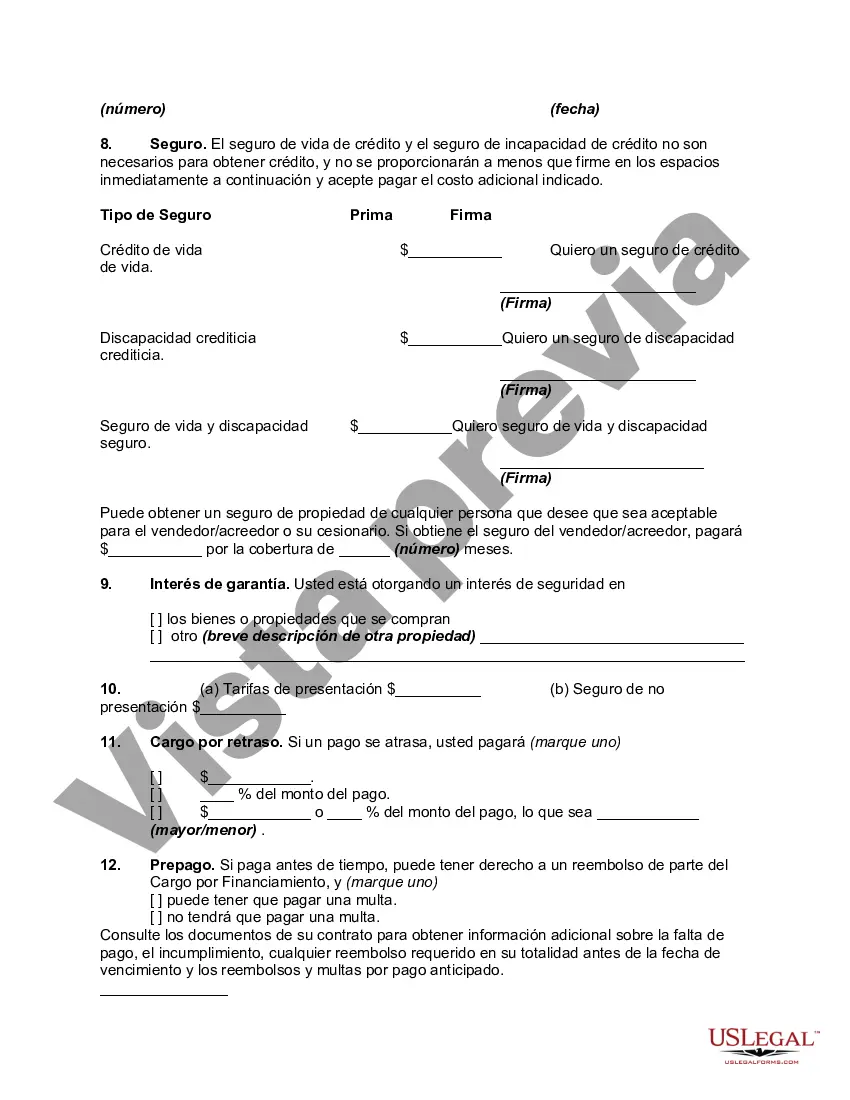

Lima, Arizona General Disclosures Required By The Federal Truth In Lending Act — Retail InstallmenContractac— - Closed End Disclosures When entering into a retail installment contract in Lima, Arizona, it is important to understand the general disclosures required by the Federal Truth In Lending Act (TILL). These disclosures aim to provide consumers with comprehensive information regarding their financial obligations and protect them from deceptive practices. The Federal Truth In Lending Act applies to closed-end credit transactions in Lima, Arizona, meaning loans with specific repayment terms and a fixed amount borrowed. These disclosures must be provided to consumers before the loan is finalized, ensuring they have sufficient time to review and understand the terms. Here are the general disclosures required by the Federal Truth In Lending Act for retail installment contracts in Lima, Arizona: 1. Annual Percentage Rate (APR): The APR represents the total cost of the loan, including the interest rate and any additional fees or finance charges. It allows consumers to compare different loan offers and understand the overall cost of borrowing. 2. Finance Charge: The finance charge encompasses the total amount of interest paid over the loan term, along with any other charges imposed by the lender. 3. Amount Financed: This disclosure provides the total amount borrowed by the consumer. It excludes any prepaid finance charges or other fees that are not part of the principal loan amount. 4. Total Payments: The total payments disclose the overall amount the borrower will pay over the life of the loan, including principal, interest, and any other charges. 5. Payment Schedule: The payment schedule illustrates the number of payments required, their frequency, and the amount due for each installment. It helps consumers understand their repayment obligations and ensures transparency in the borrowing process. 6. Late Payment Charges: Lenders must disclose any potential penalties or fees imposed for late payments. This information encourages borrowers to make payments on time and avoid additional financial burden. 7. Prepayment Penalties: If applicable, any charges associated with early loan repayment should be clearly disclosed to borrowers. This allows consumers to evaluate the cost-effectiveness of paying off their loan before the scheduled term. It is essential for lenders and financing institutions in Lima, Arizona to adhere to these general disclosures required by the Federal Truth In Lending Act. Failure to provide accurate and transparent information may result in legal consequences and financial loss for both borrowers and lenders. In addition to these general disclosures, there may be other specific disclosures required depending on the nature of the retail installment contract. These additional disclosures could include information about insurance coverage, security interest, required down payments, and other relevant terms specific to the loan or purchase agreement. Overall, the Federal Truth In Lending Act safeguards consumers in Lima, Arizona by ensuring they have access to crucial information regarding their financial obligations. By reviewing and understanding these disclosures, borrowers can make informed decisions and avoid potential pitfalls associated with complex loan arrangements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Pima Arizona Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Description

How to fill out Pima Arizona Divulgaciones Generales Requeridas Por La Ley Federal De Veracidad En Los Préstamos - Contrato Minorista A Plazos - Divulgaciones Cerradas?

How much time does it normally take you to draft a legal document? Considering that every state has its laws and regulations for every life sphere, locating a Pima General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures suiting all local requirements can be stressful, and ordering it from a professional lawyer is often pricey. Numerous online services offer the most popular state-specific documents for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most comprehensive online catalog of templates, collected by states and areas of use. Aside from the Pima General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, here you can get any specific form to run your business or personal deeds, complying with your county requirements. Specialists verify all samples for their validity, so you can be certain to prepare your documentation correctly.

Using the service is pretty easy. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the required sample, and download it. You can retain the file in your profile at any moment later on. Otherwise, if you are new to the platform, there will be some extra actions to complete before you obtain your Pima General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another form utilizing the related option in the header.

- Click Buy Now once you’re certain in the chosen file.

- Choose the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Pima General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- Print the sample or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the purchased template, you can find all the samples you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!