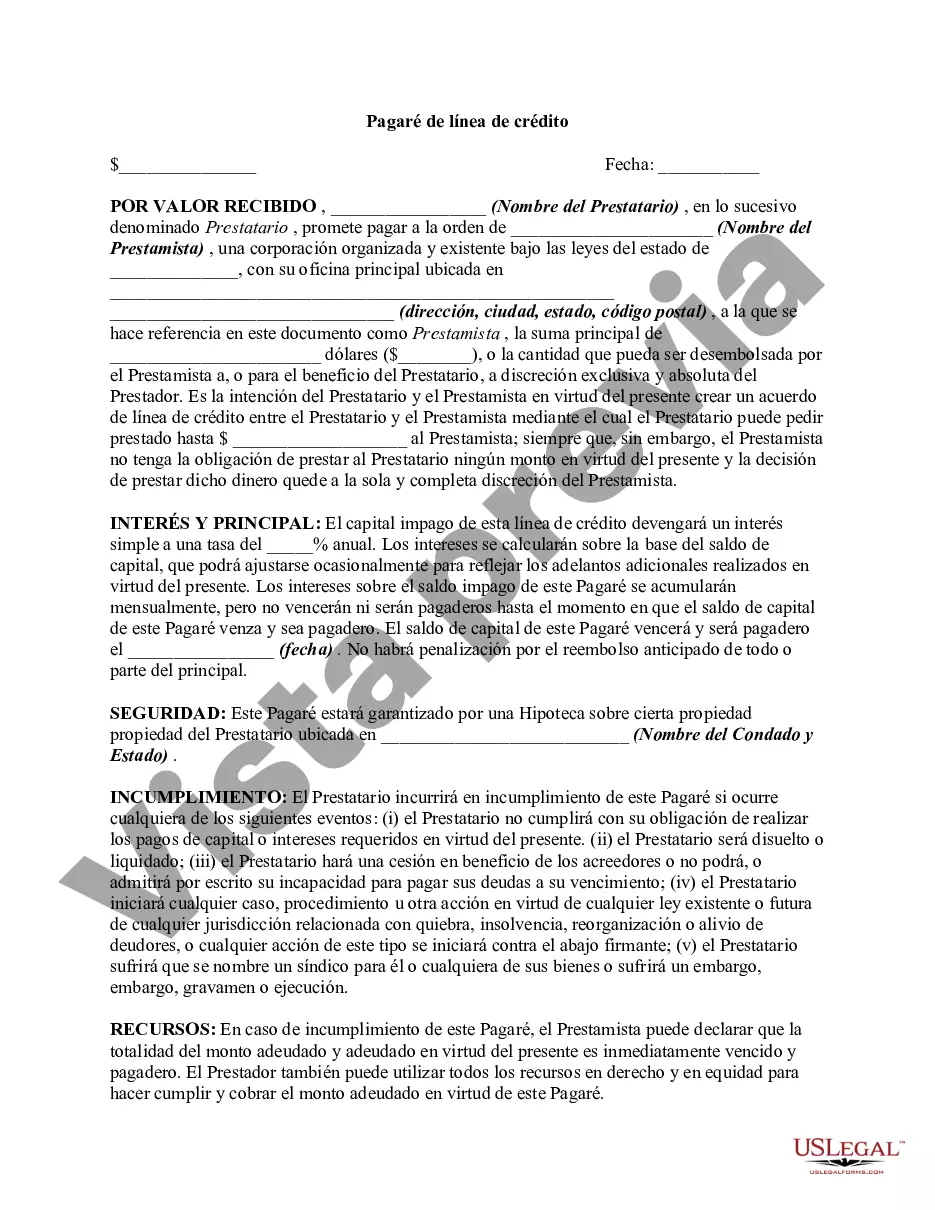

A Line of Credit refers to the maximum borrowing power that a lender extends to a borrower. The borrower may draw required amounts from the fixed amount. Usually, it is a credit source extended to any credit-worthy business by a bank or any financial institution. A line of credit includes cash credit, overdraft, demand loan, export packing credit, term loan, discounting or purchase of commercial bills, etc. The borrower may use the line of credit to overcome liquidity problems. Requisite amounts may be withdrawn from the account as and when required. The borrower pays interest only for the amount withdrawn.

A Cook Illinois Line of Credit Promissory Note is a legal document used in finance and lending agreements. It outlines the terms and conditions of a line of credit provided by Cook Illinois Corporation to a borrower. This promissory note serves as evidence of the borrower's promise to repay the borrowed funds along with any applicable interest and fees. The Cook Illinois Line of Credit Promissory Note typically includes the following information: 1. Parties involved: It identifies Cook Illinois Corporation as the lender and the borrower who is seeking the line of credit. 2. Loan amount: The note specifies the maximum amount of funds that the borrower can draw from the line of credit. 3. Interest rate: It indicates the interest rate that will be charged on any outstanding balances. 4. Repayment terms: The note outlines how and when the borrower is required to repay the borrowed funds. It typically includes details such as repayment schedule, minimum monthly payments, and any applicable late payment penalties. 5. Draw period: This term refers to the period during which the borrower can access funds from the line of credit. It specifies the start and end date of the draw period. 6. Maturity date: The note mentions the date by which the borrower must repay the outstanding balance in full, or convert it into another form of loan if applicable. 7. Security and collateral: In some cases, the Cook Illinois Line of Credit Promissory Note may require the borrower to provide specific assets or collateral as security for the line of credit. Different types of Cook Illinois Line of Credit Promissory Notes may include variations in terms and conditions to cater to specific borrowing needs. Some common types include: 1. Revolving line of credit promissory note: Allows the borrower to borrow, repay, and borrow again within the specified draw period. 2. Non-revolving line of credit promissory note: Provides a one-time borrowing opportunity, wherein once the borrower repays the borrowed funds, they cannot draw additional funds from the line. 3. Secured line of credit promissory note: Requires the borrower to pledge specific assets or provide collateral to secure the line of credit. 4. Unsecured line of credit promissory note: Does not require any specific assets or collateral to secure the line of credit but may have higher interest rates to compensate for the increased risk. It's important for both the lender and the borrower to carefully review and understand the terms and conditions outlined in the Cook Illinois Line of Credit Promissory Note to ensure mutual agreement and compliance with applicable laws and regulations.A Cook Illinois Line of Credit Promissory Note is a legal document used in finance and lending agreements. It outlines the terms and conditions of a line of credit provided by Cook Illinois Corporation to a borrower. This promissory note serves as evidence of the borrower's promise to repay the borrowed funds along with any applicable interest and fees. The Cook Illinois Line of Credit Promissory Note typically includes the following information: 1. Parties involved: It identifies Cook Illinois Corporation as the lender and the borrower who is seeking the line of credit. 2. Loan amount: The note specifies the maximum amount of funds that the borrower can draw from the line of credit. 3. Interest rate: It indicates the interest rate that will be charged on any outstanding balances. 4. Repayment terms: The note outlines how and when the borrower is required to repay the borrowed funds. It typically includes details such as repayment schedule, minimum monthly payments, and any applicable late payment penalties. 5. Draw period: This term refers to the period during which the borrower can access funds from the line of credit. It specifies the start and end date of the draw period. 6. Maturity date: The note mentions the date by which the borrower must repay the outstanding balance in full, or convert it into another form of loan if applicable. 7. Security and collateral: In some cases, the Cook Illinois Line of Credit Promissory Note may require the borrower to provide specific assets or collateral as security for the line of credit. Different types of Cook Illinois Line of Credit Promissory Notes may include variations in terms and conditions to cater to specific borrowing needs. Some common types include: 1. Revolving line of credit promissory note: Allows the borrower to borrow, repay, and borrow again within the specified draw period. 2. Non-revolving line of credit promissory note: Provides a one-time borrowing opportunity, wherein once the borrower repays the borrowed funds, they cannot draw additional funds from the line. 3. Secured line of credit promissory note: Requires the borrower to pledge specific assets or provide collateral to secure the line of credit. 4. Unsecured line of credit promissory note: Does not require any specific assets or collateral to secure the line of credit but may have higher interest rates to compensate for the increased risk. It's important for both the lender and the borrower to carefully review and understand the terms and conditions outlined in the Cook Illinois Line of Credit Promissory Note to ensure mutual agreement and compliance with applicable laws and regulations.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.