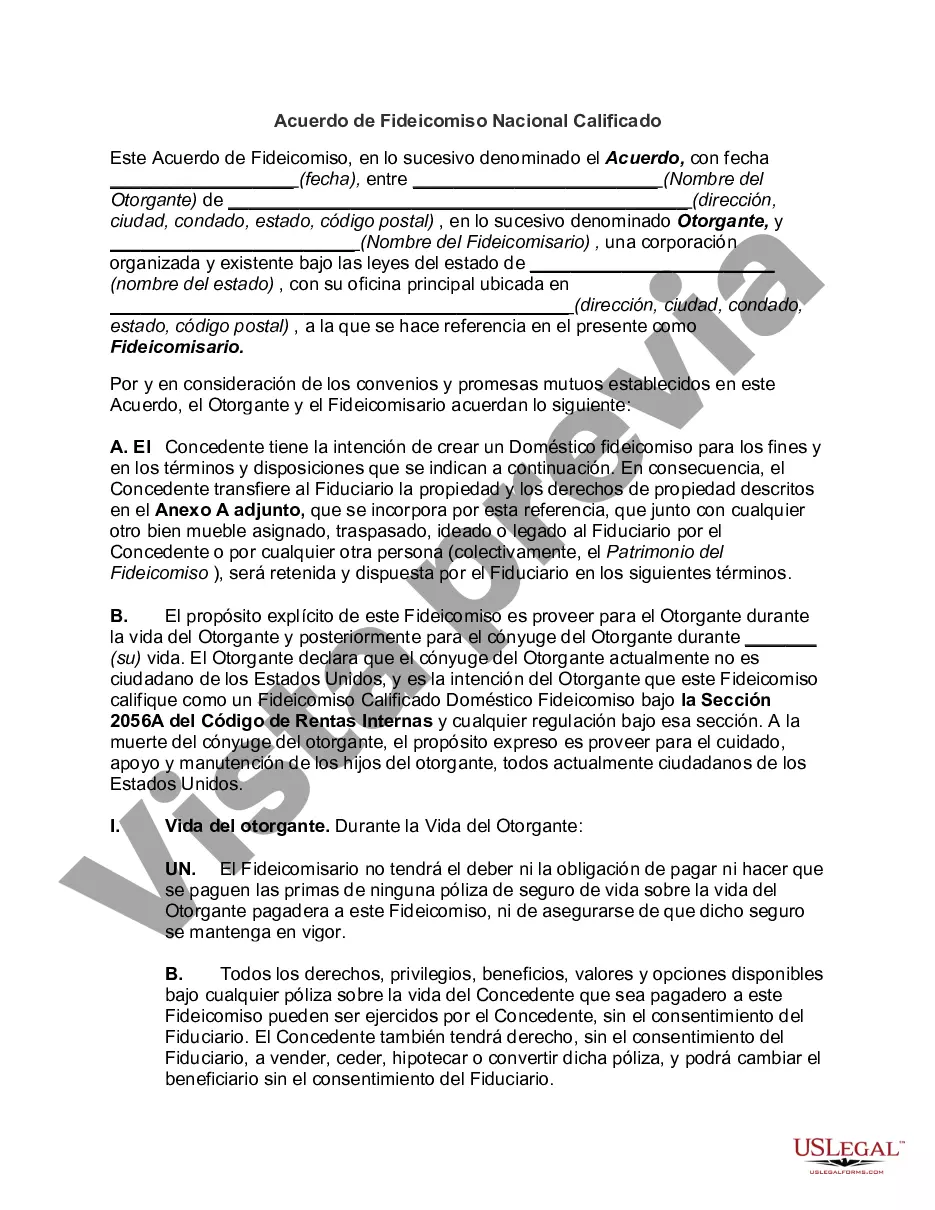

The Harris Texas Qualified Domestic Trust Agreement, commonly referred to as a DOT, is a legal arrangement that allows non-U.S. citizen surviving spouses to qualify for the marital deduction, thereby deferring estate taxes until the surviving spouse's death. The DOT is governed by the Internal Revenue Code Section 2056A and has specific requirements that must be met to ensure compliance. With the Harris Texas Qualified Domestic Trust Agreement, the non-U.S. citizen surviving spouse becomes the beneficiary of the trust, and the assets are held in trust until their death. It serves as a means to protect the interests of the U.S. government by postponing the estate tax liability. Under this arrangement, the Harris Texas DOT must satisfy certain conditions. Firstly, it requires a U.S. citizen or domestic trust to act as a trustee, responsible for overseeing the administration of the DOT. This trustee ensures compliance with applicable tax regulations and takes necessary actions to fulfill the trust's obligations. Additionally, the DOT must contain provisions that restrict distributions, allowing only income or a limited amount of principal distributions to the surviving non-U.S. citizen spouse. The objective here is to preserve the estate tax until the surviving spouse's subsequent passing. Moreover, the DOT must submit an annual information return to the Internal Revenue Service (IRS) to ensure proper tax reporting and compliance. The trustee is responsible for preparing and filing this return, disclosing specific details about the trust, its assets, income, distributions, and beneficiaries. There are different types of Harris Texas Qualified Domestic Trust Agreements based on the unique circumstances and needs of individuals. These include: 1. General DOT: This is the most common type of DOT, where the surviving spouse receives income distributions and can access a limited portion of the principal if necessary. 2. Estate Tax Deferral DOT: This type of DOT allows for a full deferral of estate taxes until both the death of the non-U.S. citizen spouse and any other triggering events occur, such as the sale of certain assets. 3. Portability DOT: This form of DOT is established when the couple wants to make use of the portability provision, which allows the surviving spouse to use the deceased spouse's unused estate tax exemption. In conclusion, the Harris Texas Qualified Domestic Trust Agreement (DOT) is a crucial estate planning tool for non-U.S. citizen surviving spouses to delay the payment of estate taxes. It necessitates compliance with specific requirements outlined in the Internal Revenue Code Section 2056A. Various types of Dots exist, offering flexibility based on individual circumstances, such as the general DOT, estate tax deferral DOT, and portability DOT. Understanding these distinctions is essential when implementing an appropriate DOT strategy.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Harris Texas Acuerdo de Fideicomiso Nacional Calificado - Qualified Domestic Trust Agreement

Description

How to fill out Harris Texas Acuerdo De Fideicomiso Nacional Calificado?

A document routine always accompanies any legal activity you make. Opening a business, applying or accepting a job offer, transferring property, and many other life scenarios require you prepare formal paperwork that differs from state to state. That's why having it all collected in one place is so helpful.

US Legal Forms is the biggest online library of up-to-date federal and state-specific legal forms. On this platform, you can easily locate and get a document for any individual or business objective utilized in your county, including the Harris Qualified Domestic Trust Agreement.

Locating forms on the platform is remarkably straightforward. If you already have a subscription to our library, log in to your account, find the sample through the search field, and click Download to save it on your device. After that, the Harris Qualified Domestic Trust Agreement will be available for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, follow this quick guideline to get the Harris Qualified Domestic Trust Agreement:

- Make sure you have opened the proper page with your local form.

- Make use of the Preview mode (if available) and browse through the sample.

- Read the description (if any) to ensure the form satisfies your needs.

- Look for another document via the search option if the sample doesn't fit you.

- Click Buy Now once you locate the required template.

- Select the suitable subscription plan, then log in or create an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and save the Harris Qualified Domestic Trust Agreement on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the simplest and most trustworthy way to obtain legal documents. All the templates available in our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs effectively with the US Legal Forms!