Contra Costa California Partnership Agreement for Startup is a legal document that outlines the terms and conditions of a partnership between two or more individuals or entities who are joining forces to start a new business venture in Contra Costa County, California. This partnership agreement sets out the rights, obligations, and responsibilities of each partner involved in the startup. It covers various aspects of the partnership, including the distribution of profits and losses, decision-making processes, management duties, and dispute resolution mechanisms. Keywords: 1. Contra Costa County: Refers to the specific geographical location where the partnership is being formed. Contra Costa County is located in Northern California and offers a favorable business environment for startups. 2. Partnership Agreement: Signifies the legal contract that governs the partnership between the parties involved in the startup. It establishes the framework for collaboration and operation of the business. 3. Startup: Denotes a newly established business venture with innovative ideas, products, or services. Startups are characterized by high growth potential and often require partnerships to combine resources and expertise. 4. Legal document: Emphasizes the importance of this agreement as a legally binding contract that protects the rights and interests of all partners involved in the startup. Types of Contra Costa California Partnership Agreements for Startup: 1. General Partnership Agreement: This is the most common type of partnership agreement for startups. It establishes a partnership where all partners have equal rights and responsibilities, and profits and losses are shared equally. 2. Limited Partnership Agreement: This type of agreement distinguishes between general partners and limited partners. General partners have unlimited liability and manage the business, while limited partners have limited liability and invest capital without participating in management decisions. 3. Limited Liability Partnership (LLP) Agreement: LLP agreements provide partners with limited liability protection, allowing them to avoid personal responsibility for the partnership's debts and obligations. This type of agreement is suitable for startups that want to limit individual partner liability. 4. Joint Venture Agreement: In some cases, startups may enter into a joint venture agreement with another business entity to pursue a specific project or venture. This agreement establishes a partnership between the startup and the other entity, outlining the terms, objectives, and obligations of each party. In conclusion, the Contra Costa California Partnership Agreement for Startup is a crucial legal document that sets the terms and conditions for a partnership venture in Contra Costa County. It defines the rights, obligations, and responsibilities of the partners involved and ensures a solid foundation for the startup's success. The agreement can take different forms, including general partnership, limited partnership, limited liability partnership, or joint venture, depending on the specific needs and goals of the startup.

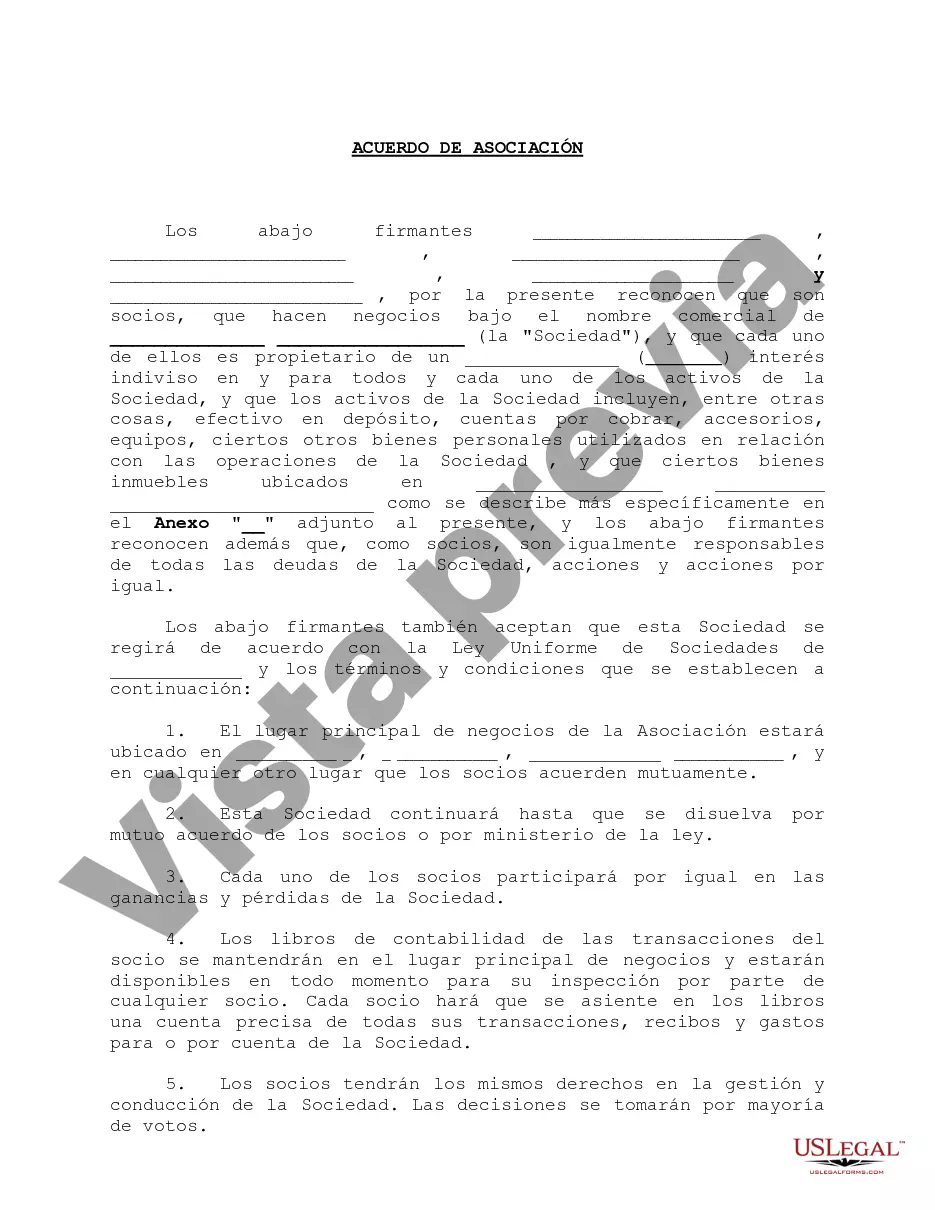

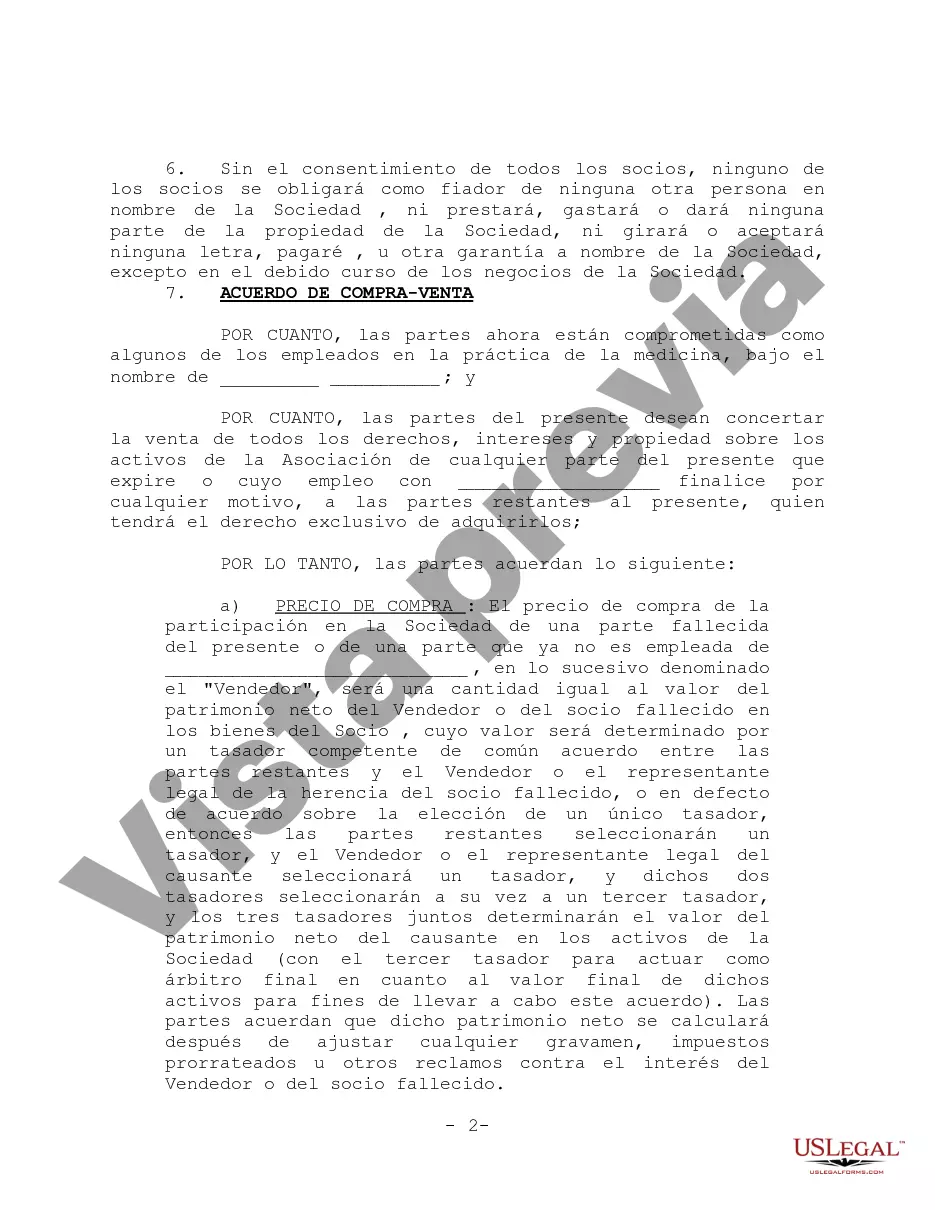

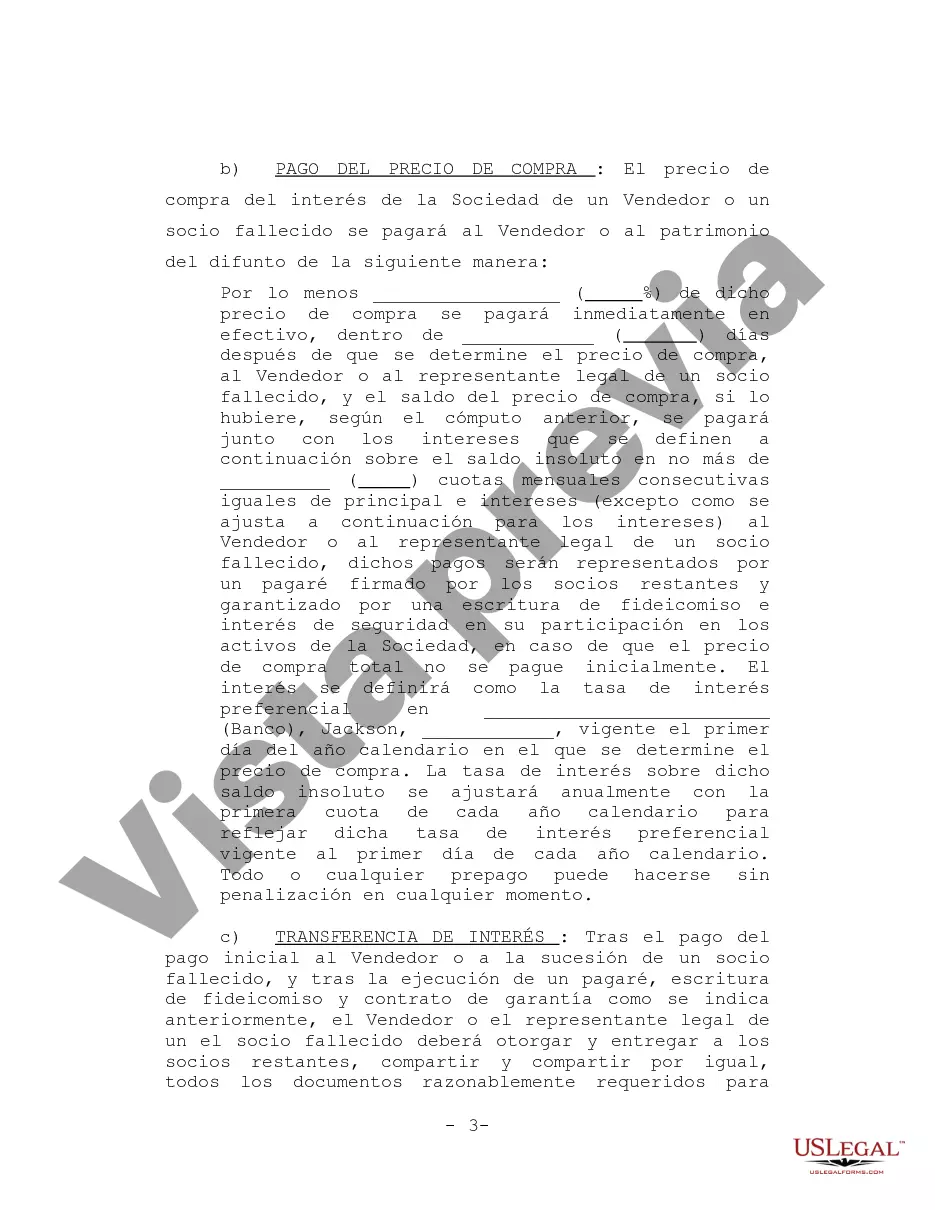

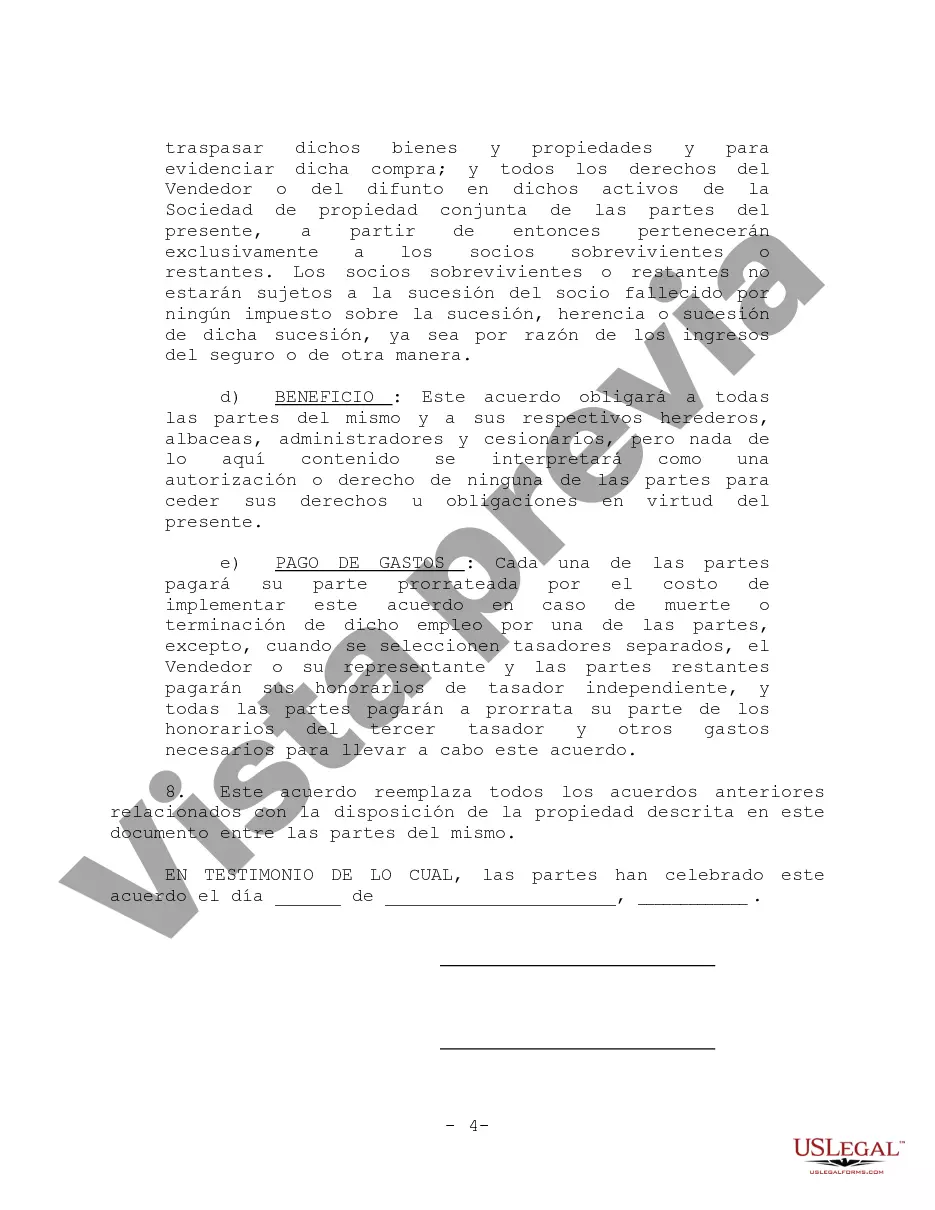

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Contra Costa California Acuerdo de Asociación para Startup - Partnership Agreement for Startup

Description

How to fill out Contra Costa California Acuerdo De Asociación Para Startup?

Draftwing forms, like Contra Costa Partnership Agreement for Startup, to take care of your legal affairs is a difficult and time-consumming process. Many cases require an attorney’s participation, which also makes this task expensive. However, you can take your legal issues into your own hands and take care of them yourself. US Legal Forms is here to the rescue. Our website features more than 85,000 legal forms created for different cases and life circumstances. We ensure each form is compliant with the laws of each state, so you don’t have to be concerned about potential legal pitfalls compliance-wise.

If you're already aware of our website and have a subscription with US, you know how easy it is to get the Contra Costa Partnership Agreement for Startup template. Simply log in to your account, download the form, and customize it to your needs. Have you lost your form? No worries. You can get it in the My Forms folder in your account - on desktop or mobile.

The onboarding process of new customers is just as straightforward! Here’s what you need to do before getting Contra Costa Partnership Agreement for Startup:

- Make sure that your form is specific to your state/county since the rules for creating legal documents may differ from one state another.

- Learn more about the form by previewing it or reading a quick description. If the Contra Costa Partnership Agreement for Startup isn’t something you were looking for, then take advantage of the search bar in the header to find another one.

- Sign in or create an account to begin utilizing our website and get the document.

- Everything looks great on your side? Click the Buy now button and select the subscription plan.

- Select the payment gateway and enter your payment details.

- Your template is ready to go. You can try and download it.

It’s an easy task to find and purchase the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive library. Subscribe to it now if you want to check what other perks you can get with US Legal Forms!