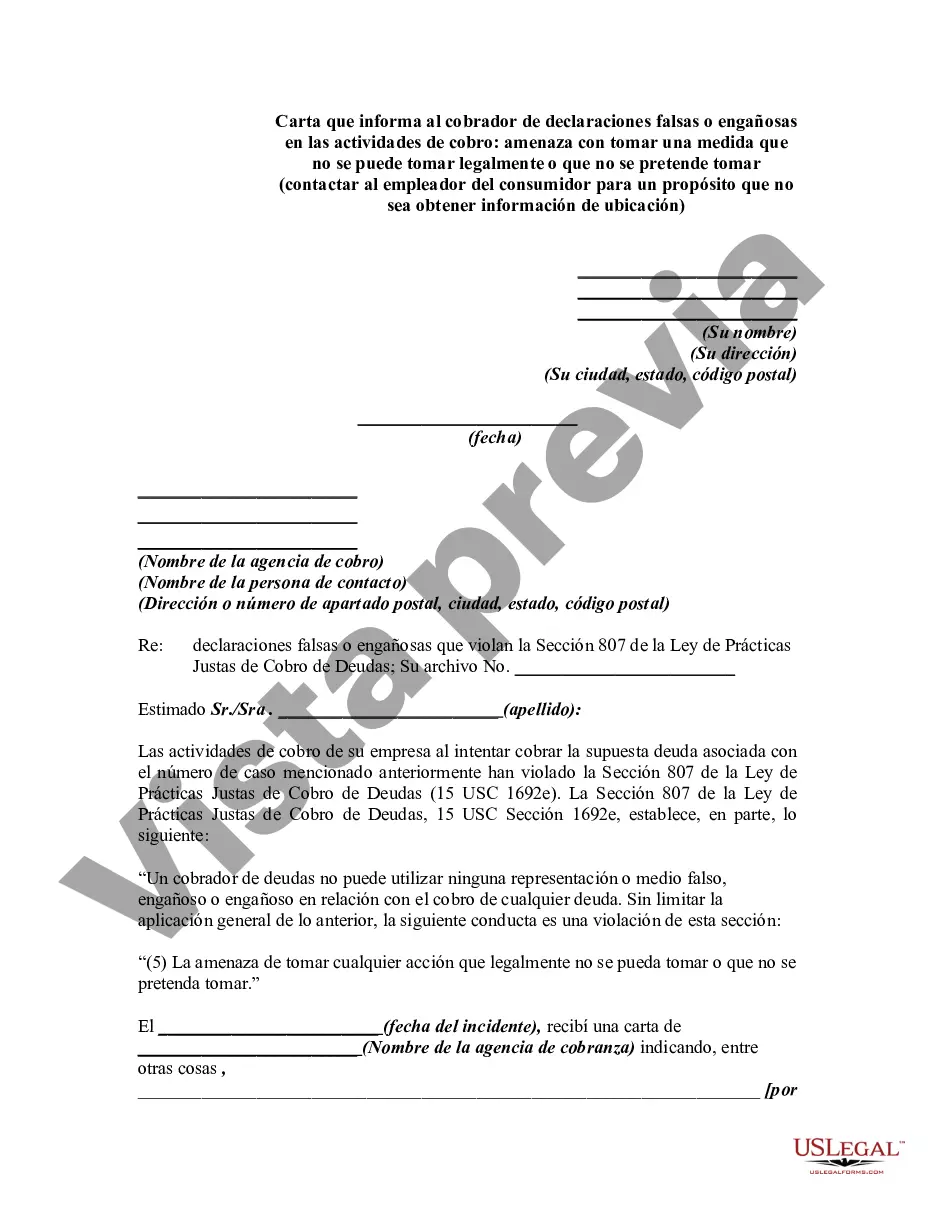

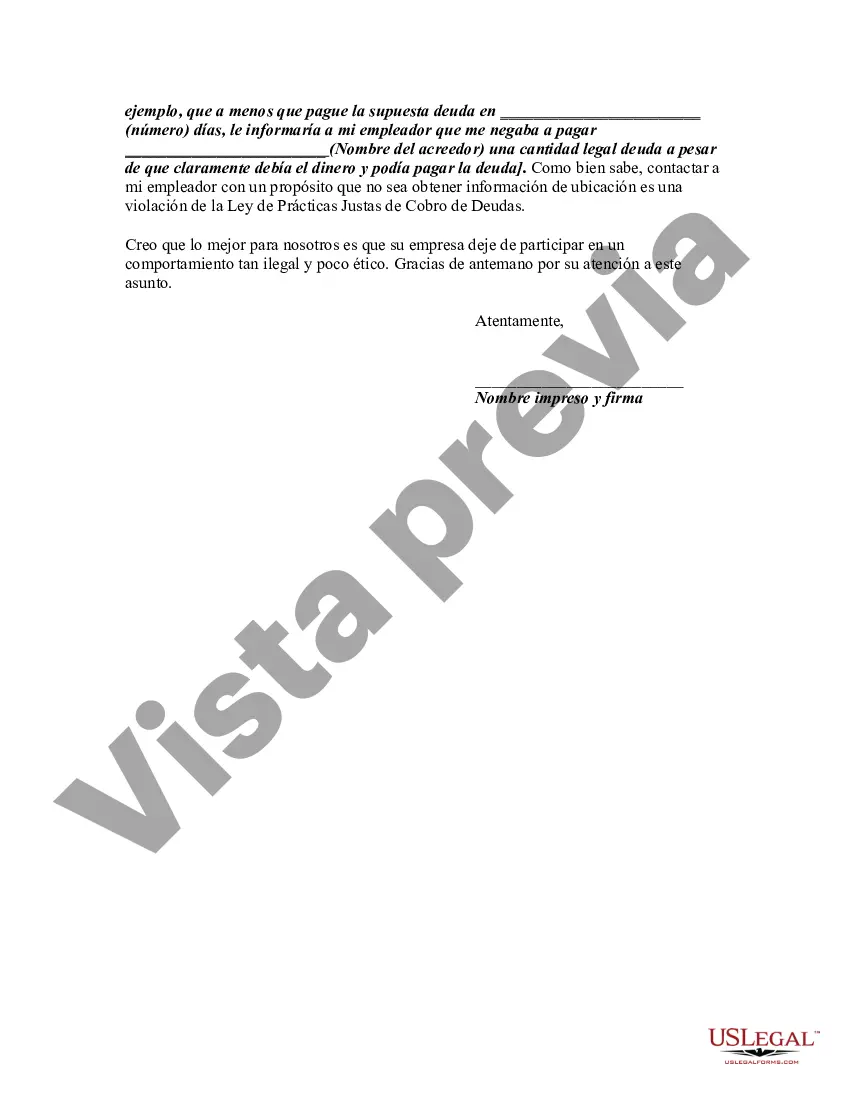

Section 807 of the Fair Debt Collection Practices Act, 15 U.S.C. Section 1692e, provides, in part, as follows: "A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of any debt. Without limiting the general application of the foregoing, the following conduct is a violation of this section:

"(5) The threat to take any action that cannot legally be taken or that is not intended to be taken."

It is a violation of the Fair Debt Collection Practices Act to contact a consumer debtor's employer for a purpose other than to obtain location information.

Title: Know Your Rights: Cook Illinois Letter to Safeguard Against False Debt Collection Practices — Contacting Consumer's Employer Introduction: In today's world, debt collection practices have become increasingly regulated to protect consumers from abusive and deceptive tactics. The Cook Illinois Letter serves as an essential tool to inform debt collectors about false or misleading misrepresentations in collection activities, specifically focusing on threatening to take illegal actions or actions not intended to be taken, such as contacting the consumer's employer. In this article, we will discuss the importance of this letter in safeguarding your rights as a consumer and shed light on various types of false or misleading practices employed by debt collectors. 1. Description of Cook Illinois Letter: The Cook Illinois Letter is a formal correspondence intended to inform debt collectors of their inaccurate or misleading representation during the debt collection process. It provides a detailed account of the collector's actions, outlining specific instances where they have threatened to take illegal actions or actions they have no intention of carrying out. 2. Threatening Actions That Cannot Legally be Taken: Debt collectors are prohibited from making false threats to coerce consumers into paying their debts. The Cook Illinois Letter addresses these instances, such as threatening to: a) File a lawsuit without legal grounds: If a debt collector threatens legal action that they cannot legally pursue due to expired statute of limitations or lack of supporting evidence, it constitutes a violation of the Fair Debt Collection Practices Act (FD CPA). b) Wage garnishment without a court order: Debt collectors cannot threaten to garnish wages without obtaining a court judgment. The Cook Illinois Letter acknowledges such unjust threats and aims to rectify the situation. c) Arrest or imprisonment: It is illegal for debt collectors to threaten consumers with arrest or imprisonment for unpaid debts. The Cook Illinois Letter highlights the unlawfulness of these threats. 3. Actions Not Intended to be Taken: Unscrupulous debt collectors may employ tactics that they have no intention of carrying out. The Cook Illinois Letter addresses the issue of debt collectors contacting consumers' employers falsely, encompassing the following scenarios: a) Misrepresentation of employment verification: In some instances, debt collectors may claim to be conducting employment verification to intimidate the consumer or pressure them into paying. The Cook Illinois Letter emphasizes the deceitfulness of such actions. b) Disclosure of debt to employer: Debt collectors may threaten to contact the consumer's employer regarding their outstanding debt, which is a violation of privacy and can harm the consumer's professional reputation. The Cook Illinois Letter notifies the debt collector of the illegality of this action. c) False threats of job loss: A debt collector may falsely imply that they have the power to jeopardize the consumer's employment by misrepresenting their ability to report the debt or influence the employer's decision. The Cook Illinois Letter aims to correct these misconceptions. Conclusion: The Cook Illinois Letter serves as a vital tool for consumers who have encountered false or misleading debt collection practices, particularly those involving unlawful threats or deceptive contact with their employers. By raising awareness about these illegal actions and informing debt collectors of their misconduct, the Cook Illinois Letter enables consumers to assert their rights, hold debt collectors accountable, and seek appropriate remedies under the law.Title: Know Your Rights: Cook Illinois Letter to Safeguard Against False Debt Collection Practices — Contacting Consumer's Employer Introduction: In today's world, debt collection practices have become increasingly regulated to protect consumers from abusive and deceptive tactics. The Cook Illinois Letter serves as an essential tool to inform debt collectors about false or misleading misrepresentations in collection activities, specifically focusing on threatening to take illegal actions or actions not intended to be taken, such as contacting the consumer's employer. In this article, we will discuss the importance of this letter in safeguarding your rights as a consumer and shed light on various types of false or misleading practices employed by debt collectors. 1. Description of Cook Illinois Letter: The Cook Illinois Letter is a formal correspondence intended to inform debt collectors of their inaccurate or misleading representation during the debt collection process. It provides a detailed account of the collector's actions, outlining specific instances where they have threatened to take illegal actions or actions they have no intention of carrying out. 2. Threatening Actions That Cannot Legally be Taken: Debt collectors are prohibited from making false threats to coerce consumers into paying their debts. The Cook Illinois Letter addresses these instances, such as threatening to: a) File a lawsuit without legal grounds: If a debt collector threatens legal action that they cannot legally pursue due to expired statute of limitations or lack of supporting evidence, it constitutes a violation of the Fair Debt Collection Practices Act (FD CPA). b) Wage garnishment without a court order: Debt collectors cannot threaten to garnish wages without obtaining a court judgment. The Cook Illinois Letter acknowledges such unjust threats and aims to rectify the situation. c) Arrest or imprisonment: It is illegal for debt collectors to threaten consumers with arrest or imprisonment for unpaid debts. The Cook Illinois Letter highlights the unlawfulness of these threats. 3. Actions Not Intended to be Taken: Unscrupulous debt collectors may employ tactics that they have no intention of carrying out. The Cook Illinois Letter addresses the issue of debt collectors contacting consumers' employers falsely, encompassing the following scenarios: a) Misrepresentation of employment verification: In some instances, debt collectors may claim to be conducting employment verification to intimidate the consumer or pressure them into paying. The Cook Illinois Letter emphasizes the deceitfulness of such actions. b) Disclosure of debt to employer: Debt collectors may threaten to contact the consumer's employer regarding their outstanding debt, which is a violation of privacy and can harm the consumer's professional reputation. The Cook Illinois Letter notifies the debt collector of the illegality of this action. c) False threats of job loss: A debt collector may falsely imply that they have the power to jeopardize the consumer's employment by misrepresenting their ability to report the debt or influence the employer's decision. The Cook Illinois Letter aims to correct these misconceptions. Conclusion: The Cook Illinois Letter serves as a vital tool for consumers who have encountered false or misleading debt collection practices, particularly those involving unlawful threats or deceptive contact with their employers. By raising awareness about these illegal actions and informing debt collectors of their misconduct, the Cook Illinois Letter enables consumers to assert their rights, hold debt collectors accountable, and seek appropriate remedies under the law.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.