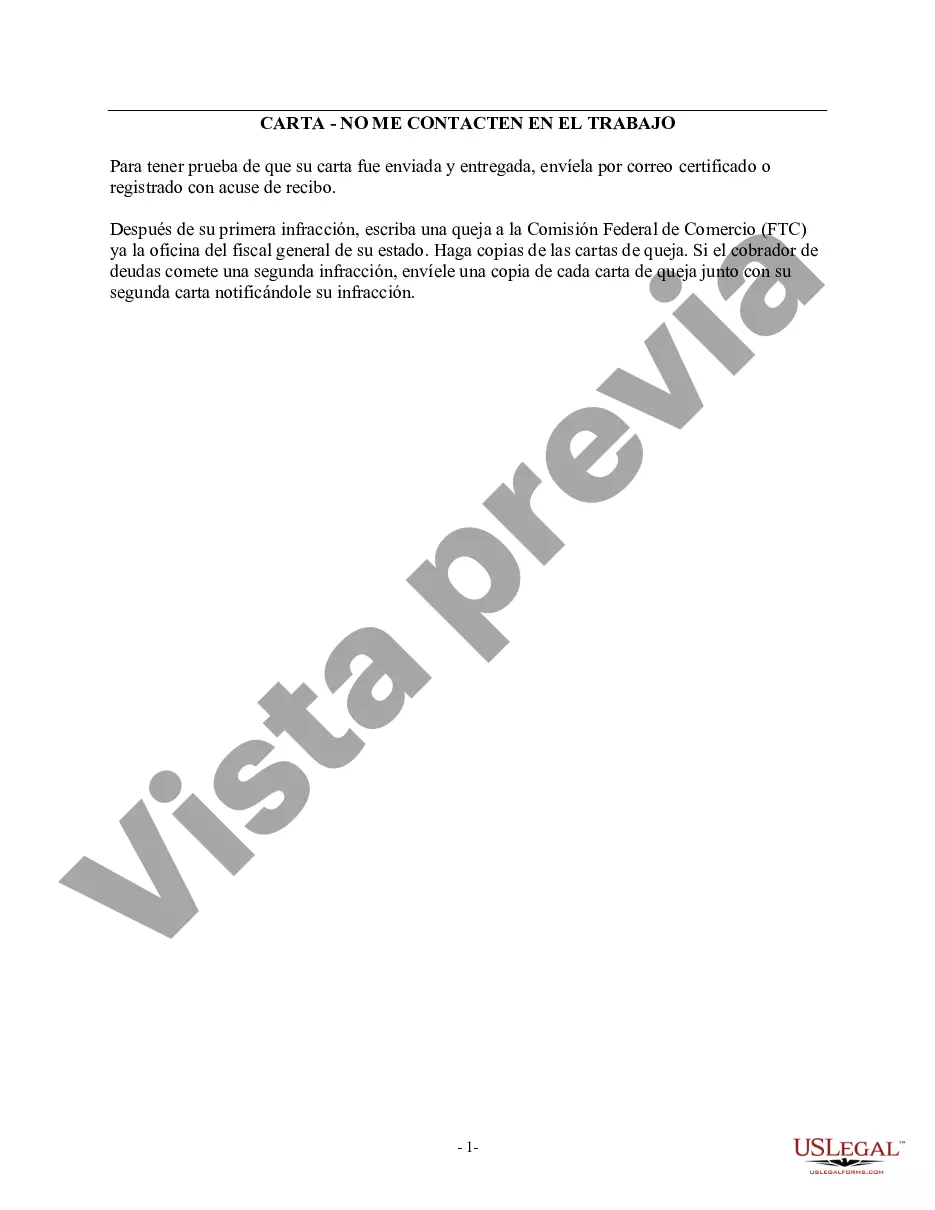

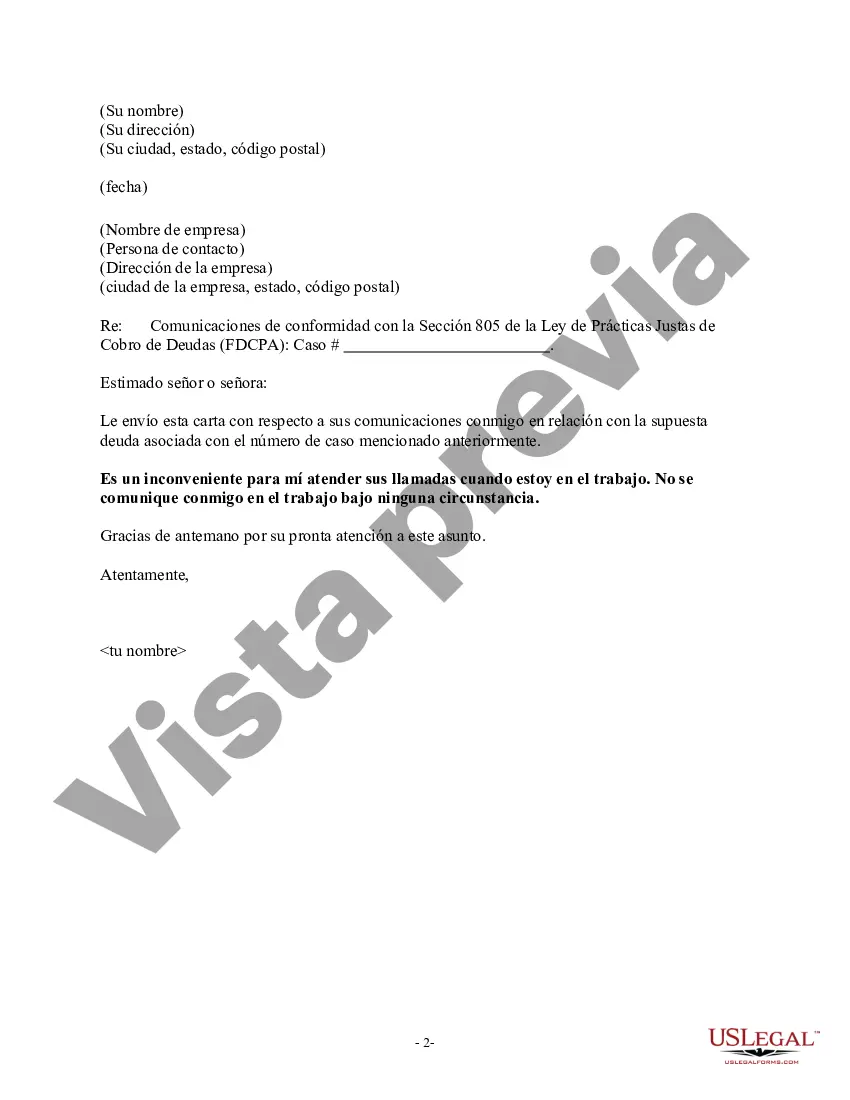

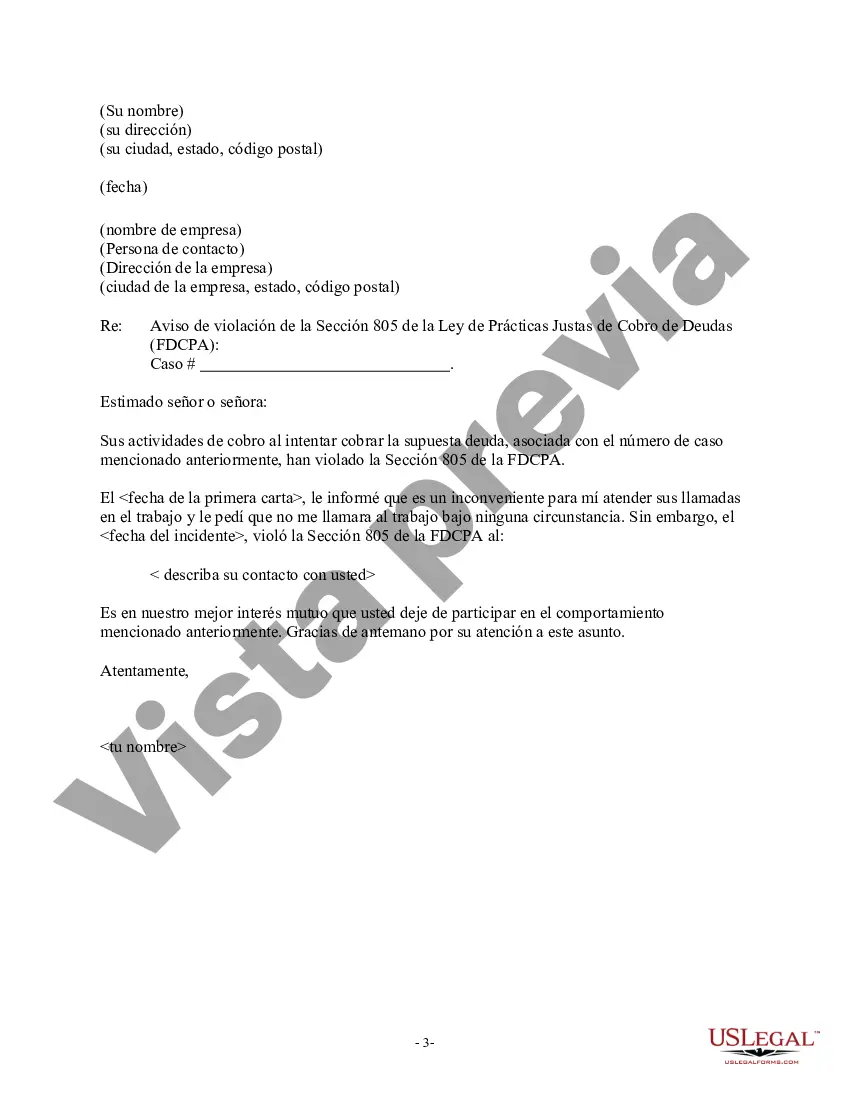

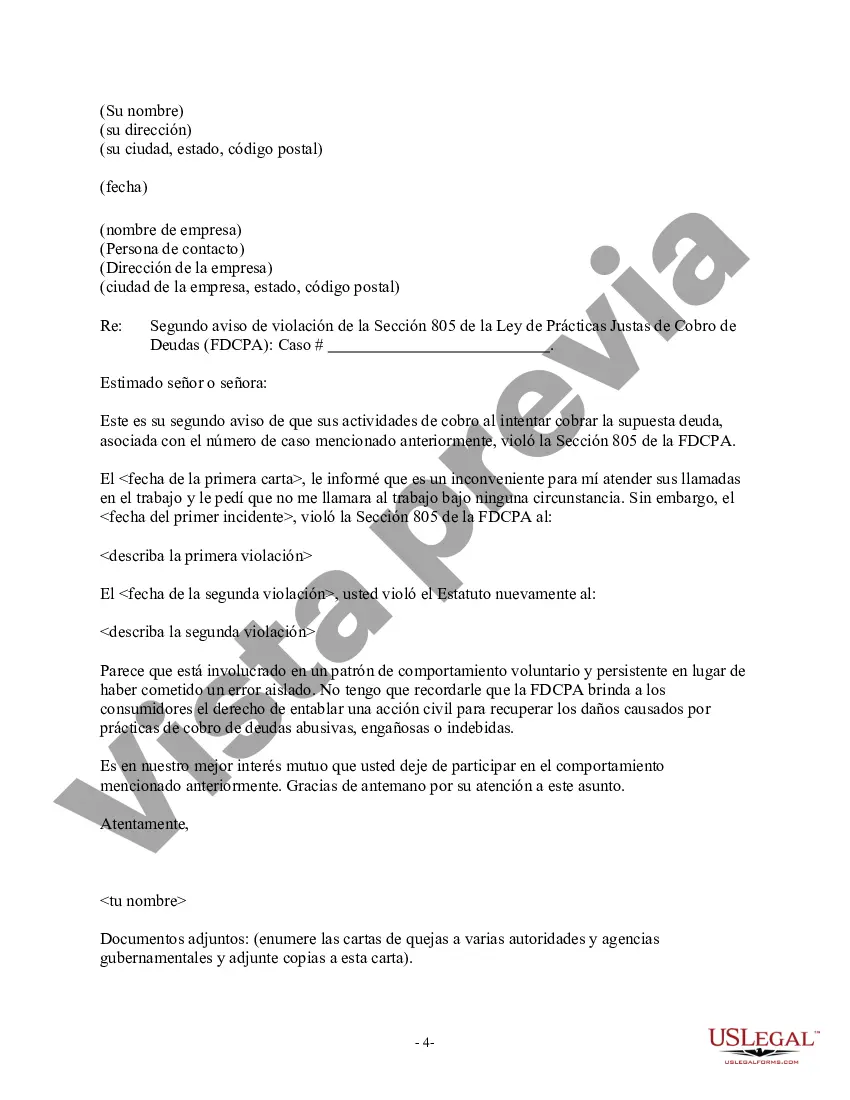

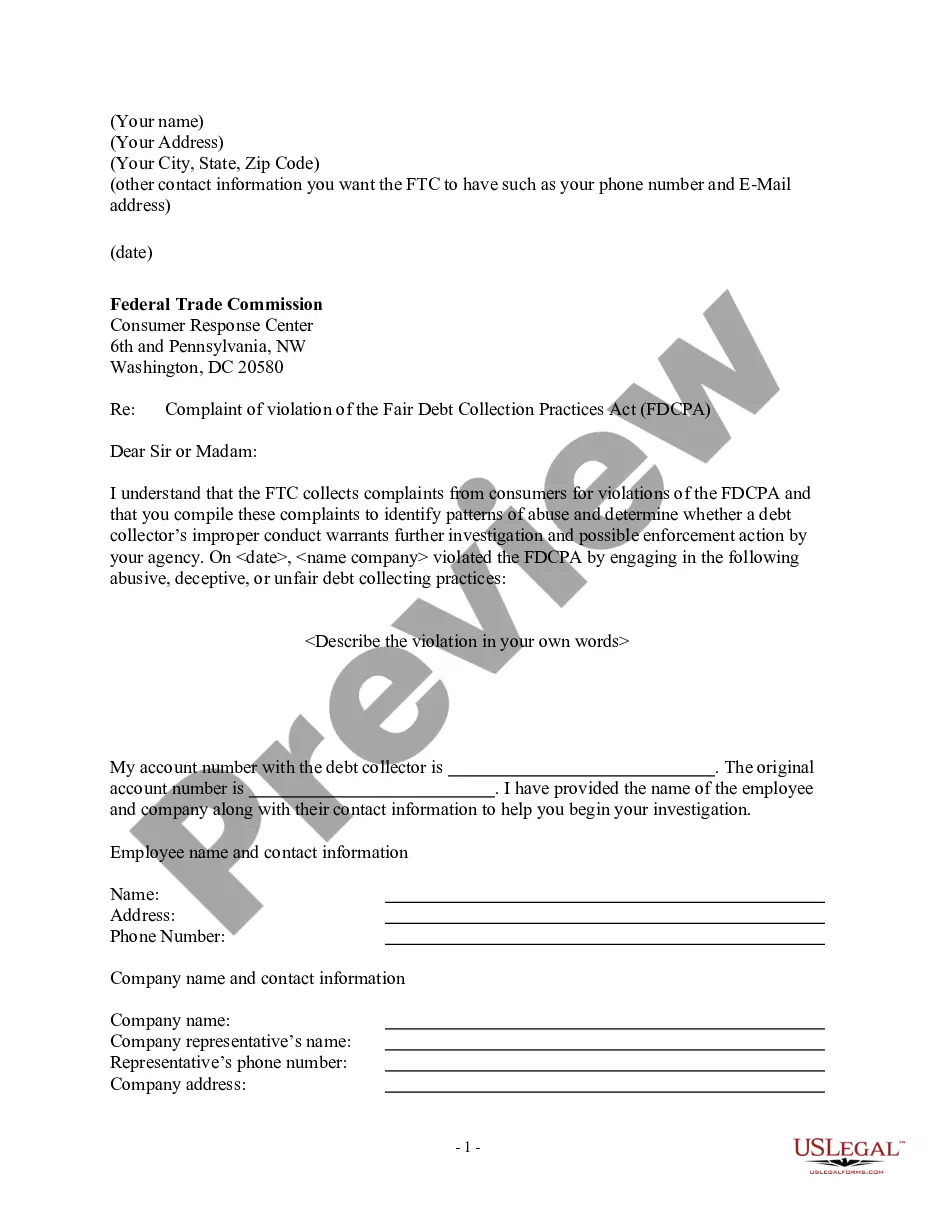

Cook Illinois Notice of Violation of Fair Debt Act — Improper Contact at Work is a legal document that addresses a specific violation of the Fair Debt Collection Practices Act (FD CPA) by Cook Illinois. The FD CPA is a federal law that regulates the practices of debt collectors and ensures that consumers are treated fairly and protected from harassment. In this particular violation, Cook Illinois has been found guilty of engaging in improper contact with a debtor at their workplace. Under the FD CPA, debt collectors are prohibited from contacting debtors at their place of employment if they know or have reason to know that the debtor's employer prohibits such communication. The Cook Illinois Notice of Violation of Fair Debt Act — Improper Contact at Work serves as a formal notification to Cook Illinois, alerting them to the violation and demanding immediate cessation of any further contact with the debtor at their workplace. The purpose of this notice is to hold Cook Illinois accountable for their breach of the FD CPA and to protect the rights of the debtor. It is important to note that there may be different types of Cook Illinois Notice of Violation of Fair Debt Act — Improper Contact at Work, depending on the specific circumstances of the violation. These variations may include instances where Cook Illinois made repeated calls to the debtor's workplace, made threats or disclosed private financial information to the debtor's coworkers, or persisted in contacting the debtor even after being informed of the employer's prohibition on such communication. By issuing a Cook Illinois Notice of Violation of Fair Debt Act — Improper Contact at Work, the debtor is seeking to halt any further violation of their rights as protected by the FD CPA. Additionally, this notice may also serve as a precursor to potential legal action against Cook Illinois for their improper conduct.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Cook Illinois Aviso de violación de la Ley de deuda justa: contacto inadecuado en el trabajo - Notice of Violation of Fair Debt Act - Improper Contact at Work

Description

How to fill out Cook Illinois Aviso De Violación De La Ley De Deuda Justa: Contacto Inadecuado En El Trabajo?

How much time does it normally take you to draft a legal document? Considering that every state has its laws and regulations for every life sphere, finding a Cook Notice of Violation of Fair Debt Act - Improper Contact at Work meeting all regional requirements can be exhausting, and ordering it from a professional lawyer is often pricey. Numerous online services offer the most common state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most extensive online catalog of templates, collected by states and areas of use. Apart from the Cook Notice of Violation of Fair Debt Act - Improper Contact at Work, here you can find any specific form to run your business or personal affairs, complying with your regional requirements. Specialists check all samples for their validity, so you can be certain to prepare your documentation properly.

Using the service is fairly simple. If you already have an account on the platform and your subscription is valid, you only need to log in, select the required sample, and download it. You can get the document in your profile at any time later on. Otherwise, if you are new to the platform, there will be some extra actions to complete before you obtain your Cook Notice of Violation of Fair Debt Act - Improper Contact at Work:

- Examine the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another form utilizing the corresponding option in the header.

- Click Buy Now once you’re certain in the chosen document.

- Select the subscription plan that suits you most.

- Sign up for an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Cook Notice of Violation of Fair Debt Act - Improper Contact at Work.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the acquired template, you can find all the files you’ve ever saved in your profile by opening the My Forms tab. Give it a try!