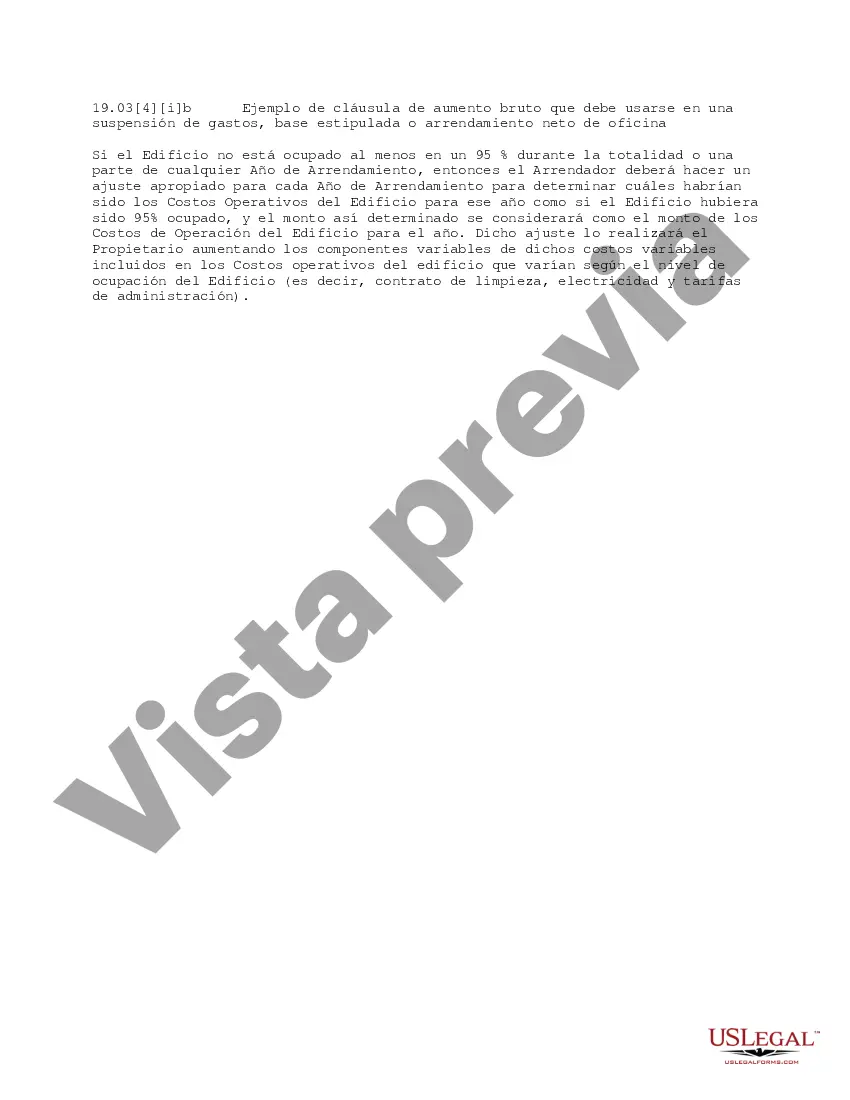

A Fairfax Virginia Gross Up Clause is a crucial component in an Expense Stop Stipulated Base or Office Net Lease agreement. This clause allows landlords to pass on a fair share of operating expenses to tenants, while also ensuring that expenses associated with vacant spaces are adequately covered. By incorporating a Gross Up Clause, landlords can calculate and allocate expenses in a more equitable and manageable manner. The primary purpose of a Fairfax Virginia Gross Up Clause is to ensure that tenants are responsible for their proportionate share of operating expenses based on the occupied space. It enables landlords to adjust operating expenses to account for vacant spaces, ensuring that the financial burden does not fall solely on existing tenants. This clause enables a fair and transparent allocation of expenses among tenants. There are several types of Fairfax Virginia Gross Up Clauses that can be utilized depending on the specific lease agreement. Here are some commonly used types: 1. Direct Expense Gross Up: This clause calculates expenses based on the total occupied square footage in the building. It includes all direct expenses related to the operation and maintenance of the property, such as property taxes, insurance, and property management fees. Direct Expense Gross Up ensures that tenants are responsible for their fair share of direct expenses, considering the occupied space only. 2. Indirect Expense Gross Up: This clause covers expenses that are not directly tied to the occupied space but are necessary for the overall functioning of the property. Examples include common area maintenance expenses, utility costs, and repairs. Indirect Expense Gross Up allocates these expenses based on the proportionate share of occupied space. 3. Variable Expense Gross Up: This clause addresses expenses that can fluctuate over time, such as utilities or taxes. It enables landlords to adjust these expenses annually or at regular intervals, taking into account changes in occupancy or other relevant factors. Variable Expense Gross Up allows for flexibility in adjusting expenses to accurately reflect the current situation. 4. Base Year Gross Up: This type of Gross Up Clause establishes a base year against which future expenses will be calculated. The base year is typically the first year of the lease term or a predefined year when actual expenses are determined. Subsequent years' expenses are then adjusted based on any increase or decrease from the base year. In conclusion, a Fairfax Virginia Gross Up Clause is an essential component of an Expense Stop Stipulated Base or Office Net Lease agreement. By utilizing appropriate Gross Up Clauses, landlords can ensure a fair distribution of operating expenses while considering both occupied and vacant spaces. The various types of Gross Up Clauses enable customization based on the specific lease agreement and requirements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Fairfax Virginia Cláusula de aumento total que se debe utilizar en una base estipulada de parada de gastos o arrendamiento neto de oficina - Gross up Clause that Should be Used in an Expense Stop Stipulated Base or Office Net Lease

Description

How to fill out Fairfax Virginia Cláusula De Aumento Total Que Se Debe Utilizar En Una Base Estipulada De Parada De Gastos O Arrendamiento Neto De Oficina?

A document routine always goes along with any legal activity you make. Opening a business, applying or accepting a job offer, transferring property, and lots of other life situations demand you prepare official documentation that varies throughout the country. That's why having it all collected in one place is so helpful.

US Legal Forms is the most extensive online collection of up-to-date federal and state-specific legal templates. Here, you can easily locate and download a document for any individual or business purpose utilized in your county, including the Fairfax Gross up Clause that Should be Used in an Expense Stop Stipulated Base or Office Net Lease.

Locating templates on the platform is amazingly simple. If you already have a subscription to our library, log in to your account, find the sample using the search field, and click Download to save it on your device. Following that, the Fairfax Gross up Clause that Should be Used in an Expense Stop Stipulated Base or Office Net Lease will be available for further use in the My Forms tab of your profile.

If you are dealing with US Legal Forms for the first time, adhere to this quick guide to obtain the Fairfax Gross up Clause that Should be Used in an Expense Stop Stipulated Base or Office Net Lease:

- Ensure you have opened the correct page with your regional form.

- Utilize the Preview mode (if available) and browse through the sample.

- Read the description (if any) to ensure the template corresponds to your needs.

- Search for another document via the search option if the sample doesn't fit you.

- Click Buy Now when you find the required template.

- Select the appropriate subscription plan, then sign in or create an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Choose file format and download the Fairfax Gross up Clause that Should be Used in an Expense Stop Stipulated Base or Office Net Lease on your device.

- Use it as needed: print it or fill it out electronically, sign it, and file where requested.

This is the simplest and most trustworthy way to obtain legal paperwork. All the templates available in our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and run your legal affairs properly with the US Legal Forms!