Montgomery County in Maryland has a specific provision defining the taxable components falling into the escalation definition of taxes. This provision lays out the specific items that are subject to taxation, ensuring transparency and clarity in the tax system. Understanding this provision is vital for taxpayers, businesses, and local authorities to accurately determine their tax liabilities and obligations in Montgomery County. The Montgomery Maryland provision defining taxable components falling into the escalation definition of taxes encompasses various categories. Here, we will explore some key types of taxable components falling under this provision: 1. Real Estate Tax: Montgomery County imposes a tax on the assessed value of real property owned within its jurisdiction. This tax is calculated based on the property's assessed value and the current tax rate set by the county government. The taxable components related to real estate include residential properties, commercial properties, land, and any improvements made to the property. 2. Personal Property Tax: Montgomery County also levies taxes on personal property owned by businesses and individuals. This includes tangible assets such as vehicles, equipment, machinery, and inventory held for commercial purposes. The taxable components for personal property vary depending on the nature and value of the assets. 3. Income Tax: Income earned within Montgomery County is also subject to taxation based on a progressive tax rate structure. This provision defines taxable components falling into the escalation definition of income taxes, considering sources such as wages, salaries, dividends, interest, and capital gains. Different tax rates apply to various income brackets, and these components play a crucial role in determining the tax liability of individuals and businesses. 4. Sales and Use Tax: Montgomery County imposes a sales and use tax on the sale or use of tangible personal property and specific services. Taxable components include retail sales of goods, leases, and rentals, as well as taxable services rendered within the county. It is important for businesses to understand which goods and services fall under this provision to ensure accurate collection and remittance of sales and use taxes. 5. Transfer and Decoration Tax: Any transfer or sale of real property in Montgomery County is subject to transfer and decoration taxes. The taxable components falling under this provision include the value of the property being transferred, which may include land, residential or commercial structures, and associated improvements. These taxes are typically paid by the seller or buyer, depending on the terms of the transaction. 6. Special Taxes: Montgomery County may also have specific provisions for special taxes that are imposed for designated purposes. These special taxes can include components such as hotel taxes, rental taxes, or taxes on specific industries or activities. Understanding these provisions is essential for businesses operating in sectors subject to such special taxes. In summary, Montgomery County in Maryland has a provision defining various taxable components falling into the escalation definition of taxes. It encompasses real estate taxes, personal property taxes, income taxes, sales and use taxes, transfer and decoration taxes, as well as potential special taxes. Familiarity with these components is crucial for accurate tax compliance and financial planning within the county.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Montgomery Maryland Disposición que define los componentes imponibles que caen en la definición de escalamiento de los impuestos - Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes

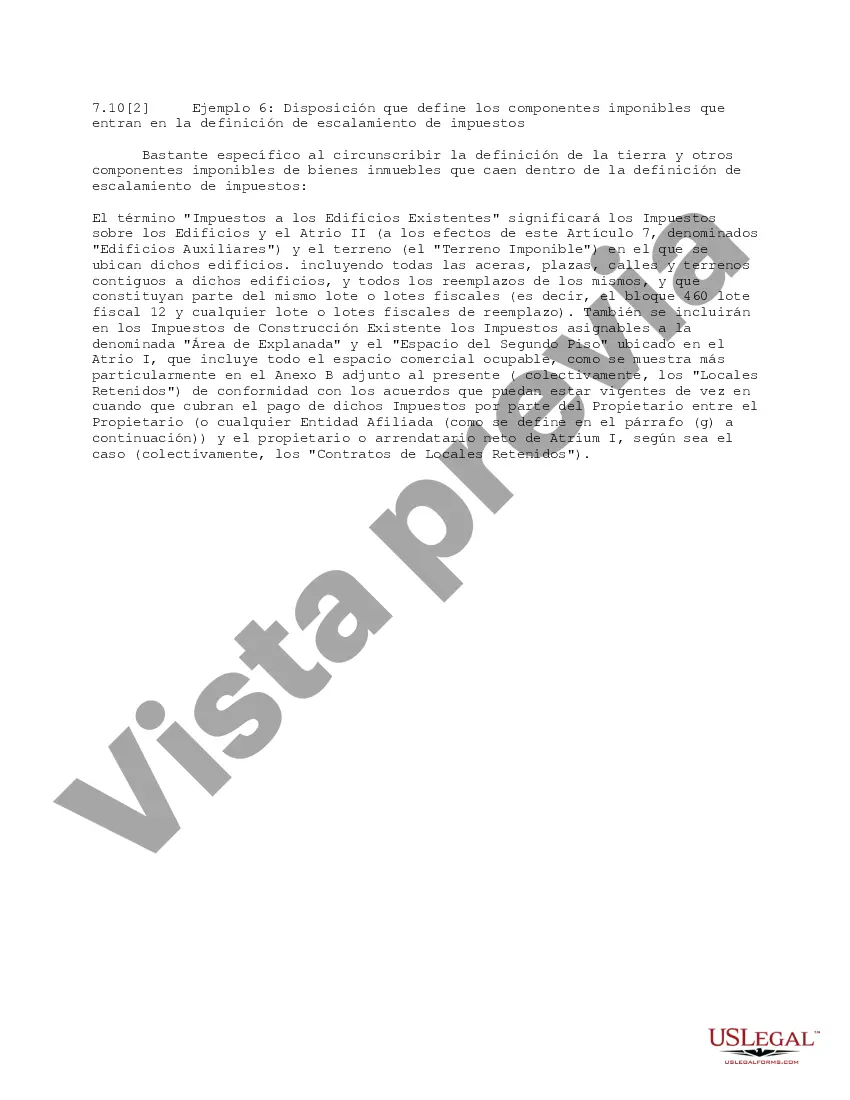

Description

How to fill out Montgomery Maryland Disposición Que Define Los Componentes Imponibles Que Caen En La Definición De Escalamiento De Los Impuestos?

Preparing legal paperwork can be burdensome. In addition, if you decide to ask a legal professional to write a commercial contract, documents for proprietorship transfer, pre-marital agreement, divorce paperwork, or the Montgomery Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes, it may cost you a lot of money. So what is the most reasonable way to save time and money and draft legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is an excellent solution, whether you're looking for templates for your personal or business needs.

US Legal Forms is the most extensive online library of state-specific legal documents, providing users with the up-to-date and professionally checked forms for any use case accumulated all in one place. Therefore, if you need the recent version of the Montgomery Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes, you can easily find it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Montgomery Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes:

- Look through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to make sure it's the template you need.

- Don't worry if the form doesn't suit your requirements - look for the right one in the header.

- Click Buy Now when you find the needed sample and pick the best suitable subscription.

- Log in or register for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the file format for your Montgomery Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes and save it.

Once finished, you can print it out and complete it on paper or upload the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the paperwork ever obtained multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!