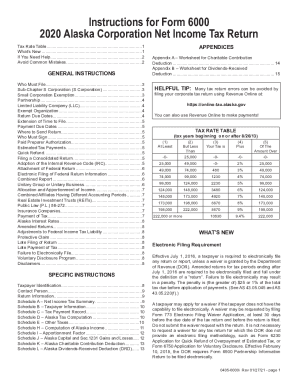

Get Ak 6000i 2020

How it works

-

Open form follow the instructions

-

Easily sign the form with your finger

-

Send filled & signed form or save

Tips on how to fill out, edit and sign 2015 alaska return online

How to fill out and sign 2015 6000i income online?

Get your online template and fill it in using progressive features. Enjoy smart fillable fields and interactivity. Follow the simple instructions below:

When the tax period started unexpectedly or maybe you just misssed it, it could probably cause problems for you. AK 6000i is not the easiest one, but you have no reason for panic in any case.

Utilizing our convenient online sofware you will see the right way to fill AK 6000i even in situations of critical time deficit. You simply need to follow these easy recommendations:

-

Open the record with our advanced PDF editor.

-

Fill in all the details required in AK 6000i, using fillable lines.

-

Insert photos, crosses, check and text boxes, if needed.

-

Repeating info will be added automatically after the first input.

-

In case of misunderstandings, use the Wizard Tool. You will see useful tips for simpler completion.

-

Do not forget to add the date of application.

-

Make your unique e-signature once and place it in the required lines.

-

Check the details you have included. Correct mistakes if needed.

-

Click on Done to complete editing and select how you will deliver it. You have the ability to use online fax, USPS or electronic mail.

-

It is possible to download the file to print it later or upload it to cloud storage like Google Drive, Dropbox, etc.

Using our powerful digital solution and its useful tools, completing AK 6000i becomes more handy. Don?t wait to use it and have more time on hobbies rather than on preparing files.

How to modify 2015 ak compress: customize forms online

Check out a single service to handle all of your paperwork with ease. Find, modify, and complete your 2015 ak compress in a single interface with the help of smart instruments.

The days when people needed to print out forms or even write them by hand are long gone. These days, all it takes to find and complete any form, like 2015 ak compress, is opening a single browser tab. Here, you can find the 2015 ak compress form and customize it any way you need, from inserting the text directly in the document to drawing it on a digital sticky note and attaching it to the document. Discover instruments that will streamline your paperwork without additional effort.

Click the Get form button to prepare your 2015 ak compress paperwork quickly and start editing it instantly. In the editing mode, you can easily fill in the template with your details for submission. Just click on the field you need to change and enter the data right away. The editor's interface does not demand any specific skills to use it. When done with the edits, check the information's accuracy once again and sign the document. Click on the signature field and follow the instructions to eSign the form in a moment.

Use Additional instruments to customize your form:

- Use Cross, Check, or Circle instruments to pinpoint the document's data.

- Add text or fillable text fields with text customization tools.

- Erase, Highlight, or Blackout text blocks in the document using corresponding instruments.

- Add a date, initials, or even an image to the document if necessary.

- Utilize the Sticky note tool to annotate the form.

- Use the Arrow and Line, or Draw tool to add graphic components to your document.

Preparing 2015 ak compress paperwork will never be complicated again if you know where to search for the suitable template and prepare it easily. Do not hesitate to try it yourself.

Related links form

Industry-leading security and compliance

-

In businnes since 199725+ years providing professional legal documents.

-

Accredited businessGuarantees that a business meets BBB accreditation standards in the US and Canada.

-

Secured by BraintreeValidated Level 1 PCI DSS compliant payment gateway that accepts most major credit and debit card brands from across the globe.