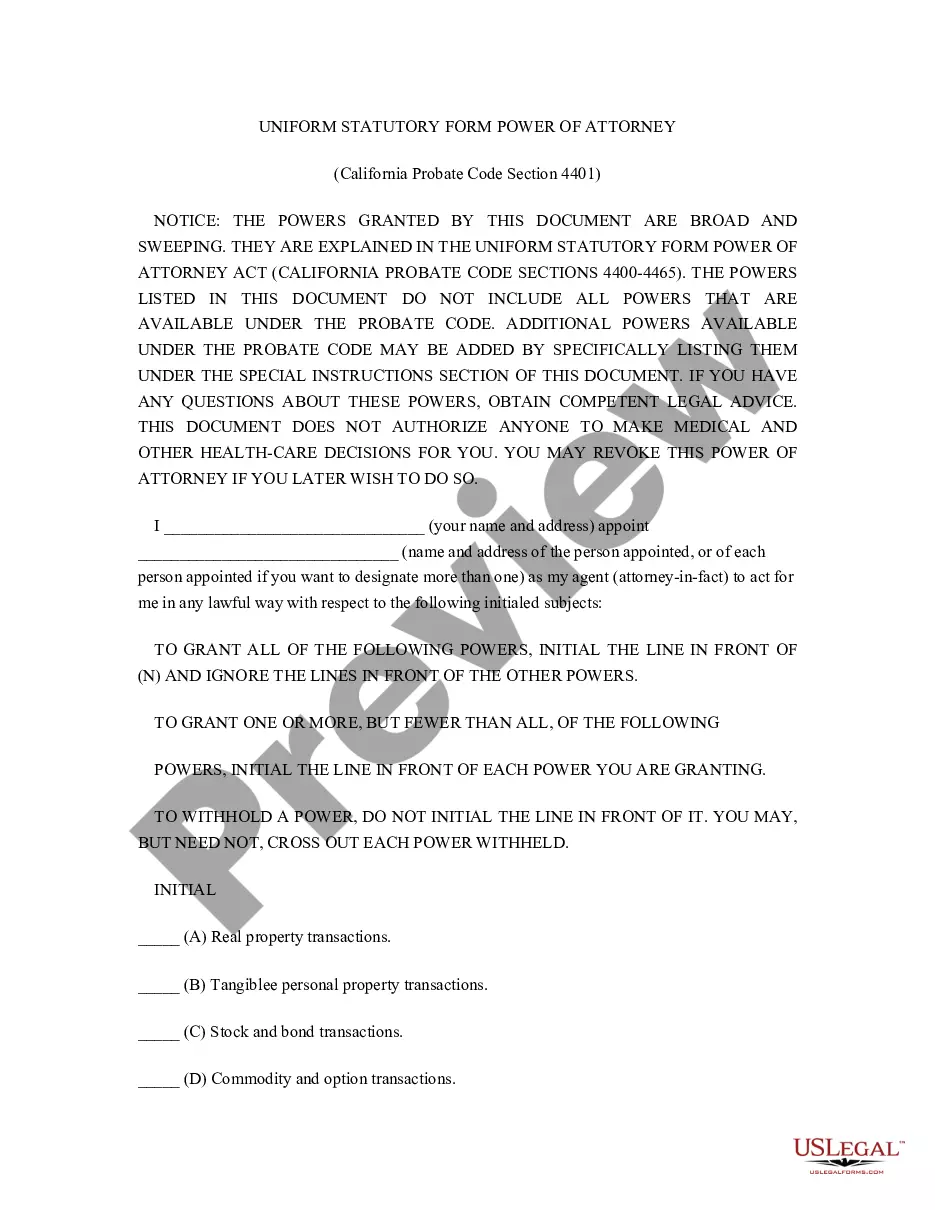

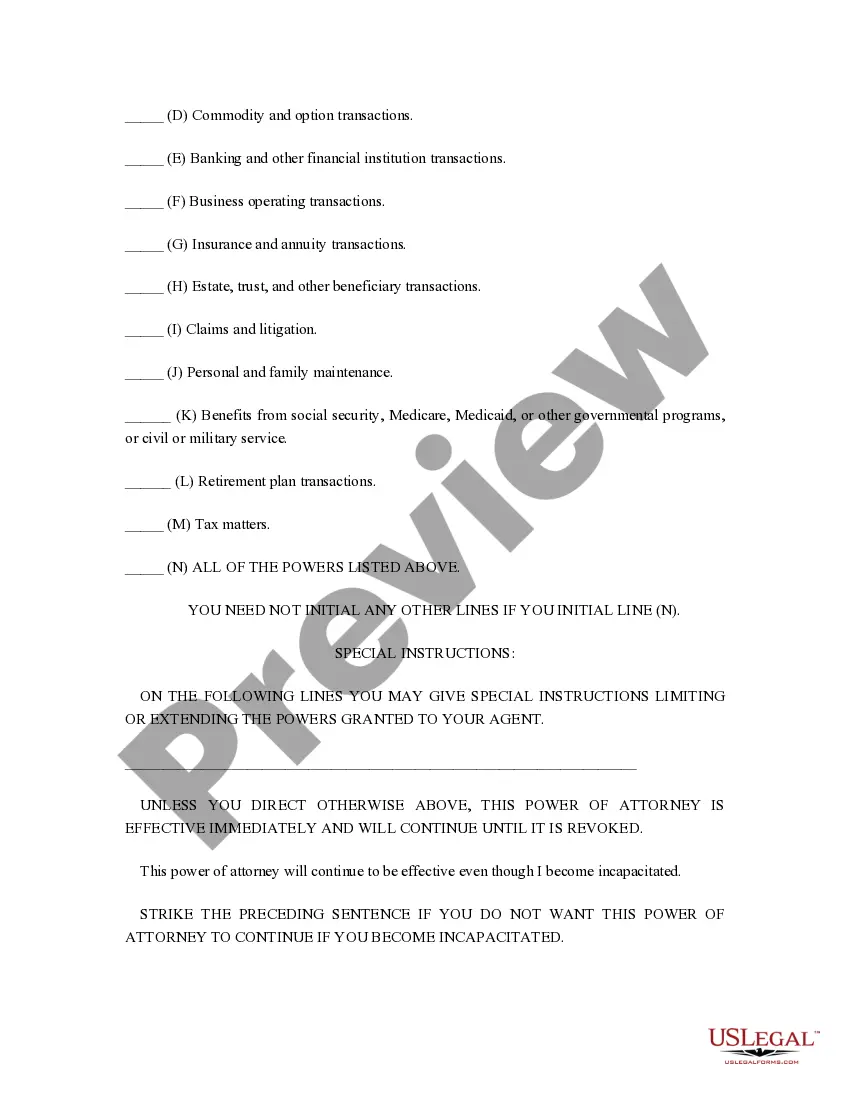

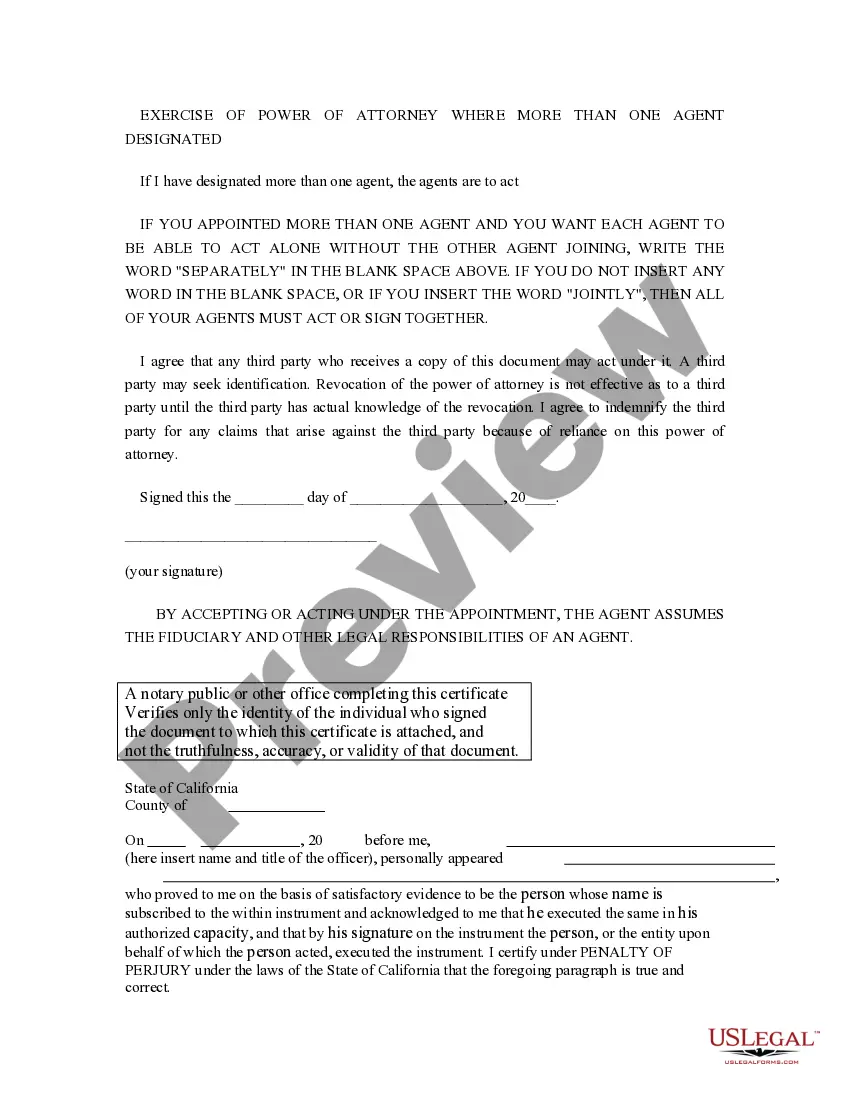

This form is a Uniform Statutory Form of Power of Attorney for California for property, finances and other powers you specify. It also provides that it can be durable.

California Uniform 4401 withholding refers to a specific type of withholding tax applicable in the state of California. This tax is imposed on payments made to non-resident individuals or entities who earn income from California sources but are not California residents. Withholding taxes serve as a mechanism to collect tax revenue and ensure compliance with tax laws from non-residents. Under the California Uniform 4401 withholding, non-resident taxpayers are subject to a flat tax rate of 7% on their income derived from California sources. The income subject to withholding includes wages, salaries, commissions, bonuses, rental and lease payments, royalties, and other types of California-sourced income. There are two main types of California Uniform 4401 withholding: 1. Non-wage Withholding: This type of withholding is applicable when non-resident taxpayers receive non-wage income from California sources. Examples include rental income from California properties, royalties from intellectual property located in California, and income from freelance or consulting services rendered in California. 2. Wage Withholding: This type of withholding is applicable when non-resident taxpayers earn wages or salaries from California employers. It includes regular wages, overtime pay, bonuses, and commissions paid by California employers to non-resident employees. It's important to note that non-resident taxpayers who have sufficient connections to California, such as owning property or engaging in substantial business activities within the state, may be subject to California income tax laws beyond the withholding requirements. To comply with California Uniform 4401 withholding, employers are required to withhold 7% of the non-resident employee's wages and remit these withheld amounts to the California Franchise Tax Board (FT) on a regular basis. Non-wage payers, such as lessors and royalties' payers, are also responsible for withholding the appropriate amounts and submitting them to the FT. In conclusion, California Uniform 4401 withholding is a tax mechanism that ensures non-resident taxpayers pay their fair share of taxes on income earned from California sources. It encompasses wage and non-wage income, and both employers and non-wage payers have specific responsibilities to withhold and submit the appropriate tax amounts to the California tax authorities.California Uniform 4401 withholding refers to a specific type of withholding tax applicable in the state of California. This tax is imposed on payments made to non-resident individuals or entities who earn income from California sources but are not California residents. Withholding taxes serve as a mechanism to collect tax revenue and ensure compliance with tax laws from non-residents. Under the California Uniform 4401 withholding, non-resident taxpayers are subject to a flat tax rate of 7% on their income derived from California sources. The income subject to withholding includes wages, salaries, commissions, bonuses, rental and lease payments, royalties, and other types of California-sourced income. There are two main types of California Uniform 4401 withholding: 1. Non-wage Withholding: This type of withholding is applicable when non-resident taxpayers receive non-wage income from California sources. Examples include rental income from California properties, royalties from intellectual property located in California, and income from freelance or consulting services rendered in California. 2. Wage Withholding: This type of withholding is applicable when non-resident taxpayers earn wages or salaries from California employers. It includes regular wages, overtime pay, bonuses, and commissions paid by California employers to non-resident employees. It's important to note that non-resident taxpayers who have sufficient connections to California, such as owning property or engaging in substantial business activities within the state, may be subject to California income tax laws beyond the withholding requirements. To comply with California Uniform 4401 withholding, employers are required to withhold 7% of the non-resident employee's wages and remit these withheld amounts to the California Franchise Tax Board (FT) on a regular basis. Non-wage payers, such as lessors and royalties' payers, are also responsible for withholding the appropriate amounts and submitting them to the FT. In conclusion, California Uniform 4401 withholding is a tax mechanism that ensures non-resident taxpayers pay their fair share of taxes on income earned from California sources. It encompasses wage and non-wage income, and both employers and non-wage payers have specific responsibilities to withhold and submit the appropriate tax amounts to the California tax authorities.