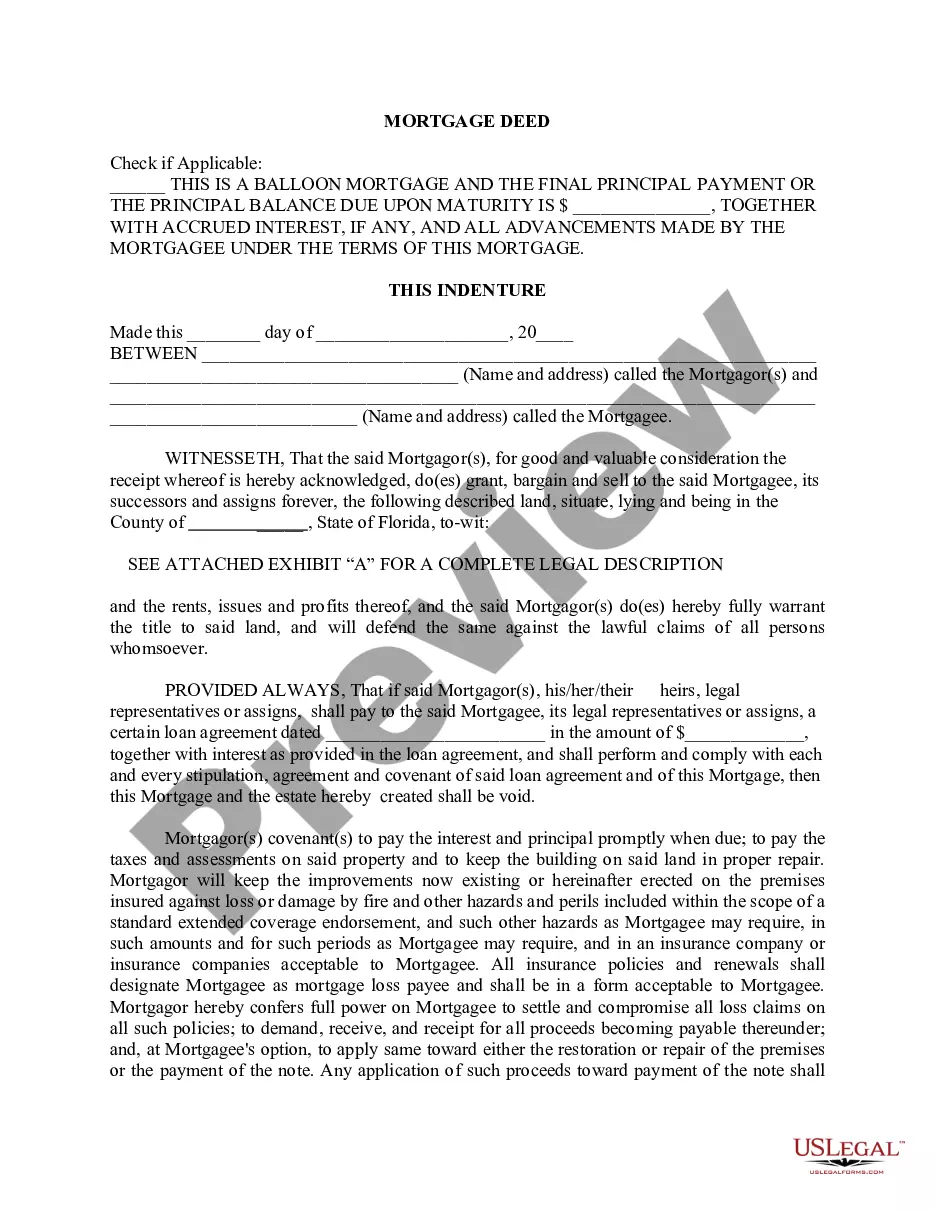

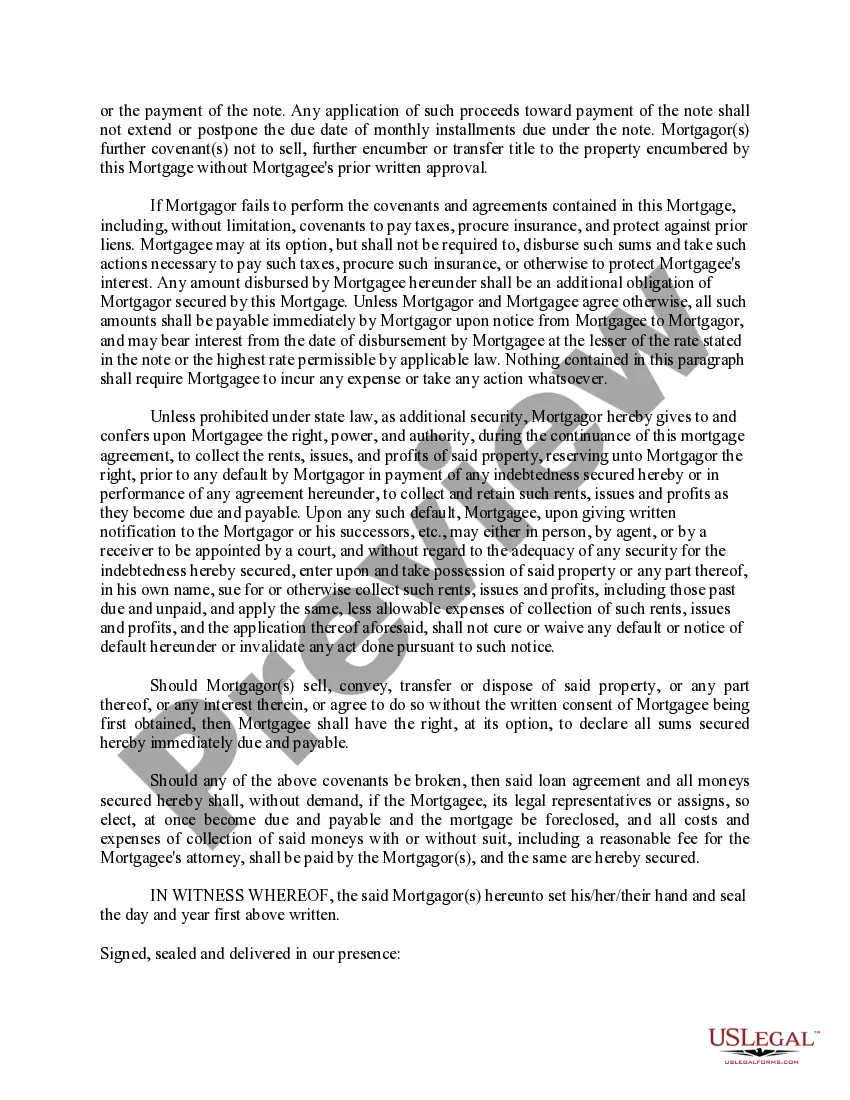

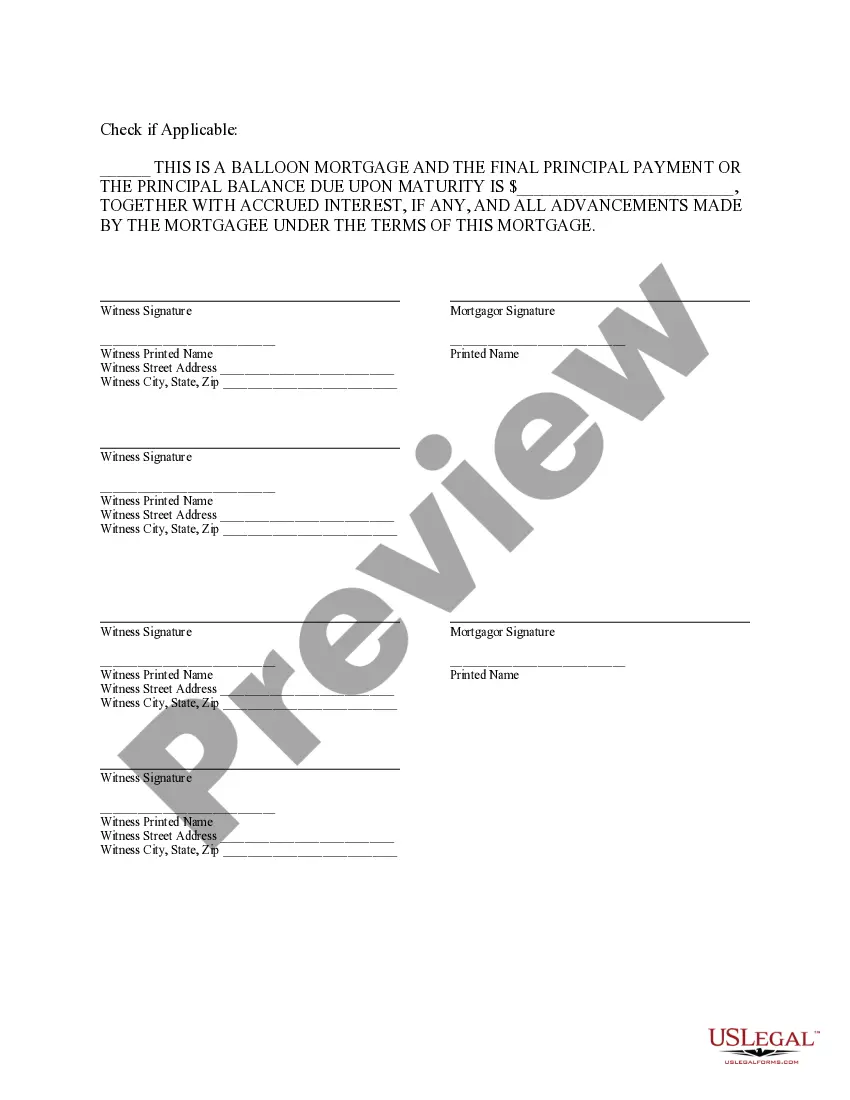

A mortgage deed with a bank refers to a legal document that establishes a contractual agreement between a borrower and a bank, where the borrower pledges a property as collateral for a loan received from the bank. This type of mortgage deed outlines the terms and conditions of the loan, the rights and obligations of both parties, and the procedures in case of default. Here is a detailed description of a mortgage deed sample with a bank, including the various types of mortgage deeds: 1. Definition: A mortgage deed with a bank is a legally binding agreement that enables individuals or businesses to obtain financing from a bank by using their property as security. 2. Parties Involved: The mortgage deed involves two primary parties: a. Borrower: The individual or entity applying for the loan and pledging their property as collateral. b. Bank: The financial institution providing the funds to the borrower and holding the mortgage over the property. 3. Loan Amount and Security: The mortgage deed specifies the loan amount granted by the bank and describes the property offered as security for the loan. This includes details such as property address, legal description, and any restrictions on the property. 4. Repayment Terms: The document outlines the repayment terms, including the loan duration, interest rate, payment frequency, and any provisions for early repayment or prepayment penalties. It also specifies the consequences of default or non-payment. 5. Rights and Obligations: The mortgage deed highlights the responsibilities and rights of both the borrower and the bank. It may include terms related to property insurance, maintenance, taxes, and the bank's rights to inspect or monitor the property. 6. Default and Foreclosure: This section explains the process and consequences of default. It outlines the steps the bank can take, such as issuing a notice of default, initiating foreclosure proceedings, and auctioning the property to recover the outstanding debt. 7. Additional Clauses: Depending on the specific requirements, the mortgage deed may include additional clauses such as acceleration clauses (allowing the bank to demand immediate full repayment under specific circumstances) or subordination clauses (prioritizing multiple mortgage liens). Types of Mortgage Deed Samples with Banks: 1. Fixed-Rate Mortgage Deed: In this type, the interest rate remains constant throughout the loan term, providing predictable and stable monthly payments. 2. Adjustable-Rate Mortgage Deed: With this mortgage deed, the interest rate can adjust periodically based on market conditions, potentially resulting in fluctuating monthly payments. 3. Balloon Mortgage Deed: This type involves making smaller monthly payments initially, followed by a larger lump-sum payment at the end of the loan term. 4. Interest-Only Mortgage Deed: In this arrangement, the borrower pays only the interest portion for a specified period, with the principal repaid later. Remember, it is essential to consult with legal professionals or specialized mortgage advisors to understand the specific terms and conditions mentioned within each type of mortgage deed.

Mortgage Deed Sample With Bank

Description What Does A Deed Look Like In Florida

How to fill out What Does A Mortgage Agreement Look Like?

Handling legal paperwork and procedures might be a time-consuming addition to your day. Mortgage Deed Sample With Bank and forms like it often need you to search for them and understand how you can complete them properly. As a result, whether you are taking care of economic, legal, or individual matters, using a comprehensive and convenient web catalogue of forms at your fingertips will greatly assist.

US Legal Forms is the top web platform of legal templates, boasting over 85,000 state-specific forms and a number of tools to assist you complete your paperwork effortlessly. Discover the catalogue of pertinent documents available to you with just one click.

US Legal Forms provides you with state- and county-specific forms available at any moment for downloading. Protect your document management processes using a high quality support that allows you to put together any form in minutes without having additional or hidden charges. Simply log in to the account, locate Mortgage Deed Sample With Bank and download it right away from the My Forms tab. You may also gain access to formerly saved forms.

Would it be the first time making use of US Legal Forms? Sign up and set up your account in a few minutes and you will get access to the form catalogue and Mortgage Deed Sample With Bank. Then, adhere to the steps listed below to complete your form:

- Make sure you have discovered the proper form by using the Review option and reading the form information.

- Choose Buy Now as soon as all set, and select the subscription plan that meets your needs.

- Choose Download then complete, sign, and print out the form.

US Legal Forms has twenty five years of experience supporting users deal with their legal paperwork. Discover the form you want today and streamline any process without breaking a sweat.