- US Legal Forms

- Waiver and Release Forms

-

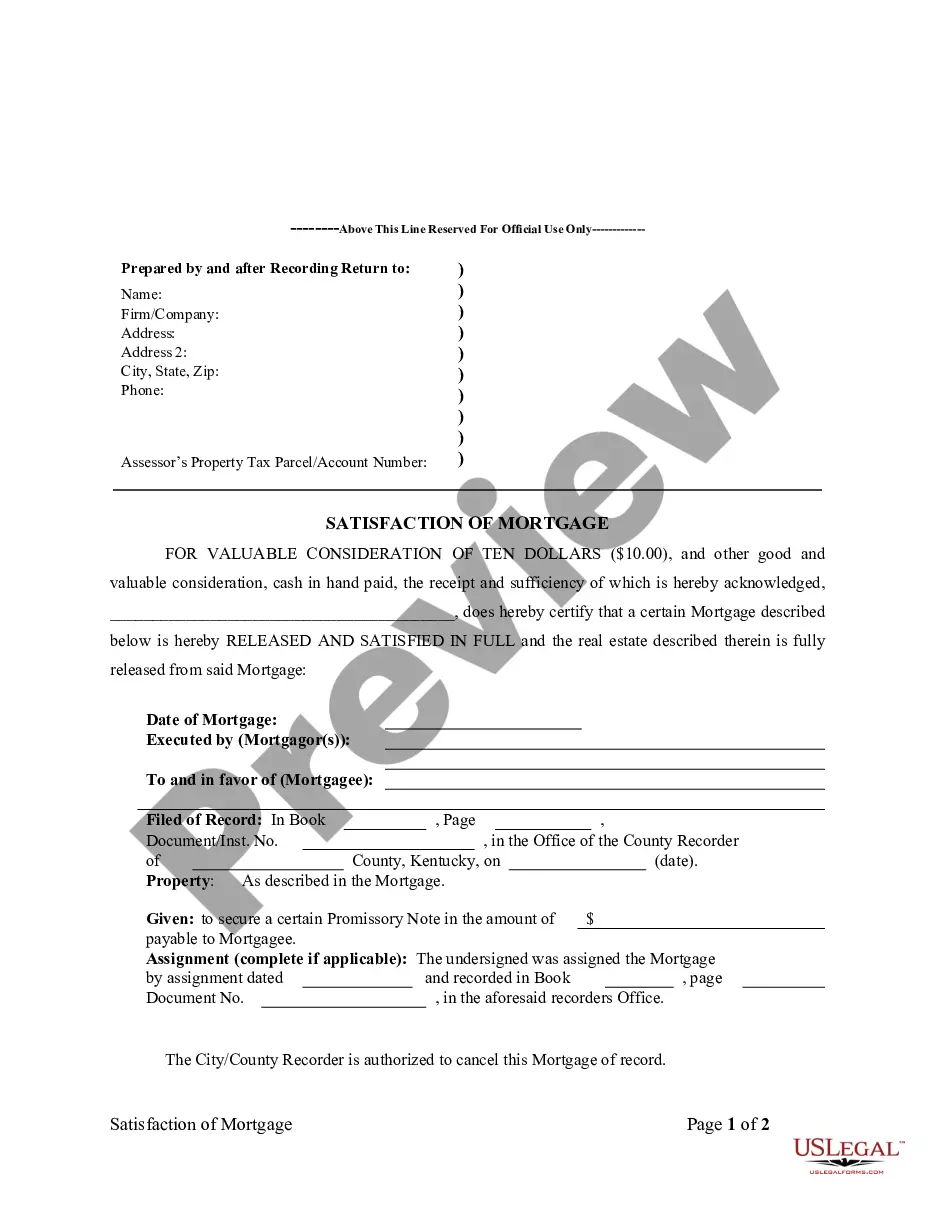

Kentucky Satisfaction...

Kentucky Release Mortgage For Bad Credit

Description Mortgagee Released Prepared

Released Mortgagor Valuable Related forms

View Montana promissory note with payment schedule

View Montana promissory note with personal guarantee

View Montana promissory note with personal guarantee template

View Montana promissory note without interest

View Montana promissory note without interest tax implications

Viewed forms

How to fill out Mortgagee Parcel Valuable?

What is the most reliable service to acquire the Kentucky Release Mortgage For Bad Credit and other recent versions of legal paperwork? US Legal Forms is the solution! It's the largest collection of legal documents for any occasion. Every sample is professionally drafted and checked for compliance with federal and local laws and regulations. They are grouped by field and state of use, so finding the one you need is an easy task.

Experienced users of the platform only need to log in to the system, check if their subscription is valid, and click the Download key near the Kentucky Release Mortgage For Bad Credit to acquire it. Once saved, the sample remains available for further use within the My Forms tab of your profile. If you still don't have an account with our library, here are the actions that you need to take to get one:

- Form compliance study. Before you obtain any template, you must check if it satisfies your use case terms and your state or county's regulations. Read the form description and utilize the Preview if available.

- Alternative document search. If there are any inconsistencies, utilize the search bar in the page header to find a different sample. Click Buy Now to pick the right one.

- Registration and subscription purchase. Decide on the most appropriate pricing plan, log in or create your account, and pay for your subscription via PayPal or credit card.

- Downloading the paperwork. Decide on the format you want to save the Kentucky Release Mortgage For Bad Credit (PDF or DOCX) and click Download to obtain it.

US Legal Forms is an excellent solution for everyone who needs to handle legal paperwork. Premium users can get even more since they complete and sign the earlier saved papers electronically at any time within the integrated PDF editing tool. Check it out today!

Inst Mortgagor Secure Form Rating

Inst Satisfied Promissory Form popularity

Assessor Mortgagee Released Other Form Names

Mortgagee Satisfied Favor FAQ

A New Mortgage May Temporarily Lower Your Credit Score When a lender pulls your credit score and report as part of a loan application, the inquiry can cause a minor drop in your credit score (usually less than five points).

For most lenders, you'll need credit scores between 620 and 680 as a minimum to a mortgage.

On FHA loans in Kentucky, FHA will go down to a 500 minimum credit score with at least 10% down payment or 10% equity on a refinance. If your scores is over 580, then you could use a FHA loan in Kentucky to with just 3.5% down payment or refinance with that much equity.

Kentucky FHA Mortgage Credit Score Requirements To be eligible for maximum financing, borrowers will need a minimum credit score of 500 or higher. Kentucky FHA Borrowers with a credit score between 500 and 579 will be limited to a loan to value of 90%.

Qualified mortgages can't have the following: Risky loan features, or those that offer artificially low monthly loan repayments in the early years of the loan term, including interest-only, balloon or negative amortization loans, sometimes referred to as subprime mortgages.

Kentucky Release Mortgage For Bad Credit Related Searches

-

bad credit mortgage loans guaranteed approval

-

credit karma

-

first-time home buyer loans with bad credit and zero down

-

kentucky mortgage lenders

-

fha loan requirements ky

-

how to get a mortgage

-

credit karma

-

first-time home buyer loans with bad credit and zero down

-

fha loan requirements ky

-

how to get a mortgage

Mortgagee Parcel Valuable Interesting Questions

A release mortgage, also known as a discharge mortgage, is a legal document that releases a property from the mortgage lien once the loan has been fully paid off or satisfied.

Yes, it is possible to obtain a mortgage release in Kentucky even with bad credit. However, keep in mind that bad credit may affect your eligibility and the terms of the release.

Having bad credit might make it more challenging to find lenders willing to provide a mortgage release. Additionally, you may face higher interest rates or stricter terms due to the perceived higher risk associated with bad credit.

To improve your chances, you can start by understanding your credit situation and working towards improving your credit score. Paying off existing debts, making timely payments, and reducing your overall debt-to-income ratio can make you a more attractive borrower.

While there aren't specific mortgage release programs exclusive to borrowers with bad credit in Kentucky, various assistance programs and lenders might be more flexible in considering your application based on factors beyond just credit score.

While it is not legally required to involve a lawyer in the mortgage release process, it's helpful to consult with one to ensure all legal aspects are adequately addressed and to have proper guidance throughout the process.

Refinancing a mortgage with bad credit may be more challenging, but it is not impossible. It's advisable to work on improving your credit score before attempting to refinance, as it can potentially result in better terms and interest rates.

While specific document requirements may vary, you generally need to provide identification proof, income verification, bank statements, details of the current mortgage, and any additional documents required by the lender or mortgage release process.

The length of the mortgage release process can vary depending on several factors, including the complexity of the case, the responsiveness of involved parties, and the efficiency of the specific lender or institution handling the release. It can range from a few weeks to a couple of months.

Yes, you can sell your property even if you have a bad credit mortgage in Kentucky. However, it's essential to consider that any outstanding mortgage balance would need to be satisfied or released before transferring ownership to the buyer.

More info

Mortgagee Released Mortgage Trusted and secure by over 3 million people of the world’s leading companies

-

No results found.

-

Kentucky

-

Alabama

-

Alaska

-

Arizona

-

Arkansas

-

California

-

Colorado

-

Connecticut

-

Delaware

-

District of Columbia

-

Florida

-

Georgia

-

Hawaii

-

Idaho

-

Illinois

-

Indiana

-

Iowa

-

Kansas

-

Louisiana

-

Maine

-

Maryland

-

Massachusetts

-

Michigan

-

Minnesota

-

Mississippi

-

Missouri

-

Montana

-

Nebraska

-

Nevada

-

New Hampshire

-

New Jersey

-

New Mexico

-

New York

-

North Carolina

-

North Dakota

-

Ohio

-

Oklahoma

-

Oregon

-

Pennsylvania

-

Rhode Island

-

South Carolina

-

South Dakota

-

Tennessee

-

Texas

-

Utah

-

Vermont

-

Virginia

-

Washington

-

West Virginia

-

Wisconsin

-

Wyoming

Assignments Generally: Lenders, or holders of mortgages or deeds of trust, often assign mortgages or deeds of trust to other lenders, or third parties. When this is done the assignee (person who received the assignment) steps into the place of the original lender or assignor. To effectuate an assignment, the general rules is that the assignment must be in proper written format and recorded to provide notice of the assignment.

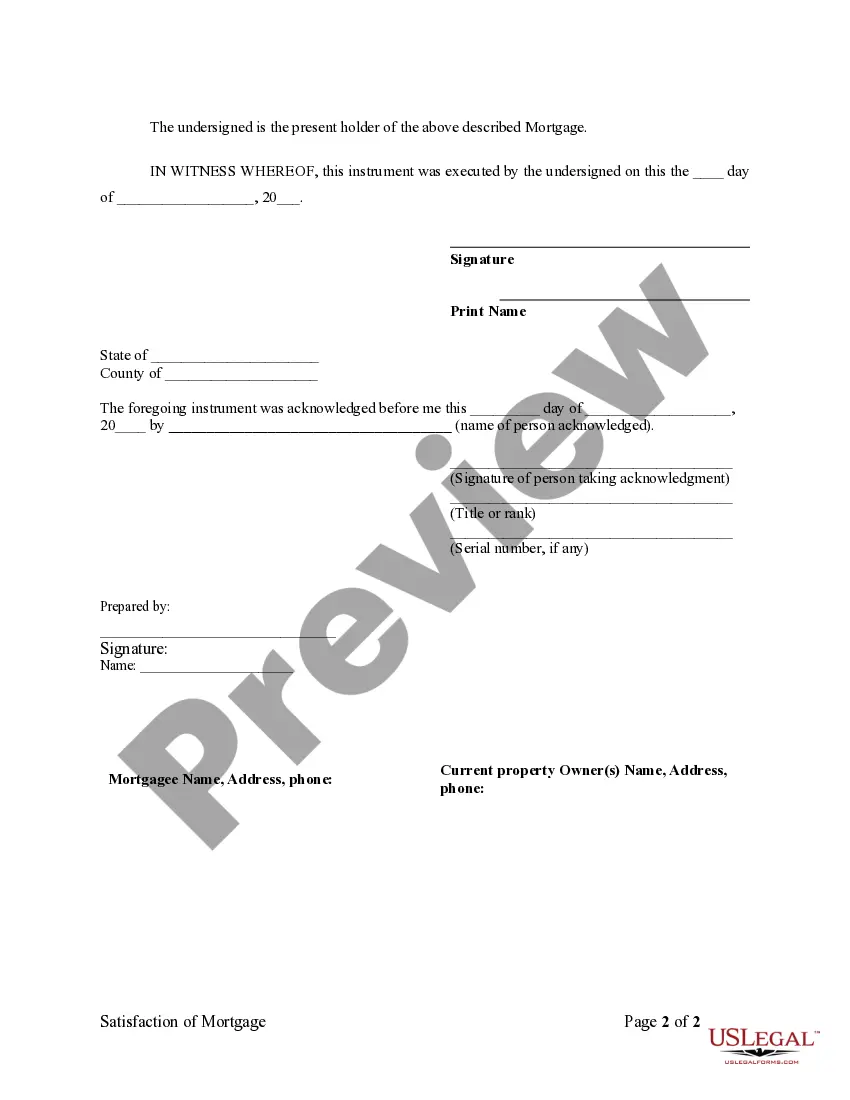

Satisfactions Generally: Once a mortgage or deed of trust is paid, the holder of the mortgage is required to satisfy the mortgage or deed of trust of record to show that the mortgage or deed of trust is no longer a lien on the property. The general rule is that the satisfaction must be in proper written format and recorded to provide notice of the satisfaction. If the lender fails to record a satisfaction within set time limits, the lender may be responsible for damages set by statute for failure to timely cancel the lien. Depending on your state, a satisfaction may be called a Satisfaction, Cancellation, or Reconveyance. Some states still recognize marginal satisfaction but this is slowly being phased out. A marginal satisfaction is where the holder of the mortgage physically goes to the recording office and enters a satisfaction on the face of the the recorded mortgage, which is attested by the clerk.

Kentucky Law

Execution of Assignment or Satisfaction: Must be signed by the mortgagee.

Assignment: An assignment must be in writing and recorded.

Demand to Satisfy: Written demand required. See below, Penalty.

Recording Satisfaction: A holder of a lien on real property shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

Marginal Satisfaction: Not allowed.

Penalty: If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner in securing the release of real property by such violation.

Acknowledgment: An assignment or satisfaction must contain a proper Kentucky acknowledgment, or other acknowledgment approved by Statute.

Kentucky Statutes

382.290 Recording of mortgages and deeds retaining liens -- Assignment -- Discharge -- Form of record -- Clerk's fee.

(1) In recording mortgages and deeds in which liens are retained (except railroad mortgages securing bonds payable to bearer), there shall be left a blank space immediately after the record of the deed or mortgage of at least two (2) full lines for each note or obligation named in the deed or mortgage, or in the alternative, at the option of the county clerk, a marginal entry record may be kept for the same purposes as the blank space. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instruments.(2) No county clerk or deputy county clerk shall admit to record any mortgage or deed in which liens are retained unless the mortgage or deed in which a lien is retained plainly specifies and refers to the immediate source from which the mortgagor or grantor derived title to the property or the interest encumbered therein.

(3) When any note named in any deed or mortgage is assigned to any other person, the assignor may, over his own hand, attested by the clerk, note such assignment in the blank space, or in a marginal entry record, beside a listing of the book and page of the document being assigned, and when any one (1) or more of the notes named in any deed or mortgage is paid, or otherwise released or satisfied, the holder of the note, and who appears from the record to be such holder, may release the lien, so far as such note is concerned, by release, over his own hand, attested by the clerk. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instrument.

(4) No person who does not, from such record or assignment of record, appear at the time to be the legal holder of any note secured by lien in any deed or mortgage, shall be permitted to release the lien securing any such note, and any release made in contravention of this section shall be void; but this section does not change the existing law if no such entry is made.

(5) For each assignment and release so made and attested by the clerk, he may charge a fee pursuant to KRS 64.012 to be paid by the person executing the release or noting the assignment.

(6) If such assignment of a note is made by separate instrument or by deed assigning the note, or in a marginal entry record, the instrument of writing or deed or marginal entry record shall set forth the date of notes assigned, a brief description of notes, the name and post office address of assignee, and the deed book and page of the instrument wherein the lien or mortgage is recorded and the clerk or deputy clerk receiving such instrument of writing or deed of assignment for record shall at the option of the county clerk immediately either link the assignment and its filing location to its respective referenced instrument in the indexing system for the referenced instrument, or endorse at the foot of the record in the space provided in subsection (1) of this section, "The notes mentioned herein (giving a brief description of notes assigned) have been transferred and assigned to (insert name and address of assignee) by deed of assignment (or describe instrument) dated and recorded in deed book .... page ....," and attest such certificate. For making such notation on the record the clerk shall be allowed a fee pursuant to KRS 64.012 for each notation so made, to be paid by the party filing the instrument of writing or deed of assignment.

(7) No holder of a note secured by lien retained in either deed or mortgage shall lodge for record, and no clerk or deputy clerk shall receive and permit to be lodged for record, any deed or instrument of writing that does not comply with the provisions of this section.

382.335 Certain information to be included in instruments in order for them to be recorded.

(1) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or personal property, or any interest therein or lien thereon, is conveyed, granted, encumbered, assigned, or otherwise disposed of; nor receive any instrument or permit any instrument, provided by law, to be recorded as evidence of title to real estate, unless the instrument has endorsed on it, a printed, typewritten, or stamped statement showing the name and address of the individual who prepared the instrument, and the statement is signed by the individual. The person who prepared the instrument may execute his or her signature by affixing a facsimile of his or her signature on the instrument. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1962.(2) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or any interest therein is conveyed, granted, assigned, or otherwise disposed of unless the instrument contains the mailing address of the grantee or assignee. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1970.

(3) This section shall not apply to wills or to statutory liens in favor of the Commonwealth.

(4) No county clerk shall receive, or permit the recording of, any instrument by which real estate, or any interest therein, is conveyed, granted, assigned, transferred, or otherwise disposed of unless the instrument complies with the official indexing system of the county. The indexing system shall have been in place for at least twenty-four (24) months prior to July 15, 1994 or shall be implemented for the purpose of allowing computerized searching for the instruments of record of the county clerk. If a county clerk requires a parcel identification number on an instrument before recording, the clerk shall provide a computer terminal, at no charge to the public, for use in finding the parcel identification number. The county clerk may make reasonable rules about the use of the computer terminal, requests for a parcel identification number, or both.

(5) The receipt for record and recording of any instrument by the county clerk without compliance with the provisions of this section shall not prevent the record of filing of the instrument from becoming notice as otherwise provided by law, nor impair the admissibility of the record as evidence.

382.365 Release of lien, with notice to property owner, within thirty days of satisfaction — Assignments of liens — Proceeding against lienholder in District Court or Circuit Court — Liability of lienholder when lien not released or notice not sent — Notice to state or lienholder — Damages.

(1) A holder of a lien on real property, including a lien provided for in KRS 376.010, shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

(2) An assignee of a lien on real property shall record the assignment in the county clerk's office as required by KRS 382.360. Failure of an assignee to record a mortgage assignment shall not affect the validity or perfection, or invalidity or lack of perfection, of a mortgage lien under applicable law.

(3) A proceeding may be filed by any owner of real property or any party acquiring an interest in the real property in District Court or Circuit Court against a lienholder that violates subsection (1) or (2) of this section. A proceeding filed under this section shall be given precedence over other matters pending before the court.

(4) Upon proof to the court of the lien being satisfied by payment in full to the final lienholder or final assignee, the court shall enter a judgment noting the identity of the final lienholder or final assignee and authorizing and directing the master commissioner of the court to execute and file with the county clerk the requisite release or assignments or both, as appropriate. The judgment shall be with costs including a reasonable attorney's fee. If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property or to a party with an interest in the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. This written notice shall be properly addressed and sent by certified mail or delivered in person to the final lienholder or final assignee as follows:

(a) For a corporation, to an officer at the lienholder's principal address or to an agent for process located in Kentucky; however, if the corporation is a foreign corporation and has not appointed an agent for process in Kentucky, then to the agent for process in the state of domicile of the corporation;

(b) For an individual, to the individual at the address shown on the mortgage, at the lienholder's residence or place of business, or at an address to which the lienholder has directed that correspondence or payoff be sent;

(c) For a trust or an estate, to a fiduciary at the address shown on the mortgage or at an address to which the lienholder has directed that correspondence or payoff be sent; and

(d) For any other entity, including but not limited to limited liability companies, partnerships, limited partnerships, limited liability partnerships, and associations, to an officer, partner, or member at the entity's principal place of business or to an agent for process.

(5) A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property or to a party with an interest in the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner or a party with an interest in the real property in securing the release of real property by such violation and in securing an award of damages. Damages under this subsection for failure to record an assignment pursuant to KRS 382.360(3) shall not exceed three (3) times the actual damages, plus attorney's fees and court costs, but in no event less than five hundred dollars ($500).

(6) The former holder of a lien on real property shall send by regular mail a copy of the lien release to the property owner at his or her last known address within seven (7) days of the release. A former lienholder that violates this subsection shall be liable to the owner of the real property for fifty dollars ($50) and any actual expense incurred by the owner in obtaining documentation of the lien release.

(7) For the purposes of this section, “date of satisfaction” means that date of receipt by a holder of a lien on real property of a sum of money in the form of a certified check, cashier's check, wired transferred funds, or other form of payment satisfactory to the lienholder that is sufficient to pay the principal, interest, and other costs owing on the obligation that is secured by the lien on the property.

(8) The provisions of this section shall not apply when a lienholder is deceased and the estate of the lienholder has not been settled.

(9) The state licensing agency, if applicable, or any holder of a lien on real property shall be notified of the disposition of any actions brought under this section against the lienholder.

(10) The provisions of this section shall be held and construed as ancillary and supplemental to any other remedy provided by law.

(11) If more than one (1) owner or party with an interest in the real property brings an action to recover damages under this section, any statutory damages shall be allocated equally among recovering parties in the absence of agreement otherwise among said parties. The entry of a judgment awarding damages shall bar a subsequent action by any other person or entity to recover damages for the same violation.

Assignments Generally: Lenders, or holders of mortgages or deeds of trust, often assign mortgages or deeds of trust to other lenders, or third parties. When this is done the assignee (person who received the assignment) steps into the place of the original lender or assignor. To effectuate an assignment, the general rules is that the assignment must be in proper written format and recorded to provide notice of the assignment.

Satisfactions Generally: Once a mortgage or deed of trust is paid, the holder of the mortgage is required to satisfy the mortgage or deed of trust of record to show that the mortgage or deed of trust is no longer a lien on the property. The general rule is that the satisfaction must be in proper written format and recorded to provide notice of the satisfaction. If the lender fails to record a satisfaction within set time limits, the lender may be responsible for damages set by statute for failure to timely cancel the lien. Depending on your state, a satisfaction may be called a Satisfaction, Cancellation, or Reconveyance. Some states still recognize marginal satisfaction but this is slowly being phased out. A marginal satisfaction is where the holder of the mortgage physically goes to the recording office and enters a satisfaction on the face of the the recorded mortgage, which is attested by the clerk.

Kentucky Law

Execution of Assignment or Satisfaction: Must be signed by the mortgagee.

Assignment: An assignment must be in writing and recorded.

Demand to Satisfy: Written demand required. See below, Penalty.

Recording Satisfaction: A holder of a lien on real property shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

Marginal Satisfaction: Not allowed.

Penalty: If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner in securing the release of real property by such violation.

Acknowledgment: An assignment or satisfaction must contain a proper Kentucky acknowledgment, or other acknowledgment approved by Statute.

Kentucky Statutes

382.290 Recording of mortgages and deeds retaining liens -- Assignment -- Discharge -- Form of record -- Clerk's fee.

(1) In recording mortgages and deeds in which liens are retained (except railroad mortgages securing bonds payable to bearer), there shall be left a blank space immediately after the record of the deed or mortgage of at least two (2) full lines for each note or obligation named in the deed or mortgage, or in the alternative, at the option of the county clerk, a marginal entry record may be kept for the same purposes as the blank space. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instruments.(2) No county clerk or deputy county clerk shall admit to record any mortgage or deed in which liens are retained unless the mortgage or deed in which a lien is retained plainly specifies and refers to the immediate source from which the mortgagor or grantor derived title to the property or the interest encumbered therein.

(3) When any note named in any deed or mortgage is assigned to any other person, the assignor may, over his own hand, attested by the clerk, note such assignment in the blank space, or in a marginal entry record, beside a listing of the book and page of the document being assigned, and when any one (1) or more of the notes named in any deed or mortgage is paid, or otherwise released or satisfied, the holder of the note, and who appears from the record to be such holder, may release the lien, so far as such note is concerned, by release, over his own hand, attested by the clerk. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instrument.

(4) No person who does not, from such record or assignment of record, appear at the time to be the legal holder of any note secured by lien in any deed or mortgage, shall be permitted to release the lien securing any such note, and any release made in contravention of this section shall be void; but this section does not change the existing law if no such entry is made.

(5) For each assignment and release so made and attested by the clerk, he may charge a fee pursuant to KRS 64.012 to be paid by the person executing the release or noting the assignment.

(6) If such assignment of a note is made by separate instrument or by deed assigning the note, or in a marginal entry record, the instrument of writing or deed or marginal entry record shall set forth the date of notes assigned, a brief description of notes, the name and post office address of assignee, and the deed book and page of the instrument wherein the lien or mortgage is recorded and the clerk or deputy clerk receiving such instrument of writing or deed of assignment for record shall at the option of the county clerk immediately either link the assignment and its filing location to its respective referenced instrument in the indexing system for the referenced instrument, or endorse at the foot of the record in the space provided in subsection (1) of this section, "The notes mentioned herein (giving a brief description of notes assigned) have been transferred and assigned to (insert name and address of assignee) by deed of assignment (or describe instrument) dated and recorded in deed book .... page ....," and attest such certificate. For making such notation on the record the clerk shall be allowed a fee pursuant to KRS 64.012 for each notation so made, to be paid by the party filing the instrument of writing or deed of assignment.

(7) No holder of a note secured by lien retained in either deed or mortgage shall lodge for record, and no clerk or deputy clerk shall receive and permit to be lodged for record, any deed or instrument of writing that does not comply with the provisions of this section.

382.335 Certain information to be included in instruments in order for them to be recorded.

(1) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or personal property, or any interest therein or lien thereon, is conveyed, granted, encumbered, assigned, or otherwise disposed of; nor receive any instrument or permit any instrument, provided by law, to be recorded as evidence of title to real estate, unless the instrument has endorsed on it, a printed, typewritten, or stamped statement showing the name and address of the individual who prepared the instrument, and the statement is signed by the individual. The person who prepared the instrument may execute his or her signature by affixing a facsimile of his or her signature on the instrument. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1962.(2) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or any interest therein is conveyed, granted, assigned, or otherwise disposed of unless the instrument contains the mailing address of the grantee or assignee. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1970.

(3) This section shall not apply to wills or to statutory liens in favor of the Commonwealth.

(4) No county clerk shall receive, or permit the recording of, any instrument by which real estate, or any interest therein, is conveyed, granted, assigned, transferred, or otherwise disposed of unless the instrument complies with the official indexing system of the county. The indexing system shall have been in place for at least twenty-four (24) months prior to July 15, 1994 or shall be implemented for the purpose of allowing computerized searching for the instruments of record of the county clerk. If a county clerk requires a parcel identification number on an instrument before recording, the clerk shall provide a computer terminal, at no charge to the public, for use in finding the parcel identification number. The county clerk may make reasonable rules about the use of the computer terminal, requests for a parcel identification number, or both.

(5) The receipt for record and recording of any instrument by the county clerk without compliance with the provisions of this section shall not prevent the record of filing of the instrument from becoming notice as otherwise provided by law, nor impair the admissibility of the record as evidence.

382.365 Release of lien, with notice to property owner, within thirty days of satisfaction — Assignments of liens — Proceeding against lienholder in District Court or Circuit Court — Liability of lienholder when lien not released or notice not sent — Notice to state or lienholder — Damages.

(1) A holder of a lien on real property, including a lien provided for in KRS 376.010, shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

(2) An assignee of a lien on real property shall record the assignment in the county clerk's office as required by KRS 382.360. Failure of an assignee to record a mortgage assignment shall not affect the validity or perfection, or invalidity or lack of perfection, of a mortgage lien under applicable law.

(3) A proceeding may be filed by any owner of real property or any party acquiring an interest in the real property in District Court or Circuit Court against a lienholder that violates subsection (1) or (2) of this section. A proceeding filed under this section shall be given precedence over other matters pending before the court.

(4) Upon proof to the court of the lien being satisfied by payment in full to the final lienholder or final assignee, the court shall enter a judgment noting the identity of the final lienholder or final assignee and authorizing and directing the master commissioner of the court to execute and file with the county clerk the requisite release or assignments or both, as appropriate. The judgment shall be with costs including a reasonable attorney's fee. If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property or to a party with an interest in the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. This written notice shall be properly addressed and sent by certified mail or delivered in person to the final lienholder or final assignee as follows:

(a) For a corporation, to an officer at the lienholder's principal address or to an agent for process located in Kentucky; however, if the corporation is a foreign corporation and has not appointed an agent for process in Kentucky, then to the agent for process in the state of domicile of the corporation;

(b) For an individual, to the individual at the address shown on the mortgage, at the lienholder's residence or place of business, or at an address to which the lienholder has directed that correspondence or payoff be sent;

(c) For a trust or an estate, to a fiduciary at the address shown on the mortgage or at an address to which the lienholder has directed that correspondence or payoff be sent; and

(d) For any other entity, including but not limited to limited liability companies, partnerships, limited partnerships, limited liability partnerships, and associations, to an officer, partner, or member at the entity's principal place of business or to an agent for process.

(5) A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property or to a party with an interest in the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner or a party with an interest in the real property in securing the release of real property by such violation and in securing an award of damages. Damages under this subsection for failure to record an assignment pursuant to KRS 382.360(3) shall not exceed three (3) times the actual damages, plus attorney's fees and court costs, but in no event less than five hundred dollars ($500).

(6) The former holder of a lien on real property shall send by regular mail a copy of the lien release to the property owner at his or her last known address within seven (7) days of the release. A former lienholder that violates this subsection shall be liable to the owner of the real property for fifty dollars ($50) and any actual expense incurred by the owner in obtaining documentation of the lien release.

(7) For the purposes of this section, “date of satisfaction” means that date of receipt by a holder of a lien on real property of a sum of money in the form of a certified check, cashier's check, wired transferred funds, or other form of payment satisfactory to the lienholder that is sufficient to pay the principal, interest, and other costs owing on the obligation that is secured by the lien on the property.

(8) The provisions of this section shall not apply when a lienholder is deceased and the estate of the lienholder has not been settled.

(9) The state licensing agency, if applicable, or any holder of a lien on real property shall be notified of the disposition of any actions brought under this section against the lienholder.

(10) The provisions of this section shall be held and construed as ancillary and supplemental to any other remedy provided by law.

(11) If more than one (1) owner or party with an interest in the real property brings an action to recover damages under this section, any statutory damages shall be allocated equally among recovering parties in the absence of agreement otherwise among said parties. The entry of a judgment awarding damages shall bar a subsequent action by any other person or entity to recover damages for the same violation.