- US Legal Forms

- Waiver and Release Forms

-

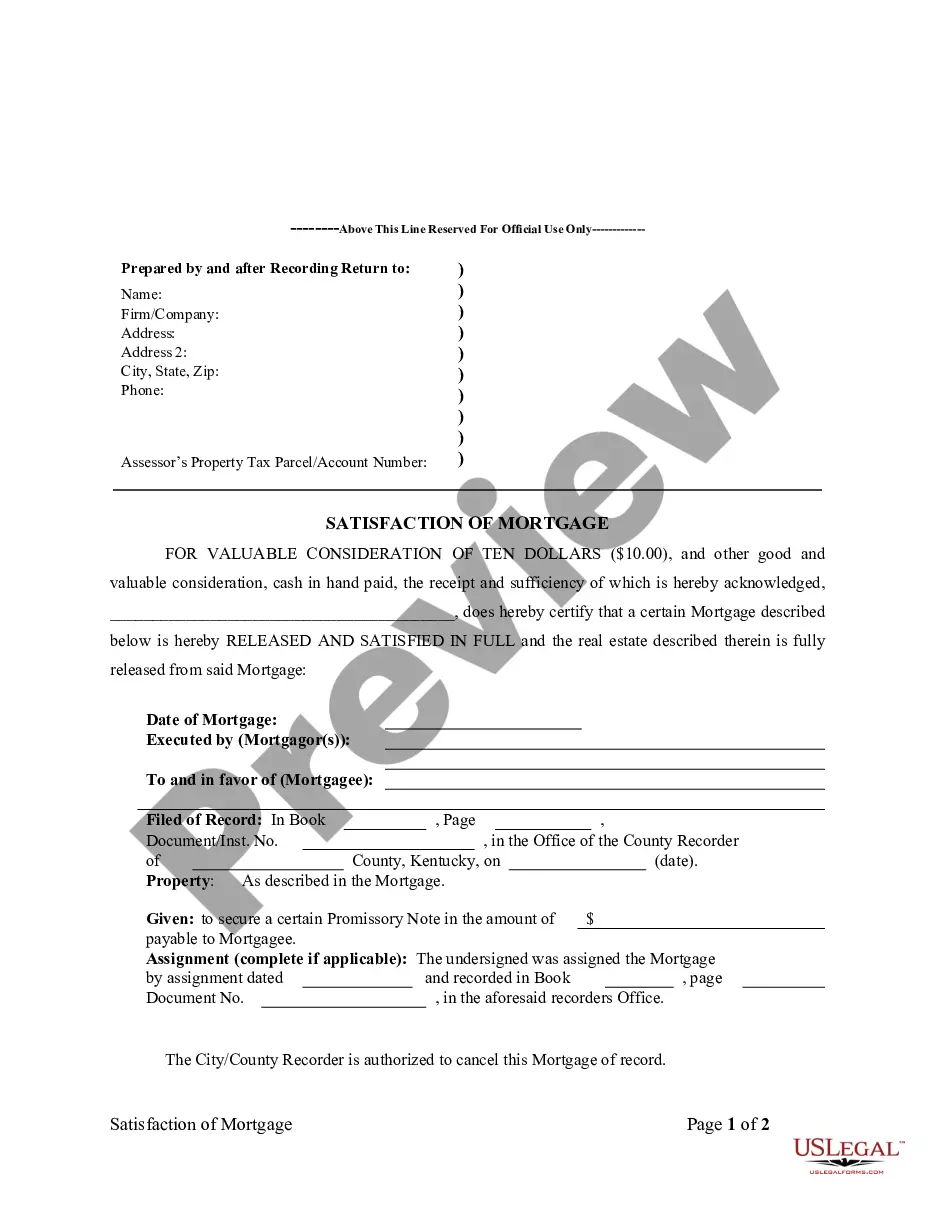

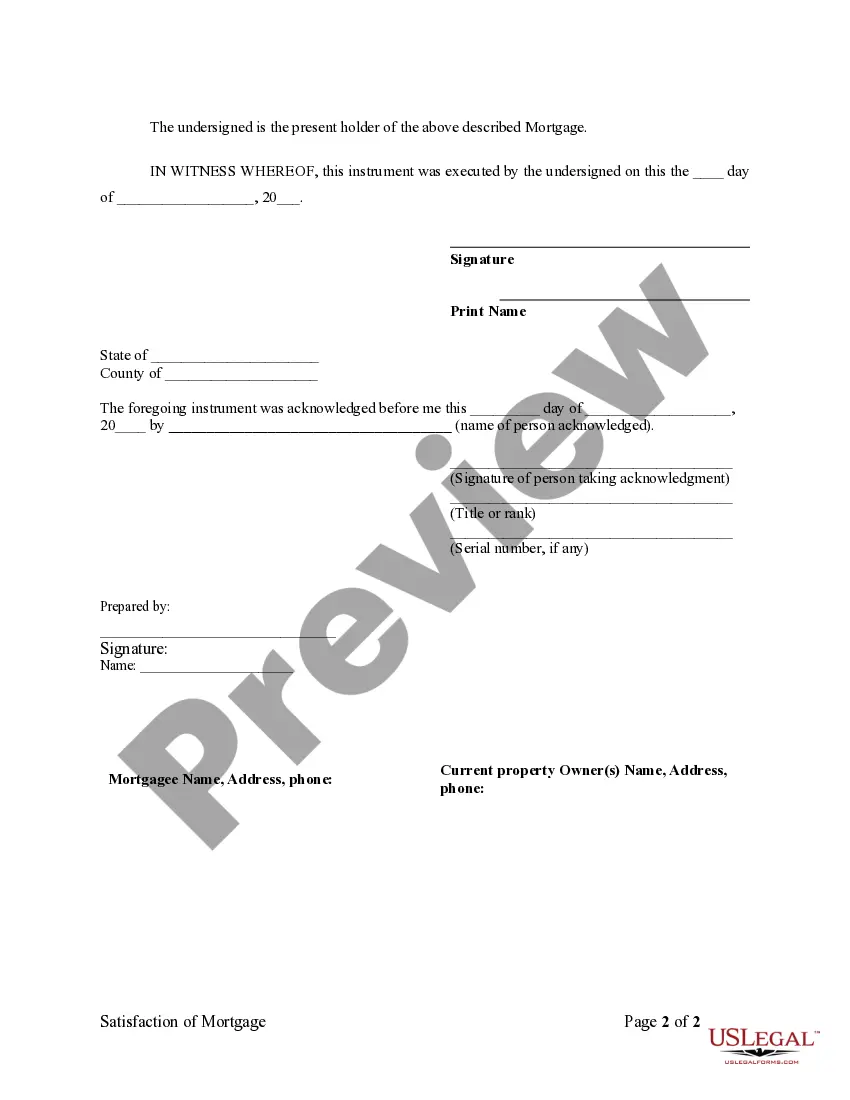

Kentucky Satisfaction...

Kentucky Release Mortgage Foreclosure

Description Mortgagee Released Prepared

Released Mortgagor Valuable Related forms

View Montana vehicle bill of sale with promissory note template

View Nebraska promissory note form

View Negotiable promissory note withdrawal

View Nevada promissory note no interest template form

View Nevada promissory note no interest template with calculator

How to fill out Mortgagee Parcel Valuable?

What is the most trustworthy service to obtain the Kentucky Release Mortgage Foreclosure and other recent iterations of legal documents.

US Legal Forms is the solution! It boasts the most comprehensive assortment of legal papers for any purpose.

If you haven't yet created an account with our library, follow these steps to get one: Form compliance review. Prior to acquiring any template, ensure it meets your usage requirements and complies with your state or county's regulations. Review the form details and utilize the Preview if offered. Alternative document search. Should there be any discrepancies, employ the search function in the header to find a different template. Click Buy Now to select the appropriate one. Account creation and subscription purchase. Choose the pricing plan that works best for you, Log In or set up your account, and process your subscription payment via PayPal or credit card. Obtaining the documents. Choose the format you wish to save the Kentucky Release Mortgage Foreclosure (PDF or DOCX) and click Download to retrieve it. US Legal Forms is an excellent option for anyone needing to manage legal documentation. Premium users receive even more benefits as they can complete and sign previously saved documents electronically at any time using the built-in PDF editor. Explore it today!

- Each template is meticulously crafted and confirmed for adherence to federal and local laws.

- They are categorized by industry and state of application, making it easy to find what you require.

- Experienced platform users merely need to Log In to the system, verify their subscription status, and click the Download button next to the Kentucky Release Mortgage Foreclosure to access it.

- Once stored, the template is accessible for future use within the My documents section of your account.

Inst Mortgagor Secure Form Rating

Inst Satisfied Promissory Form popularity

Assessor Mortgagee Released Other Form Names

Mortgagee Satisfied Favor FAQ

In Kentucky, foreclosures go through a judicial process, meaning foreclosures are handled by the courts. When it is determined that a borrower is in default on a loan, the lender files a foreclosure suit with the circuit court.

It takes approximately 5 months to foreclose on a Kentucky property. That process may be lengthened if the borrower contests the foreclosure or it may be shortened if the borrower abandons the property during the foreclosure process.

Under Kentucky law, the new owner from the foreclosure sale gets the right to possess the property after ten days' notice to the former owners. Then, the purchaser can get a writ of possession from the court.

Kentucky is a judicial foreclosure state and a lawsuit must be filed by a licensed attorney for any corporation to foreclose on a mortgage. Typically the mortgage will be about 6 months overdue when the homeowner is served with foreclosure.

Kentucky Release Mortgage Foreclosure Related Searches

-

ky mortgage release

-

kentucky foreclosure timeline

-

foreclosure process in kentucky

-

can banks foreclosures during covid-19

-

kentucky foreclosure statute of limitations

-

how long does it take before a house goes into foreclosure

-

foreclosure in kentucky

-

krs 426

-

kentucky foreclosure timeline

-

kentucky foreclosure statute

-

can banks foreclosures during covid-19

-

kentucky foreclosure statute of limitations

Mortgagee Parcel Valuable Interesting Questions

Mortgage foreclosure is a legal process in which a lender takes ownership of a property due to the borrower's failure to make mortgage payments.

Yes, you may be able to stop a mortgage foreclosure in Kentucky by negotiating with the lender, filing for bankruptcy, or seeking legal assistance.

You can try to negotiate with your lender by discussing loan modification options, such as refinancing, repayment plans, or forbearance agreements.

As a borrower, you have the right to receive notice of the foreclosure process, redeem your property before the sale, and potentially contest the foreclosure in court.

The redemption period in Kentucky is the length of time given to the homeowner after the foreclosure sale to reclaim the property by paying the outstanding mortgage debt and associated costs.

While the foreclosure process is ongoing, you may not be immediately evicted. However, once the foreclosure is complete and ownership of the property transfers, eviction proceedings may take place.

It is highly recommended to seek legal advice if you are facing a mortgage foreclosure in Kentucky. An attorney can guide you through the legal process, explain your rights, and help you explore available options.

Filing for bankruptcy can temporarily halt the foreclosure process through an automatic stay, giving you some time to sort out your financial situation. However, it is essential to consult with a bankruptcy attorney to understand the implications and determine the best course of action.

Yes, there are alternatives to foreclosure, such as loan modification, short sale, deed in lieu of foreclosure, and state-specific foreclosure prevention programs. Exploring these options with your lender or a housing counselor is advisable.

In Kentucky, you can seek assistance from HUD-approved housing counseling agencies, legal aid organizations, or consult the Kentucky Department of Financial Institutions for guidance and resources related to mortgage foreclosure.

More info

Mortgagee Released Mortgage Trusted and secure by over 3 million people of the world’s leading companies

-

No results found.

-

Kentucky

-

Alabama

-

Alaska

-

Arizona

-

Arkansas

-

California

-

Colorado

-

Connecticut

-

Delaware

-

District of Columbia

-

Florida

-

Georgia

-

Hawaii

-

Idaho

-

Illinois

-

Indiana

-

Iowa

-

Kansas

-

Louisiana

-

Maine

-

Maryland

-

Massachusetts

-

Michigan

-

Minnesota

-

Mississippi

-

Missouri

-

Montana

-

Nebraska

-

Nevada

-

New Hampshire

-

New Jersey

-

New Mexico

-

New York

-

North Carolina

-

North Dakota

-

Ohio

-

Oklahoma

-

Oregon

-

Pennsylvania

-

Rhode Island

-

South Carolina

-

South Dakota

-

Tennessee

-

Texas

-

Utah

-

Vermont

-

Virginia

-

Washington

-

West Virginia

-

Wisconsin

-

Wyoming

Assignments Generally: Lenders, or holders of mortgages or deeds of trust, often assign mortgages or deeds of trust to other lenders, or third parties. When this is done the assignee (person who received the assignment) steps into the place of the original lender or assignor. To effectuate an assignment, the general rules is that the assignment must be in proper written format and recorded to provide notice of the assignment.

Satisfactions Generally: Once a mortgage or deed of trust is paid, the holder of the mortgage is required to satisfy the mortgage or deed of trust of record to show that the mortgage or deed of trust is no longer a lien on the property. The general rule is that the satisfaction must be in proper written format and recorded to provide notice of the satisfaction. If the lender fails to record a satisfaction within set time limits, the lender may be responsible for damages set by statute for failure to timely cancel the lien. Depending on your state, a satisfaction may be called a Satisfaction, Cancellation, or Reconveyance. Some states still recognize marginal satisfaction but this is slowly being phased out. A marginal satisfaction is where the holder of the mortgage physically goes to the recording office and enters a satisfaction on the face of the the recorded mortgage, which is attested by the clerk.

Kentucky Law

Execution of Assignment or Satisfaction: Must be signed by the mortgagee.

Assignment: An assignment must be in writing and recorded.

Demand to Satisfy: Written demand required. See below, Penalty.

Recording Satisfaction: A holder of a lien on real property shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

Marginal Satisfaction: Not allowed.

Penalty: If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner in securing the release of real property by such violation.

Acknowledgment: An assignment or satisfaction must contain a proper Kentucky acknowledgment, or other acknowledgment approved by Statute.

Kentucky Statutes

382.290 Recording of mortgages and deeds retaining liens -- Assignment -- Discharge -- Form of record -- Clerk's fee.

(1) In recording mortgages and deeds in which liens are retained (except railroad mortgages securing bonds payable to bearer), there shall be left a blank space immediately after the record of the deed or mortgage of at least two (2) full lines for each note or obligation named in the deed or mortgage, or in the alternative, at the option of the county clerk, a marginal entry record may be kept for the same purposes as the blank space. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instruments.(2) No county clerk or deputy county clerk shall admit to record any mortgage or deed in which liens are retained unless the mortgage or deed in which a lien is retained plainly specifies and refers to the immediate source from which the mortgagor or grantor derived title to the property or the interest encumbered therein.

(3) When any note named in any deed or mortgage is assigned to any other person, the assignor may, over his own hand, attested by the clerk, note such assignment in the blank space, or in a marginal entry record, beside a listing of the book and page of the document being assigned, and when any one (1) or more of the notes named in any deed or mortgage is paid, or otherwise released or satisfied, the holder of the note, and who appears from the record to be such holder, may release the lien, so far as such note is concerned, by release, over his own hand, attested by the clerk. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instrument.

(4) No person who does not, from such record or assignment of record, appear at the time to be the legal holder of any note secured by lien in any deed or mortgage, shall be permitted to release the lien securing any such note, and any release made in contravention of this section shall be void; but this section does not change the existing law if no such entry is made.

(5) For each assignment and release so made and attested by the clerk, he may charge a fee pursuant to KRS 64.012 to be paid by the person executing the release or noting the assignment.

(6) If such assignment of a note is made by separate instrument or by deed assigning the note, or in a marginal entry record, the instrument of writing or deed or marginal entry record shall set forth the date of notes assigned, a brief description of notes, the name and post office address of assignee, and the deed book and page of the instrument wherein the lien or mortgage is recorded and the clerk or deputy clerk receiving such instrument of writing or deed of assignment for record shall at the option of the county clerk immediately either link the assignment and its filing location to its respective referenced instrument in the indexing system for the referenced instrument, or endorse at the foot of the record in the space provided in subsection (1) of this section, "The notes mentioned herein (giving a brief description of notes assigned) have been transferred and assigned to (insert name and address of assignee) by deed of assignment (or describe instrument) dated and recorded in deed book .... page ....," and attest such certificate. For making such notation on the record the clerk shall be allowed a fee pursuant to KRS 64.012 for each notation so made, to be paid by the party filing the instrument of writing or deed of assignment.

(7) No holder of a note secured by lien retained in either deed or mortgage shall lodge for record, and no clerk or deputy clerk shall receive and permit to be lodged for record, any deed or instrument of writing that does not comply with the provisions of this section.

382.335 Certain information to be included in instruments in order for them to be recorded.

(1) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or personal property, or any interest therein or lien thereon, is conveyed, granted, encumbered, assigned, or otherwise disposed of; nor receive any instrument or permit any instrument, provided by law, to be recorded as evidence of title to real estate, unless the instrument has endorsed on it, a printed, typewritten, or stamped statement showing the name and address of the individual who prepared the instrument, and the statement is signed by the individual. The person who prepared the instrument may execute his or her signature by affixing a facsimile of his or her signature on the instrument. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1962.(2) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or any interest therein is conveyed, granted, assigned, or otherwise disposed of unless the instrument contains the mailing address of the grantee or assignee. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1970.

(3) This section shall not apply to wills or to statutory liens in favor of the Commonwealth.

(4) No county clerk shall receive, or permit the recording of, any instrument by which real estate, or any interest therein, is conveyed, granted, assigned, transferred, or otherwise disposed of unless the instrument complies with the official indexing system of the county. The indexing system shall have been in place for at least twenty-four (24) months prior to July 15, 1994 or shall be implemented for the purpose of allowing computerized searching for the instruments of record of the county clerk. If a county clerk requires a parcel identification number on an instrument before recording, the clerk shall provide a computer terminal, at no charge to the public, for use in finding the parcel identification number. The county clerk may make reasonable rules about the use of the computer terminal, requests for a parcel identification number, or both.

(5) The receipt for record and recording of any instrument by the county clerk without compliance with the provisions of this section shall not prevent the record of filing of the instrument from becoming notice as otherwise provided by law, nor impair the admissibility of the record as evidence.

382.365 Release of lien, with notice to property owner, within thirty days of satisfaction — Assignments of liens — Proceeding against lienholder in District Court or Circuit Court — Liability of lienholder when lien not released or notice not sent — Notice to state or lienholder — Damages.

(1) A holder of a lien on real property, including a lien provided for in KRS 376.010, shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

(2) An assignee of a lien on real property shall record the assignment in the county clerk's office as required by KRS 382.360. Failure of an assignee to record a mortgage assignment shall not affect the validity or perfection, or invalidity or lack of perfection, of a mortgage lien under applicable law.

(3) A proceeding may be filed by any owner of real property or any party acquiring an interest in the real property in District Court or Circuit Court against a lienholder that violates subsection (1) or (2) of this section. A proceeding filed under this section shall be given precedence over other matters pending before the court.

(4) Upon proof to the court of the lien being satisfied by payment in full to the final lienholder or final assignee, the court shall enter a judgment noting the identity of the final lienholder or final assignee and authorizing and directing the master commissioner of the court to execute and file with the county clerk the requisite release or assignments or both, as appropriate. The judgment shall be with costs including a reasonable attorney's fee. If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property or to a party with an interest in the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. This written notice shall be properly addressed and sent by certified mail or delivered in person to the final lienholder or final assignee as follows:

(a) For a corporation, to an officer at the lienholder's principal address or to an agent for process located in Kentucky; however, if the corporation is a foreign corporation and has not appointed an agent for process in Kentucky, then to the agent for process in the state of domicile of the corporation;

(b) For an individual, to the individual at the address shown on the mortgage, at the lienholder's residence or place of business, or at an address to which the lienholder has directed that correspondence or payoff be sent;

(c) For a trust or an estate, to a fiduciary at the address shown on the mortgage or at an address to which the lienholder has directed that correspondence or payoff be sent; and

(d) For any other entity, including but not limited to limited liability companies, partnerships, limited partnerships, limited liability partnerships, and associations, to an officer, partner, or member at the entity's principal place of business or to an agent for process.

(5) A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property or to a party with an interest in the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner or a party with an interest in the real property in securing the release of real property by such violation and in securing an award of damages. Damages under this subsection for failure to record an assignment pursuant to KRS 382.360(3) shall not exceed three (3) times the actual damages, plus attorney's fees and court costs, but in no event less than five hundred dollars ($500).

(6) The former holder of a lien on real property shall send by regular mail a copy of the lien release to the property owner at his or her last known address within seven (7) days of the release. A former lienholder that violates this subsection shall be liable to the owner of the real property for fifty dollars ($50) and any actual expense incurred by the owner in obtaining documentation of the lien release.

(7) For the purposes of this section, “date of satisfaction” means that date of receipt by a holder of a lien on real property of a sum of money in the form of a certified check, cashier's check, wired transferred funds, or other form of payment satisfactory to the lienholder that is sufficient to pay the principal, interest, and other costs owing on the obligation that is secured by the lien on the property.

(8) The provisions of this section shall not apply when a lienholder is deceased and the estate of the lienholder has not been settled.

(9) The state licensing agency, if applicable, or any holder of a lien on real property shall be notified of the disposition of any actions brought under this section against the lienholder.

(10) The provisions of this section shall be held and construed as ancillary and supplemental to any other remedy provided by law.

(11) If more than one (1) owner or party with an interest in the real property brings an action to recover damages under this section, any statutory damages shall be allocated equally among recovering parties in the absence of agreement otherwise among said parties. The entry of a judgment awarding damages shall bar a subsequent action by any other person or entity to recover damages for the same violation.

Assignments Generally: Lenders, or holders of mortgages or deeds of trust, often assign mortgages or deeds of trust to other lenders, or third parties. When this is done the assignee (person who received the assignment) steps into the place of the original lender or assignor. To effectuate an assignment, the general rules is that the assignment must be in proper written format and recorded to provide notice of the assignment.

Satisfactions Generally: Once a mortgage or deed of trust is paid, the holder of the mortgage is required to satisfy the mortgage or deed of trust of record to show that the mortgage or deed of trust is no longer a lien on the property. The general rule is that the satisfaction must be in proper written format and recorded to provide notice of the satisfaction. If the lender fails to record a satisfaction within set time limits, the lender may be responsible for damages set by statute for failure to timely cancel the lien. Depending on your state, a satisfaction may be called a Satisfaction, Cancellation, or Reconveyance. Some states still recognize marginal satisfaction but this is slowly being phased out. A marginal satisfaction is where the holder of the mortgage physically goes to the recording office and enters a satisfaction on the face of the the recorded mortgage, which is attested by the clerk.

Kentucky Law

Execution of Assignment or Satisfaction: Must be signed by the mortgagee.

Assignment: An assignment must be in writing and recorded.

Demand to Satisfy: Written demand required. See below, Penalty.

Recording Satisfaction: A holder of a lien on real property shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

Marginal Satisfaction: Not allowed.

Penalty: If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner in securing the release of real property by such violation.

Acknowledgment: An assignment or satisfaction must contain a proper Kentucky acknowledgment, or other acknowledgment approved by Statute.

Kentucky Statutes

382.290 Recording of mortgages and deeds retaining liens -- Assignment -- Discharge -- Form of record -- Clerk's fee.

(1) In recording mortgages and deeds in which liens are retained (except railroad mortgages securing bonds payable to bearer), there shall be left a blank space immediately after the record of the deed or mortgage of at least two (2) full lines for each note or obligation named in the deed or mortgage, or in the alternative, at the option of the county clerk, a marginal entry record may be kept for the same purposes as the blank space. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instruments.(2) No county clerk or deputy county clerk shall admit to record any mortgage or deed in which liens are retained unless the mortgage or deed in which a lien is retained plainly specifies and refers to the immediate source from which the mortgagor or grantor derived title to the property or the interest encumbered therein.

(3) When any note named in any deed or mortgage is assigned to any other person, the assignor may, over his own hand, attested by the clerk, note such assignment in the blank space, or in a marginal entry record, beside a listing of the book and page of the document being assigned, and when any one (1) or more of the notes named in any deed or mortgage is paid, or otherwise released or satisfied, the holder of the note, and who appears from the record to be such holder, may release the lien, so far as such note is concerned, by release, over his own hand, attested by the clerk. Each entry in the marginal entry record shall be linked to its respective referenced instrument in the indexing system for the referenced instrument.

(4) No person who does not, from such record or assignment of record, appear at the time to be the legal holder of any note secured by lien in any deed or mortgage, shall be permitted to release the lien securing any such note, and any release made in contravention of this section shall be void; but this section does not change the existing law if no such entry is made.

(5) For each assignment and release so made and attested by the clerk, he may charge a fee pursuant to KRS 64.012 to be paid by the person executing the release or noting the assignment.

(6) If such assignment of a note is made by separate instrument or by deed assigning the note, or in a marginal entry record, the instrument of writing or deed or marginal entry record shall set forth the date of notes assigned, a brief description of notes, the name and post office address of assignee, and the deed book and page of the instrument wherein the lien or mortgage is recorded and the clerk or deputy clerk receiving such instrument of writing or deed of assignment for record shall at the option of the county clerk immediately either link the assignment and its filing location to its respective referenced instrument in the indexing system for the referenced instrument, or endorse at the foot of the record in the space provided in subsection (1) of this section, "The notes mentioned herein (giving a brief description of notes assigned) have been transferred and assigned to (insert name and address of assignee) by deed of assignment (or describe instrument) dated and recorded in deed book .... page ....," and attest such certificate. For making such notation on the record the clerk shall be allowed a fee pursuant to KRS 64.012 for each notation so made, to be paid by the party filing the instrument of writing or deed of assignment.

(7) No holder of a note secured by lien retained in either deed or mortgage shall lodge for record, and no clerk or deputy clerk shall receive and permit to be lodged for record, any deed or instrument of writing that does not comply with the provisions of this section.

382.335 Certain information to be included in instruments in order for them to be recorded.

(1) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or personal property, or any interest therein or lien thereon, is conveyed, granted, encumbered, assigned, or otherwise disposed of; nor receive any instrument or permit any instrument, provided by law, to be recorded as evidence of title to real estate, unless the instrument has endorsed on it, a printed, typewritten, or stamped statement showing the name and address of the individual who prepared the instrument, and the statement is signed by the individual. The person who prepared the instrument may execute his or her signature by affixing a facsimile of his or her signature on the instrument. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1962.(2) No county clerk shall receive or permit the recording of any instrument by which the title to real estate or any interest therein is conveyed, granted, assigned, or otherwise disposed of unless the instrument contains the mailing address of the grantee or assignee. This subsection shall not apply to any instrument executed or acknowledged prior to July 1, 1970.

(3) This section shall not apply to wills or to statutory liens in favor of the Commonwealth.

(4) No county clerk shall receive, or permit the recording of, any instrument by which real estate, or any interest therein, is conveyed, granted, assigned, transferred, or otherwise disposed of unless the instrument complies with the official indexing system of the county. The indexing system shall have been in place for at least twenty-four (24) months prior to July 15, 1994 or shall be implemented for the purpose of allowing computerized searching for the instruments of record of the county clerk. If a county clerk requires a parcel identification number on an instrument before recording, the clerk shall provide a computer terminal, at no charge to the public, for use in finding the parcel identification number. The county clerk may make reasonable rules about the use of the computer terminal, requests for a parcel identification number, or both.

(5) The receipt for record and recording of any instrument by the county clerk without compliance with the provisions of this section shall not prevent the record of filing of the instrument from becoming notice as otherwise provided by law, nor impair the admissibility of the record as evidence.

382.365 Release of lien, with notice to property owner, within thirty days of satisfaction — Assignments of liens — Proceeding against lienholder in District Court or Circuit Court — Liability of lienholder when lien not released or notice not sent — Notice to state or lienholder — Damages.

(1) A holder of a lien on real property, including a lien provided for in KRS 376.010, shall release the lien in the county clerk's office where the lien is recorded within thirty (30) days from the date of satisfaction.

(2) An assignee of a lien on real property shall record the assignment in the county clerk's office as required by KRS 382.360. Failure of an assignee to record a mortgage assignment shall not affect the validity or perfection, or invalidity or lack of perfection, of a mortgage lien under applicable law.

(3) A proceeding may be filed by any owner of real property or any party acquiring an interest in the real property in District Court or Circuit Court against a lienholder that violates subsection (1) or (2) of this section. A proceeding filed under this section shall be given precedence over other matters pending before the court.

(4) Upon proof to the court of the lien being satisfied by payment in full to the final lienholder or final assignee, the court shall enter a judgment noting the identity of the final lienholder or final assignee and authorizing and directing the master commissioner of the court to execute and file with the county clerk the requisite release or assignments or both, as appropriate. The judgment shall be with costs including a reasonable attorney's fee. If the court finds that the lienholder received written notice of its failure to release and lacked good cause for not releasing the lien, the lienholder shall be liable to the owner of the real property or to a party with an interest in the real property in the amount of one hundred dollars ($100) per day for each day, beginning on the fifteenth day after receipt of the written notice, of the violation for which good cause did not exist. This written notice shall be properly addressed and sent by certified mail or delivered in person to the final lienholder or final assignee as follows:

(a) For a corporation, to an officer at the lienholder's principal address or to an agent for process located in Kentucky; however, if the corporation is a foreign corporation and has not appointed an agent for process in Kentucky, then to the agent for process in the state of domicile of the corporation;

(b) For an individual, to the individual at the address shown on the mortgage, at the lienholder's residence or place of business, or at an address to which the lienholder has directed that correspondence or payoff be sent;

(c) For a trust or an estate, to a fiduciary at the address shown on the mortgage or at an address to which the lienholder has directed that correspondence or payoff be sent; and

(d) For any other entity, including but not limited to limited liability companies, partnerships, limited partnerships, limited liability partnerships, and associations, to an officer, partner, or member at the entity's principal place of business or to an agent for process.

(5) A lienholder that continues to fail to release a satisfied real estate lien, without good cause, within forty-five (45) days from the date of written notice shall be liable to the owner of the real property or to a party with an interest in the real property for an additional four hundred dollars ($400) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice, for a total of five hundred dollars ($500) per day for each day for which good cause did not exist after the forty-fifth day from the date of written notice. The lienholder shall also be liable for any actual expense including a reasonable attorney's fee incurred by the owner or a party with an interest in the real property in securing the release of real property by such violation and in securing an award of damages. Damages under this subsection for failure to record an assignment pursuant to KRS 382.360(3) shall not exceed three (3) times the actual damages, plus attorney's fees and court costs, but in no event less than five hundred dollars ($500).

(6) The former holder of a lien on real property shall send by regular mail a copy of the lien release to the property owner at his or her last known address within seven (7) days of the release. A former lienholder that violates this subsection shall be liable to the owner of the real property for fifty dollars ($50) and any actual expense incurred by the owner in obtaining documentation of the lien release.

(7) For the purposes of this section, “date of satisfaction” means that date of receipt by a holder of a lien on real property of a sum of money in the form of a certified check, cashier's check, wired transferred funds, or other form of payment satisfactory to the lienholder that is sufficient to pay the principal, interest, and other costs owing on the obligation that is secured by the lien on the property.

(8) The provisions of this section shall not apply when a lienholder is deceased and the estate of the lienholder has not been settled.

(9) The state licensing agency, if applicable, or any holder of a lien on real property shall be notified of the disposition of any actions brought under this section against the lienholder.

(10) The provisions of this section shall be held and construed as ancillary and supplemental to any other remedy provided by law.

(11) If more than one (1) owner or party with an interest in the real property brings an action to recover damages under this section, any statutory damages shall be allocated equally among recovering parties in the absence of agreement otherwise among said parties. The entry of a judgment awarding damages shall bar a subsequent action by any other person or entity to recover damages for the same violation.