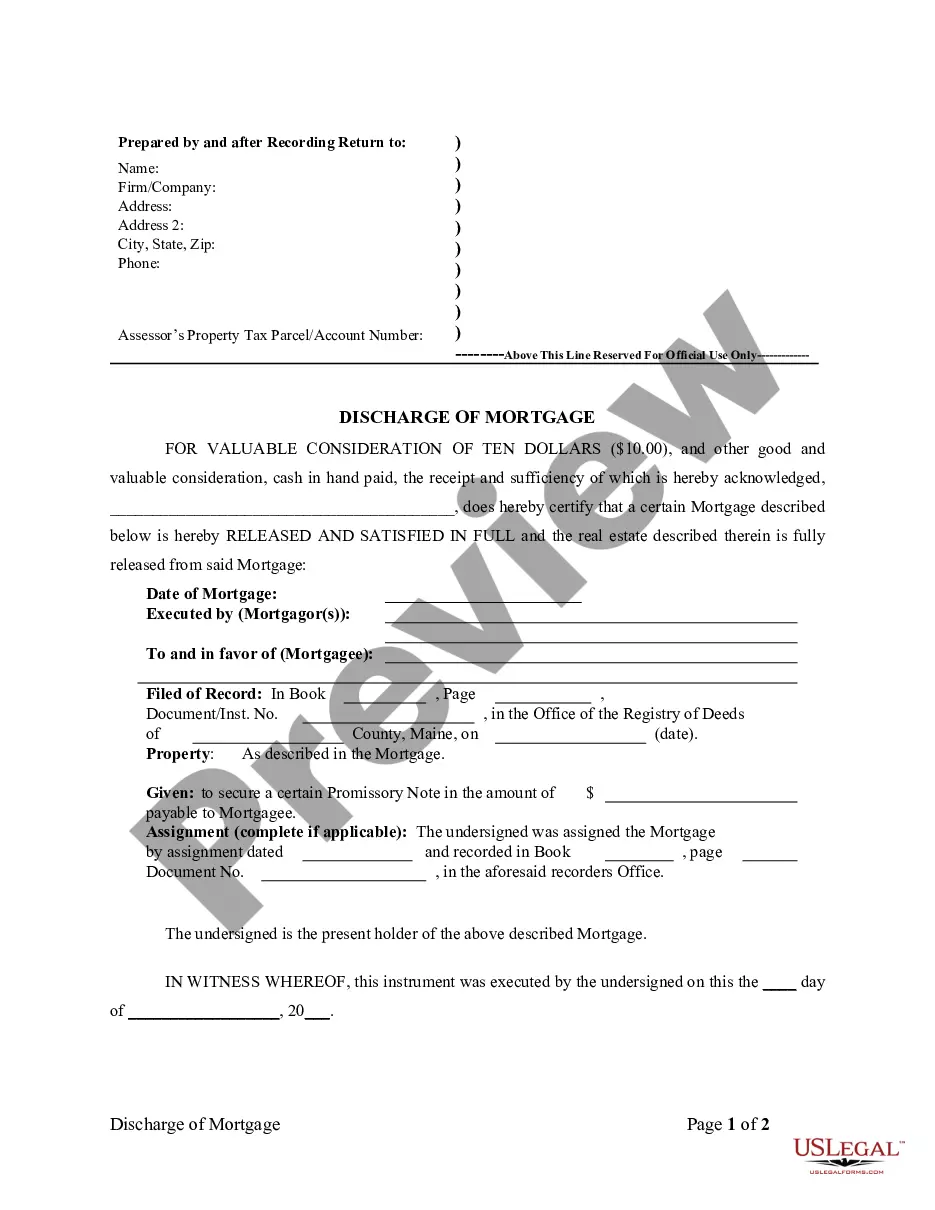

Satisfaction, Release or Cancellation of Mortgage by Individual

Assignments Generally: Lenders, or holders of mortgages or deeds of trust, often assign mortgages or deeds of trust to other lenders, or third parties. When this is done the assignee (person who received the assignment) steps into the place of the original lender or assignor. To effectuate an assignment, the general rules is that the assignment must be in proper written format and recorded to provide notice of the assignment.

Satisfactions Generally: Once a mortgage or deed of trust is paid, the holder of the mortgage is required to satisfy the mortgage or deed of trust of record to show that the mortgage or deed of trust is no longer a lien on the property. The general rule is that the satisfaction must be in proper written format and recorded to provide notice of the satisfaction. If the lender fails to record a satisfaction within set time limits, the lender may be responsible for damages set by statute for failure to timely cancel the lien. Depending on your state, a satisfaction may be called a Satisfaction, Cancellation, or Reconveyance. Some states still recognize marginal satisfaction but this is slowly being phased out. A marginal satisfaction is where the holder of the mortgage physically goes to the recording office and enters a satisfaction on the face of the the recorded mortgage, which is attested by the clerk.

Maine Law

Execution of Assignment or Satisfaction: Must be signed by the mortgagee.

Assignment: An assignment must be in writing and recorded.

Demand to Satisfy: None required. Mortgagee has 60 days from payoff of mortgage to record satisfaction or else suffer liability.

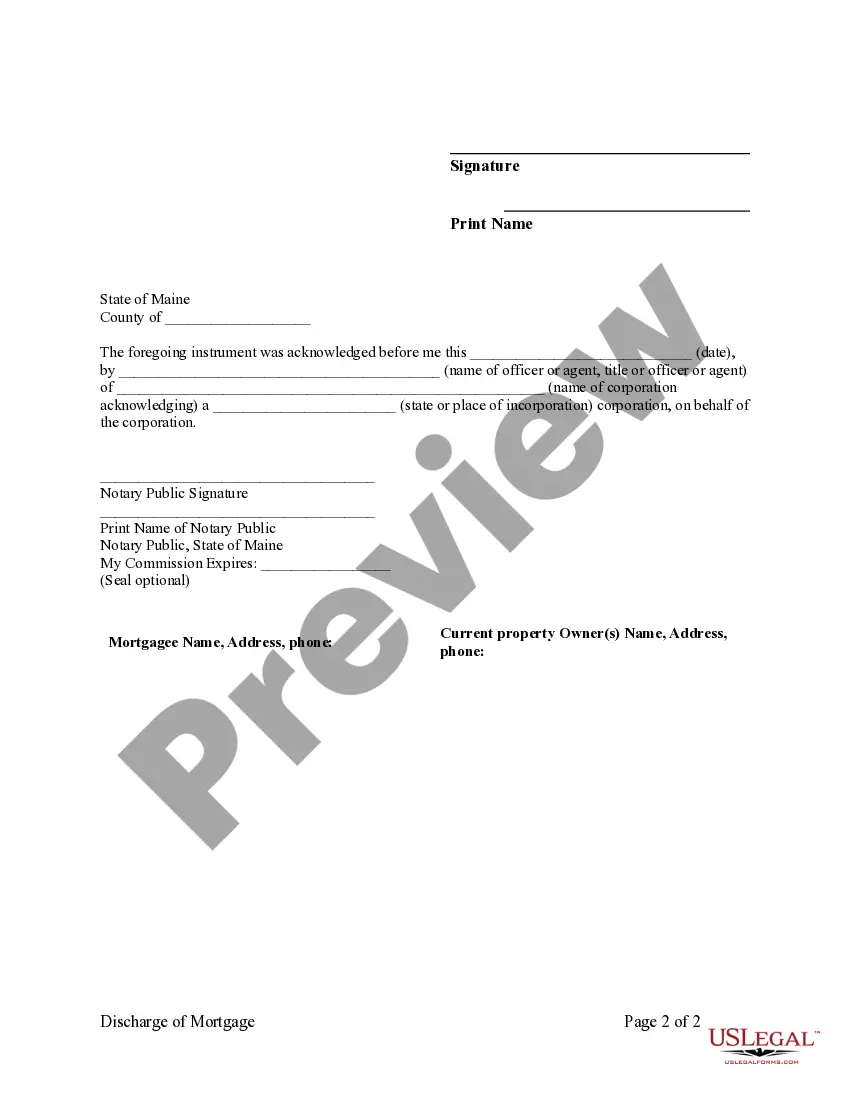

Recording Satisfaction: A mortgage only may be discharged by a written instrument acknowledging the satisfaction thereof and signed and acknowledged by the mortgagee or by the mortgagee's duly authorized officer or agent, personal representative or assignee.

Marginal Satisfaction: Not allowed. Satisfaction must be by separate written instrument.

Penalty: If a satisfied mortgage is not recorded as such by mortgagee within 60 days following satisfaction thereof, mortgagee becomes liable to aggreived parties for damages equal to exemplary damages of $200 per week after expiration of the 60 days, up to an aggregate maximum of $5,000 for all aggrieved parties or the actual loss sustained by the aggrieved party, whichever is greater, and attorney fees.

Acknowledgment: An assignment or satisfaction must contain a proper Maine acknowledgment, or other acknowledgment approved by Statute.

Maine Statutes

551. Entry on record; neglect to discharge

A mortgage only may be discharged by a written instrument acknowledging the satisfaction thereof and signed and acknowledged by the mortgagee or by the mortgagee's duly authorized officer or agent, personal representative or assignee. The instrument must recite the name or identity of the mortgagee and mortgagor, or their successors in interest and the record location of the mortgage discharged. The instrument, when recorded, has the same effect as a deed of release duly acknowledged and recorded. [1999, c. 230, 1 (AMD); 1999, c. 230, 2 (AFF).]

Within 60 days after full performance of the conditions of the mortgage, the mortgagee shall record a valid and complete release of mortgage together with any instrument of assignment necessary to establish the mortgagee's record ownership of the mortgage. Within 30 days after receiving the recorded release of the mortgage from the registry of deeds, the mortgagee shall send the release by first class mail to the mortgagorâ??s address as listed in the mortgage agreement or to an address specified in writing by the mortgagor for this purpose. As used in this paragraph, the term "mortgagee" means both the owner of the mortgage at the time it is satisfied and any servicer who receives the final payment satisfying the debt. If a release is not transmitted to the registry of deeds within 60 days, the owner and any such servicer are jointly and severally liable to an aggrieved party for damages equal to exemplary damages of $200 per week after expiration of the 60 days, up to an aggregate maximum of $5,000 for all aggrieved parties or the actual loss sustained by the aggrieved party, whichever is greater. If multiple aggrieved parties seek exemplary damages, the court shall equitably allocate the maximum amount. If the release is not sent by first class mail to the mortgagorâ??s address as listed in the mortgage agreement or to an address specified in writing by the mortgagor for this purpose within 30 days after receiving the recorded release, the mortgagee is liable to an aggrieved party for damages equal to exemplary damages of $500. The mortgagee is also liable for court costs and reasonable attorney's fees in any successful action to enforce the liability imposed under this paragraph. The mortgagee may charge the mortgagor for any recording fees incurred in recording the release of mortgage and any postage fees incurred in sending the release to the mortgagor. [2011, c. 146, 1 (AMD).]

With respect to a mortgage securing an open-end line of credit, the 60-day period to deliver a release commences after the mortgagor delivers to the address designated for payments under the line of credit a written request to terminate the line and the mortgage together with payment in full of all amounts secured by the mortgage. The mortgagee may designate in writing a different address for delivery of written notices under this paragraph. [1999, c. 230, 1 (NEW); 1999, c. 230, 2 (AFF).]

All discharges of recorded mortgages, attachments or liens of any nature must be recorded by a written instrument and, except for termination statements filed pursuant to Title 11, section 9-1513, acknowledged in same manner as other instruments presented for record and no such discharges may be permitted by entry in the margin of the instrument to be discharged. [1999, c. 699, Pt. D, 22 (AMD); 1999, c. 699, Pt. D, 30 (AFF).]

552. Validation

All marginal discharges of mortgages recorded prior to April 1, 1974, duly attested by the register of deeds as being recorded from discharge in margin of original mortgage, are validated and have the same effect as if made as provided in section 551. [1997, c. 103, 1 (AMD).]

553-A. Discharge by attorney

1. Affidavit. A recorded mortgage on a residential owner-occupied one-to-4-family dwelling may be discharged in the office of the registry of deeds by an attorney-at-law licensed to practice in the State if the mortgagee, after receipt of payment of the mortgage in accordance with the payoff statement furnished to the mortgagor by the mortgagee, fails to make that discharge or to execute and acknowledge a deed of release of the mortgage. The attorney shall execute and record an affidavit in the registry of deeds affirming that:

A. The affiant is an attorney-at-law in good standing and licensed to practice in the State; [1993, c. 534, §2 (NEW).]

B. The affidavit is made at the request of the mortgagor or the mortgagor’s executor, administrator, successor, assignee or transferee or the transferee’s mortgagee; [1993, c. 534, §2 (NEW).]

C. The mortgagee has provided a payoff statement with respect to the loan secured by the mortgage; [1993, c. 534, §2 (NEW).]

D. The mortgagee has received payment that has been proved by a bank check, certified check or attorney client funds account check negotiated by the mortgagee or by evidence of receipt of payment by the mortgagee; [1993, c. 534, §2 (NEW).]

E. More than 30 days have elapsed since the payment was received by the mortgagee; and [1993, c. 534, §2 (NEW).]

F. The mortgagee has received written notification by certified mail 15 days in advance, sent to the mortgagee’s last known address, that the affiant intends to execute and record an affidavit in accordance with this section, enclosing a copy of the proposed affidavit; the mortgagee has not delivered a discharge or deed of release in response to the notification; and the mortgagor has complied with any request made by the mortgagee for additional payment at least 15 days before the date of the affidavit. [1993, c. 534, §2 (NEW).]

[ 1993, c. 534, §2 (NEW) .]

2. Name; address; mortgagee; mortgagor. The affidavit must include the names and addresses of the mortgagor and the mortgagee, the date of the mortgage, the title reference and similar information with respect to recorded assignment of the mortgage.

[ 1993, c. 534, §2 (NEW) .]

3. Copy. The affiant shall attach to the affidavit the following, certifying that each copy is a true copy of the original document:

A. Photostatic copies of the documentary evidence that payment has been received by the mortgagee, including the mortgagee’s endorsement of a bank check, certified check or attorney client funds account check; and [1993, c. 534, §2 (NEW).]

B. A photostatic copy of the payoff statement if that statement is made in writing. [1993, c. 534, §2 (NEW).]

[ 1993, c. 534, §2 (NEW) .]

4. Effect. An affidavit recorded under this section has the same effect as a recorded discharge.

[ 1993, c. 534, §2 (NEW) .]

5. Exception. A mortgage may not be discharged as provided by this section if the holder of the mortgage at the time a discharge is sought is a financial institution or credit union authorized to do business in the State as defined in Title 9-B, section 131, subsection 12-A or 17-A.