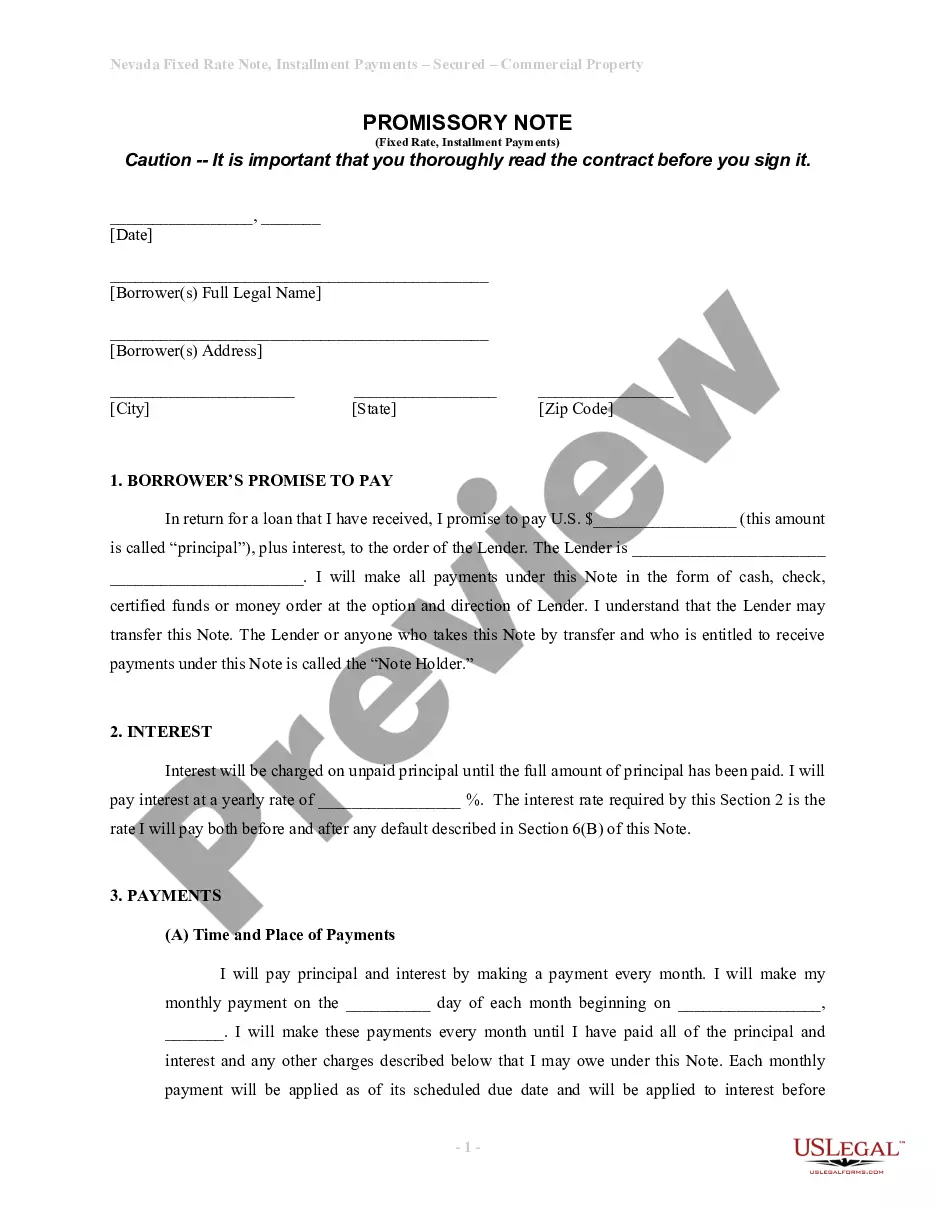

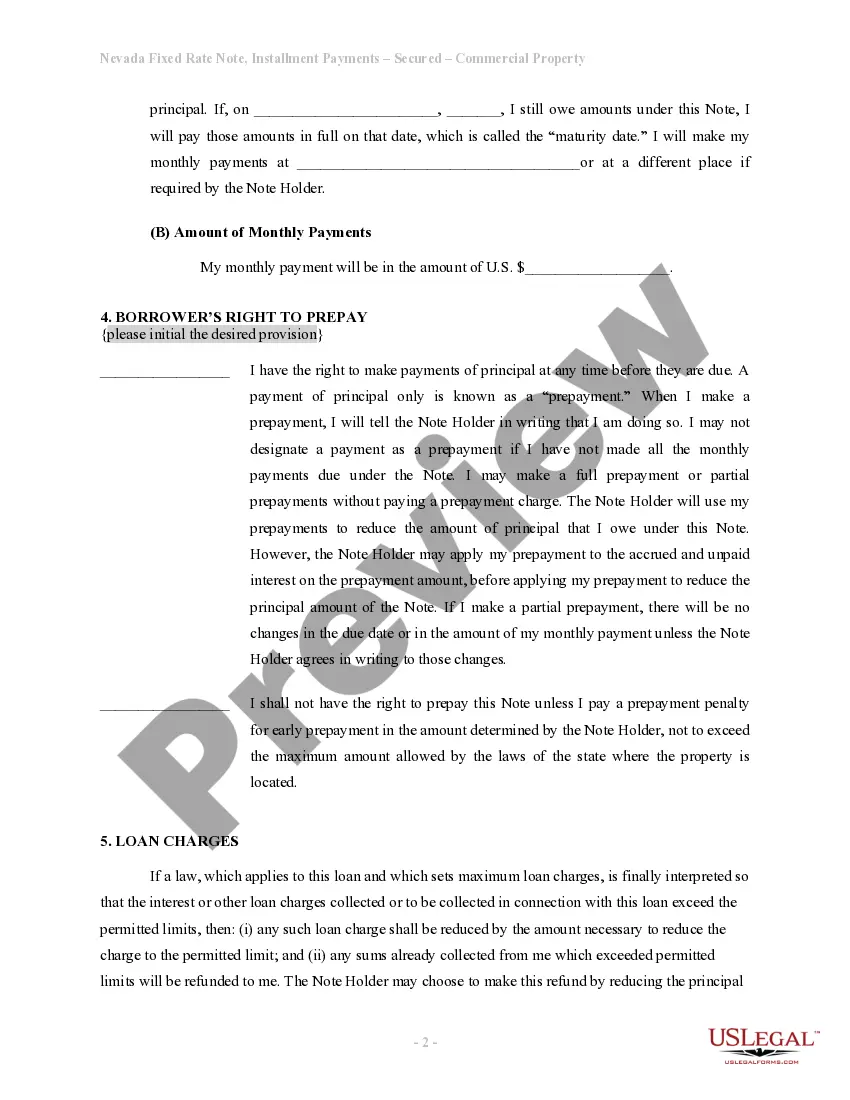

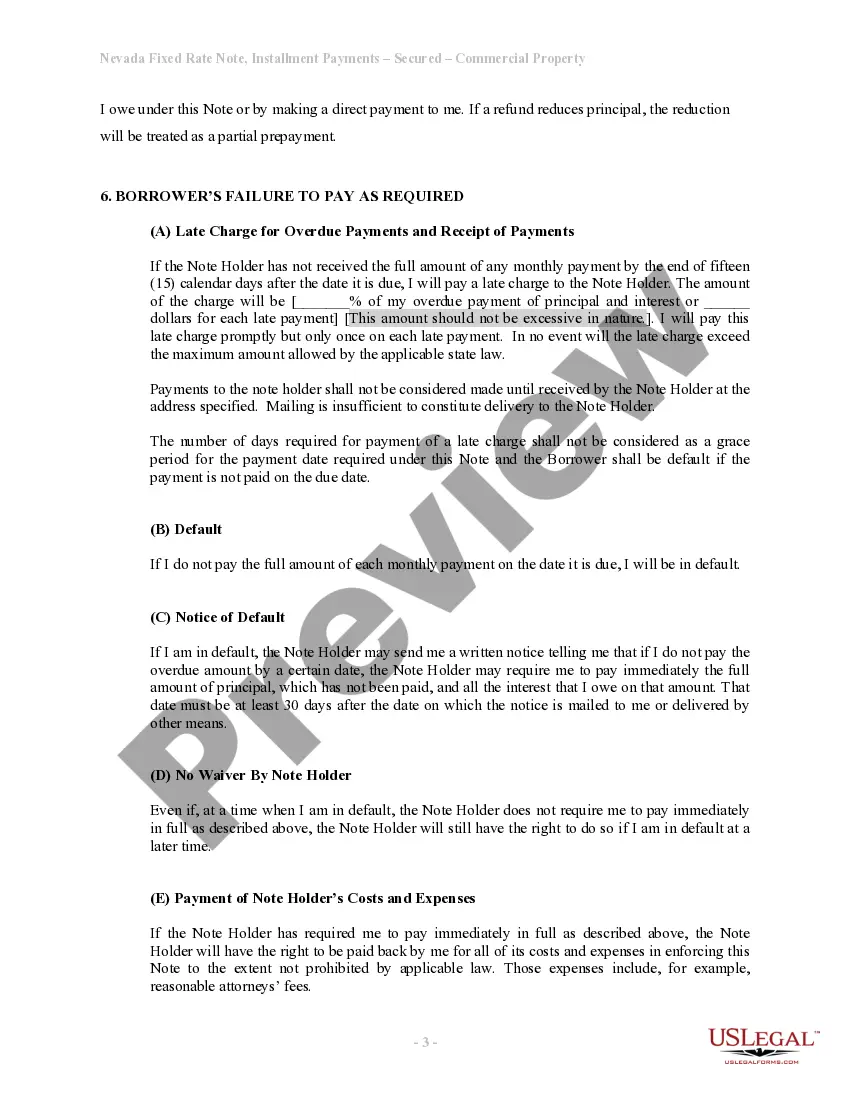

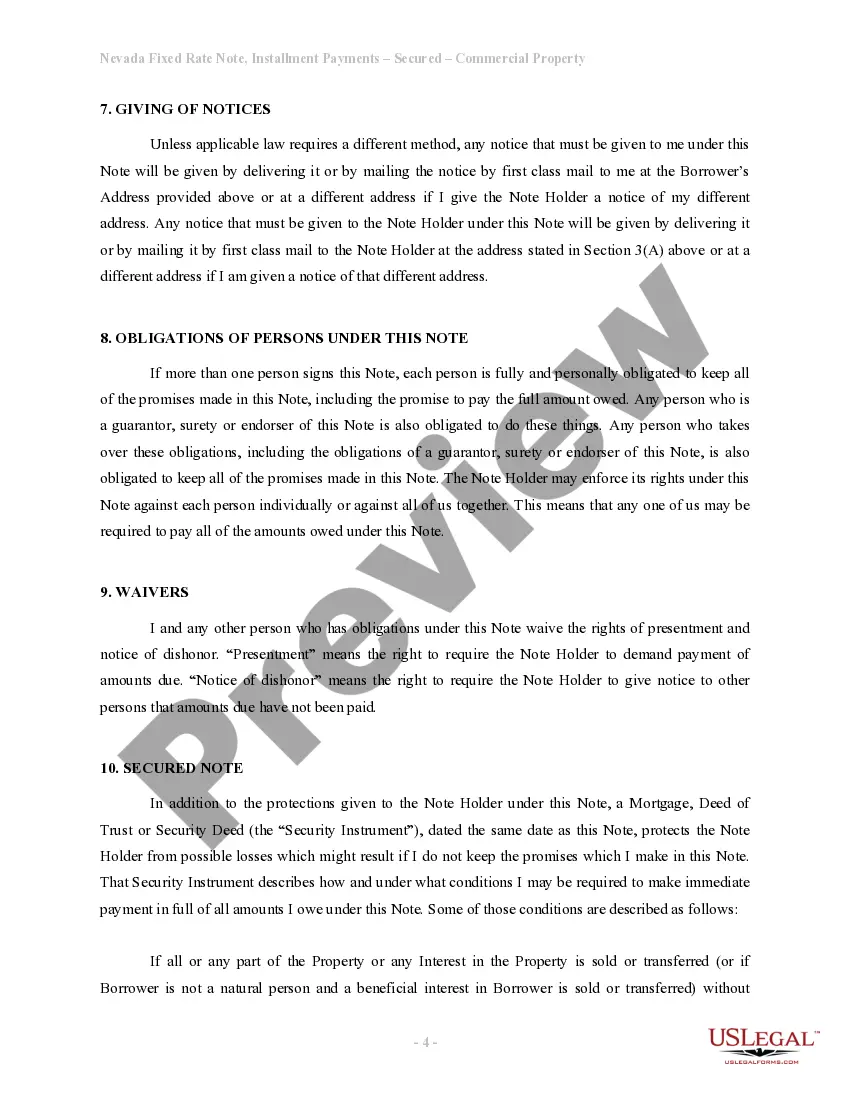

This is a form of Promissory Note for use where commercial property is security for the loan. A separate deed of trust or mortgage is also required.

Nevada Note And Mortgage

Instant download

Description

Free preview

Form popularity

FAQ

The main difference lies in the number of parties involved in the transaction. A mortgage is a two-party agreement between the borrower and the lender, while a deed of trust involves three parties: the borrower, the lender, and a trustee. This tri-party arrangement allows for more efficient handling of foreclosure processes in deed of trust transactions. If you're navigating the Nevada note and mortgage landscape, understanding this distinction is key for informed decisions.

Nevada primarily utilizes deeds of trust rather than traditional mortgages for real estate transactions. Deeds of trust provide a streamlined process for lenders, allowing them to initiate foreclosure more quickly if necessary. This framework offers certain advantages for both borrowers and lenders in Nevada's real estate market. If you seek detailed information about Nevada note and mortgage practices, consider exploring the resources available through US Legal Forms.

In California, both mortgages and deeds of trust are valid options for securing loans. Most lenders prefer deeds of trust because they offer a faster foreclosure process compared to traditional mortgages. While the terms are often used interchangeably, understanding the distinction can be crucial for your financial decisions. If you are considering a property in California, getting insights from resources like US Legal Forms can guide you through these choices effectively.

Yes, Nevada is a non-recourse mortgage state, which means that borrowers can limit their liability if they default on their loans. In this arrangement, lenders can only recover the property, rather than pursuing additional assets from the borrower. This aspect of the Nevada note and mortgage system can provide peace of mind for homeowners, as it lowers personal financial risk. When considering a mortgage in Nevada, understanding this non-recourse nature is essential for making informed decisions.

The Nevada Division of Financial Institutions is the state agency responsible for regulating the mortgage industry. This agency oversees the licensing, examination, and compliance of mortgage entities, ensuring that the Nevada note and mortgage market operates fairly and ethically. By maintaining high standards, the Division protects consumers and promotes a healthy lending environment. Engaging with this agency is important for anyone looking to work in Nevada's mortgage sector.

Obtaining a mortgage license in all 50 states requires understanding each state's regulations and requirements for the Nevada note and mortgage market. You can start by researching the specific licensing boards in each state and completing the necessary coursework and exams. Additionally, you may benefit from platforms like US Legal Forms, which provide templates and guidance to streamline your licensing process. This comprehensive approach ensures you meet the varied requirements across the nation.

In Nevada, you can obtain two main types of mortgage licenses: the Mortgage Broker License and the Mortgage Banker License. Each license caters to different roles in the Nevada note and mortgage industry. The Mortgage Broker License allows you to act as an intermediary between borrowers and lenders, while the Mortgage Banker License enables you to directly lend funds to borrowers. Understanding these licenses is essential for navigating the Nevada mortgage landscape effectively.

Not all US mortgages are non-recourse. The terms depend on the state law and the specific mortgage agreement. While Nevada offers non-recourse options, borrowers in other states may face personal liability for their mortgage. Always review your agreement carefully to understand your rights and obligations regarding the Nevada note and mortgage.

To obtain your mortgage statement, check with your lender's website or contact their customer service. Most lenders provide online access to your account, making it easy to view and download your statements. Always review these documents, as they contain important information related to your Nevada note and mortgage.

To obtain your mortgage license in Nevada, you must complete specific educational requirements, pass a background check, and submit an application to the Nevada Division of Mortgage Lending. It’s important to study the state laws governing mortgages thoroughly to comply. Once you secure your license, you can assist others with their Nevada note and mortgage transactions.