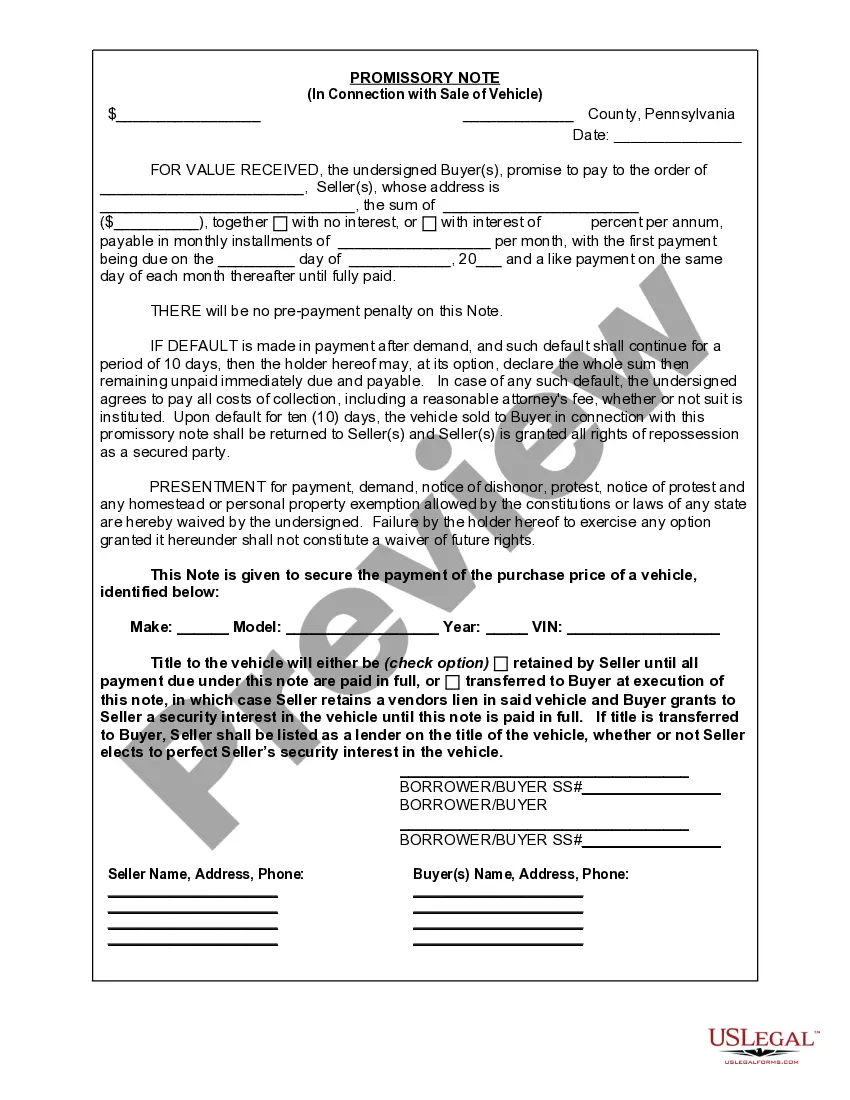

This form is a Promissory Note in connection with the sale of a vehicle where the Buyer is to pay a portion of the purchase price over time.

Pennsylvania Promissory Note With Balloon Payment

Category:

State:

Pennsylvania

Control #:

PA-00431-D

Format:

Word;

Rich Text

Instant download

Description promissory note with balloon payment template

How to fill out Pennsylvania Promissory Note With Balloon Payment?

When you are required to complete a Pennsylvania Promissory Note With Balloon Payment in line with your local state's statutes and regulations, there can be several choices to select from.

There is no need to review each document to ensure it satisfies all the legal standards if you are a subscriber to US Legal Forms.

It is a reliable service that can assist you in acquiring a reusable and contemporary template on any topic.

Using US Legal Forms simplifies the process of getting properly drafted official documents. In addition, Premium users can also enjoy robust integrated solutions for online PDF editing and signing. Give it a try today!

- US Legal Forms is the largest online repository with a collection of over 85,000 ready-to-use documents for business and personal legal situations.

- All templates are confirmed to comply with each state's laws.

- For this reason, when retrieving the Pennsylvania Promissory Note With Balloon Payment from our site, you can be assured that you have a legitimate and current document.

- Obtaining the required sample from our platform is quite simple.

- If you already possess an account, just Log In to the platform, ensure your subscription is active, and save the selected file.

- Later, you can visit the My documents tab in your profile and access the Pennsylvania Promissory Note With Balloon Payment at any time.

- If this is your first experience with our site, please follow the instructions below.

- Review the suggested page and verify it for alignment with your needs.

Form popularity

FAQ

Typically, a balloon payment would represent a percentage of the purchase price of the vehicle. For example, for a car costing R300 000, a 20 % balloon payment would work out at R60 000. This would be paid in one lump sum at the end of the contract period for example 60 months or five years after purchase.

Balloon payments are often packaged into two-step mortgages. In a "balloon payment mortgage," the borrower pays a set interest rate for a certain number of years. Then, the loan then resets and the balloon payment rolls into a new or continuing amortized mortgage at the prevailing market rates at the end of that term.

A Promissory Note with Balloon Payments is a loan contract that enables a lender set loan terms with one or more larger payments at the end. This lending document helps you to clarify the terms of a loan, define the payment schedule, and provide an amortization table, if the loan includes interest.

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

Interesting Questions

More info

A promissory note puts the terms of a loan in writing. A promissory note is a written commitment to pay someone.The seller retains title to the property until the purchase price is paid. ( ) INTEREST ONLY PAYMENTS on the outstanding principal balance. (The following must be completed if "b" or "c" is checked). The Note should specify how the lender makes demand. Pennsylvania Housing Finance Agency. Loans with balloon payments have lower monthly payments and are paid off with a lump sum. (c) Borrower shall pay the full amount of all outstanding principal and interest in one balloon payment on October 12, 2026 (the "Maturity Date"). Laude, from the University of Pennsylvania Law School.