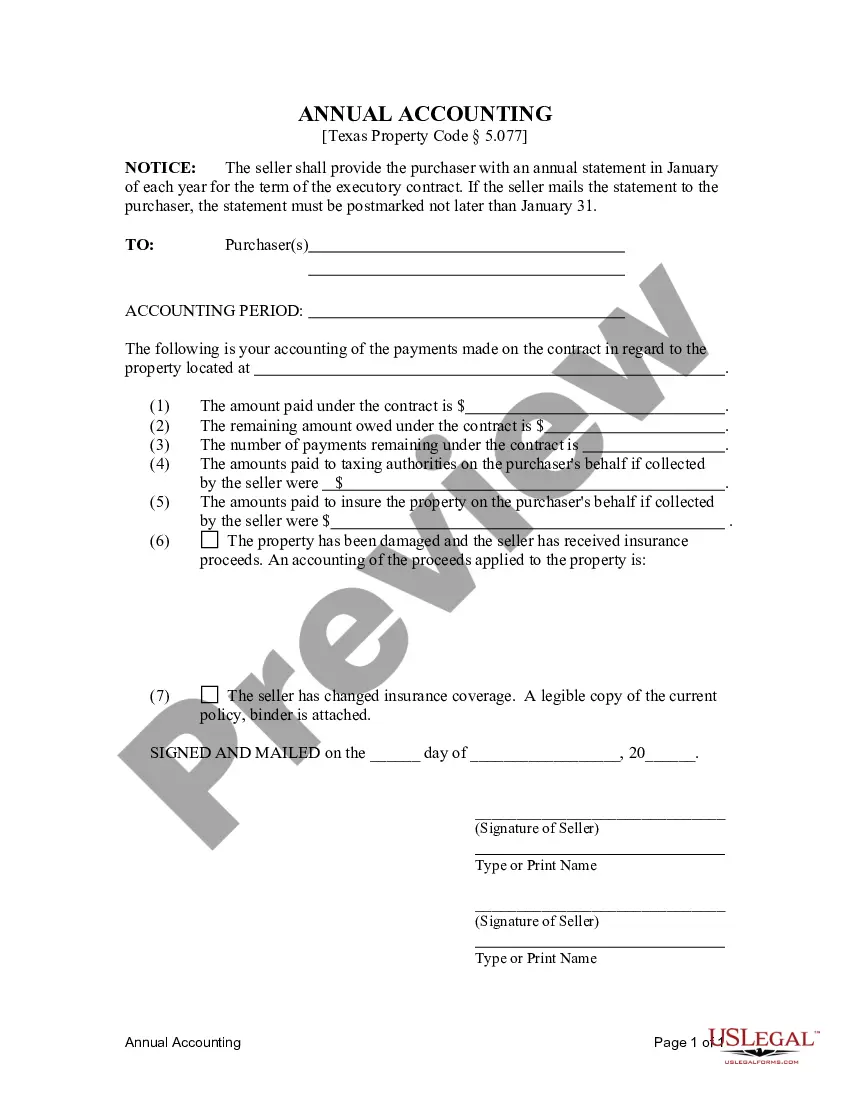

This is a Seller's Annual Accounting Statement notifying the Purchaser of the number and amount of payments received toward contract for deed's purchase price and interest. This document is provided annually by Seller to Purchaser.

Texas Buyer Seller Affidavit Form

Category:

State:

Texas

Control #:

TX-00470-4

Format:

Word;

Rich Text

Instant download

Description Executory

How to fill out Sellers Residential Land?

How to get professional legal papers compliant with your state regulations and draft the Texas Buyer Seller Affidavit Form without applying to a lawyer? A lot of services on the web offer templates to cover various legal situations and formalities. Nonetheless, it may take time to figure out which of the available samples satisfy both use case and juridical criteria for you. US Legal Forms is a trustworthy platform that helps you locate formal documents composed in accordance with the latest state law updates and save money on juridical assistance.

US Legal Forms is not a regular web catalog. It's a collection of more than 85k verified templates for various business and life situations. All papers are arranged by area and state to make your search process quicker and more convenient. In addition, it integrates with powerful tools for PDF editing and electronic signature, allowing users with a Premium subscription to quickly fill out their paperwork online.

It takes minimum effort and time to get the needed paperwork. If you already have an account, log in and make sure your subscription is valid. Download the Texas Buyer Seller Affidavit Form with the relevant button next to the file name. If you don't have an account with US Legal Forms, then adhere to the guide below:

- Go over the web page you've opened and check if the form fits your needs.

- To do so, take advantage of the form description and preview options if available.

- Look for another sample in the header providing your state if necessary.

- Click the Buy Now button once you find the appropriate document.

- Choose the most suitable pricing plan, then log in or create an account.

- Decide on the payment method (by credit card or via PayPal).

- Change the file format for your Texas Buyer Seller Affidavit Form and click Download.

The acquired documents remain in your possession: you can always return to them in the My Forms tab of your profile. Sign up for our platform and prepare legal documents on your own like an experienced legal specialist!