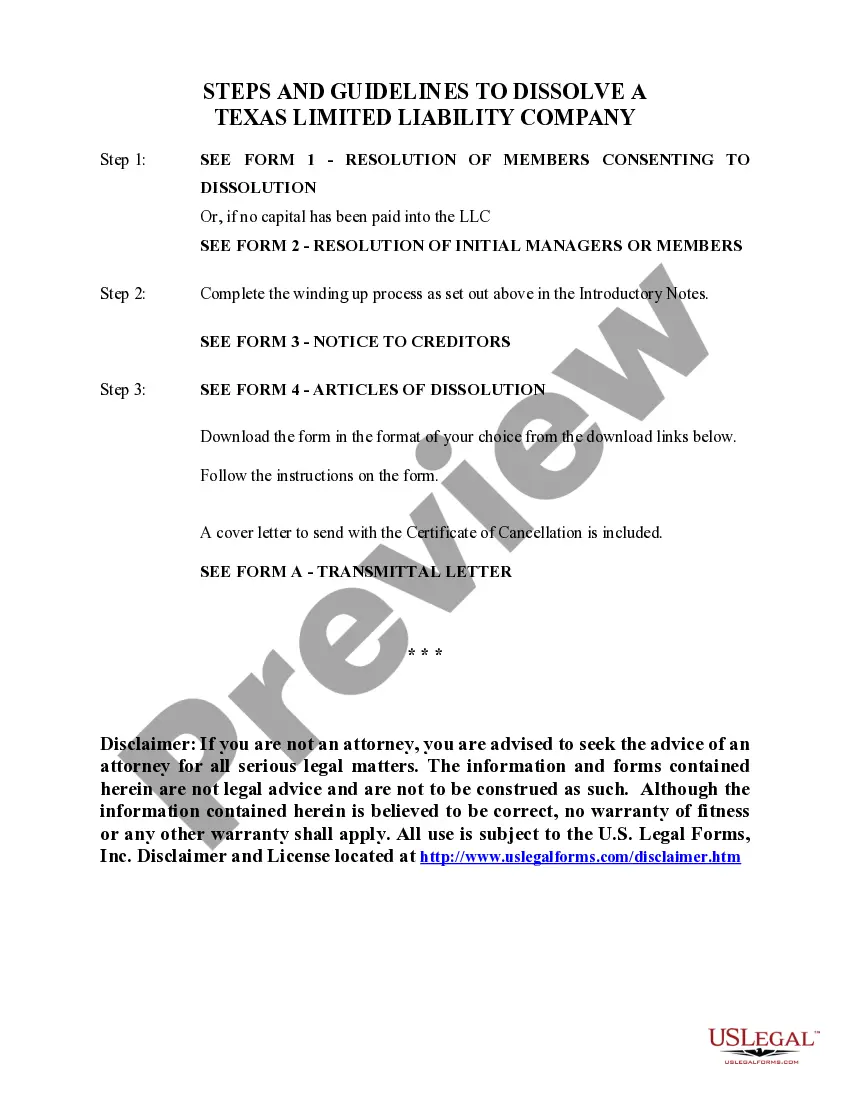

The dissolution package contains all forms to dissolve a LLC or PLLC in Texas, step by step instructions, addresses, transmittal letters, and other information.

We use cookies to improve security, personalize the user experience, enhance our marketing activities (including cooperating with our marketing partners) and for other business use.

Click "here" to read our Cookie Policy. By clicking "Accept" you agree to the use of cookies. Read less

Read more

- US Legal Forms

- Agreements - Agreement Forms

-

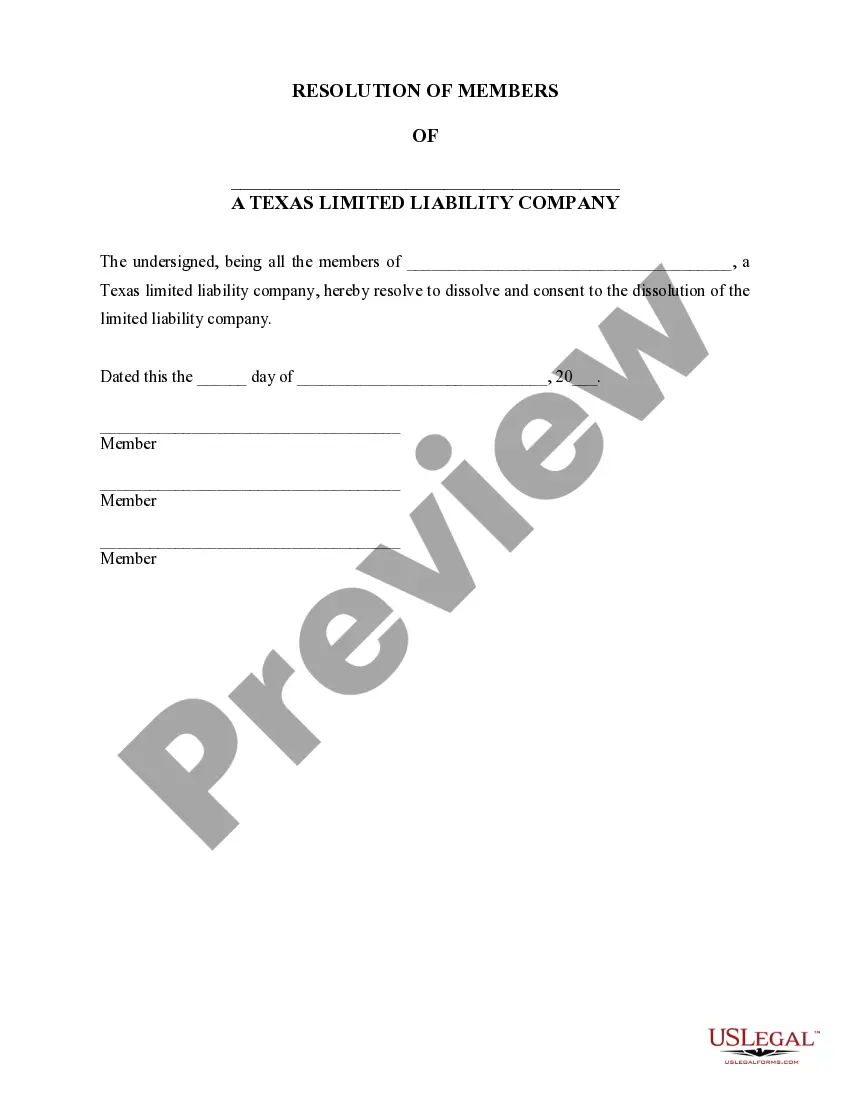

Texas Dissolution Package to Dissolve Limited Liability Company LLC

Texas Dissolve Llc Withdrawal

State:

Texas

Control #:

TX-DP-LLC-0001

Format:

Word;

Rich Text

Instant download

Description Texas Limited Liability Company

Free preview Dissolution Dissolve Llc

Dissolve Limited Liability Company Related forms

View Parents liability for tort of minors

View Parents liability for tort of minors

View this form

View Court transcript proceedings for rent arrears

View Court transcript proceedings for rent arrears

View this form

View Notice reclaim rental property for our own use form

View Notice reclaim rental property for our own use form

View this form

View Late fee for rent

View Late fee for rent

View this form

View Late fee for rent bc

View Late fee for rent bc

View this form

Related legal definitions

How To Dissolve An Llc In Texas Form Rating

4.7

Satisfied(469)

Limited Liability Company Texas Form popularity

Tx Dissolve Llc Other Form Names

Dissolution Limited Liability Company

Texas Limited Liability Company Form

Texas Dissolution Dissolve

Texas Dissolution Dissolve Limited Liability Company

Dissolution All Dissolve

Tx Limited Liability Company

Llc Its Dissolve

Texas Dissolve Llc Withdrawal Related Searches

-

how to dissolve an llc in texas online

-

how to reinstate a forfeited llc in texas

-

how to close a dba in texas

-

how much does it cost to dissolve an llc in texas

-

dissolve llc texas form

-

certificate of termination texas

-

tax forfeiture llc texas

-

certificate of termination texas online

-

how to reinstate a forfeited llc in texas

-

how to close a dba in texas

Texas Dissolution Llc Interesting Questions

The process to dissolve an LLC in Texas involves filing a Certificate of Termination with the Secretary of State, settling all outstanding debts and taxes, and obtaining written consent from the members or managers of the LLC.

Yes, you can voluntarily dissolve your LLC in Texas. It is a decision made by the owners/members of the LLC to dissolve the business.

Yes, you need to file a Certificate of Termination with the Texas Secretary of State to formalize the dissolution of your LLC.

To dissolve an LLC in Texas, you must ensure that all taxes and debts of the LLC are paid off, and the members or managers of the LLC should agree to the dissolution.

The cost of dissolving an LLC in Texas varies. The filing fee for a Certificate of Termination with the Texas Secretary of State is $40, but additional costs may be incurred depending on the complexity of your LLC and any outstanding obligations.

After LLC dissolution in Texas, you will still be responsible for handling any remaining debts and obligations of the LLC until they are fully settled. It's important to properly wind up the business affairs to avoid any potential personal liability.

No, you cannot dissolve your LLC without notifying creditors. It is important to inform all creditors and settle any outstanding debts before officially dissolving the LLC.

The time required to dissolve an LLC in Texas can vary. Once you file the Certificate of Termination, it usually takes around 7-10 business days for processing. However, the complete dissolution process may take longer depending on the specific circumstances of your LLC.

No, there is no specific timeframe for dissolving an LLC in Texas. It is up to the owners/members to decide when they want to dissolve the LLC, as long as all necessary requirements are fulfilled.

If you don't properly dissolve your LLC in Texas, you may still be liable for any ongoing obligations, taxes, or debts of the LLC, which can potentially lead to legal issues and personal liability.

Texas Dissolve Llc Trusted and secure by over 3 million people of the world’s leading companies

Limited Liability Company Form

Change state

To change the state, select it from the list below and press Change state.

Changing the state redirects you to another page.

Texas

Change state

-

No results found.

-

Texas

-

Alabama

-

Alaska

-

Arizona

-

Arkansas

-

California

-

Connecticut

-

Delaware

-

District of Columbia

-

Florida

-

Georgia

-

Hawaii

-

Idaho

-

Illinois

-

Indiana

-

Iowa

-

Kansas

-

Kentucky

-

Louisiana

-

Maine

-

Maryland

-

Massachusetts

-

Michigan

-

Minnesota

-

Missouri

-

Montana

-

Nebraska

-

Nevada

-

New Hampshire

-

New Jersey

-

New Mexico

-

New York

-

North Carolina

-

North Dakota

-

Ohio

-

Oklahoma

-

Oregon

-

Pennsylvania

-

South Carolina

-

Tennessee

-

Utah

-

Vermont

-

Virginia

-

Washington

-

West Virginia

-

Wyoming

Law summary

Texas Dissolution Package to Dissolve Limited Liability Company LLC

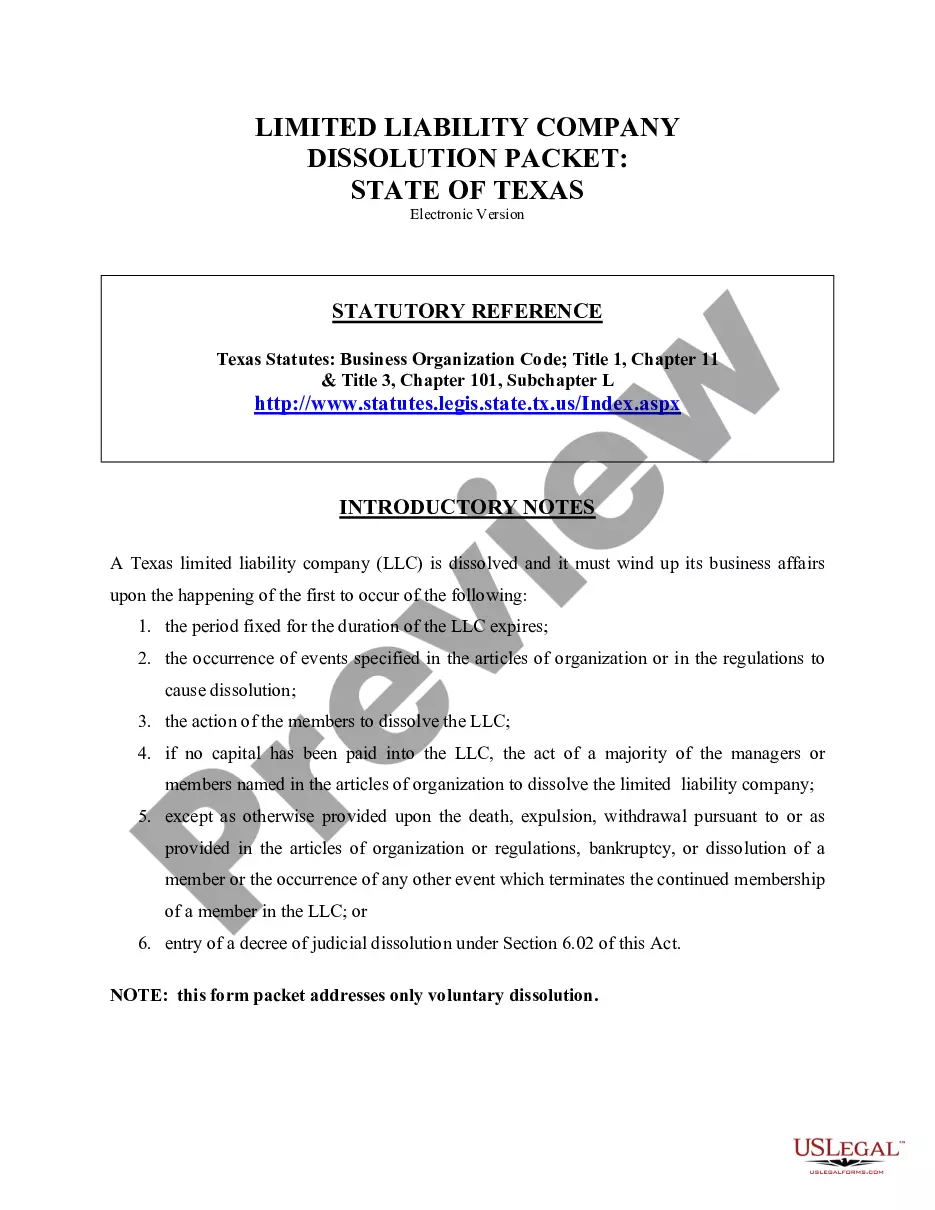

LIMITED LIABILITY COMPANY DISSOLUTION

STATUTORY REFERENCE:

Texas Statutes: Business Organization Code; Title 1, Chapter 11 & Title 3, Chapter 101, Subchapter L

DISCUSSION

A Texas limited liability company (LLC) is dissolved and it must wind up its business affairs upon the happening of the first to occur of the following:

- the period fixed for the duration of the LLC expires;

- the occurrence of events specified in the articles of organization or in the regulations to cause dissolution;

- the action of the members to dissolve the LLC;

- if no capital has been paid into the LLC, the act of a majority of the managers or members named in the articles of organization to dissolve the limited liability company;

- except as otherwise provided upon the death, expulsion, withdrawal pursuant to or as provided in the articles of organization or regulations, bankruptcy, or dissolution of a member or the occurrence of any other event which terminates the continued membership of a member in the LLC; or

- entry of a decree of judicial dissolution under Section 6.02 of this Act.

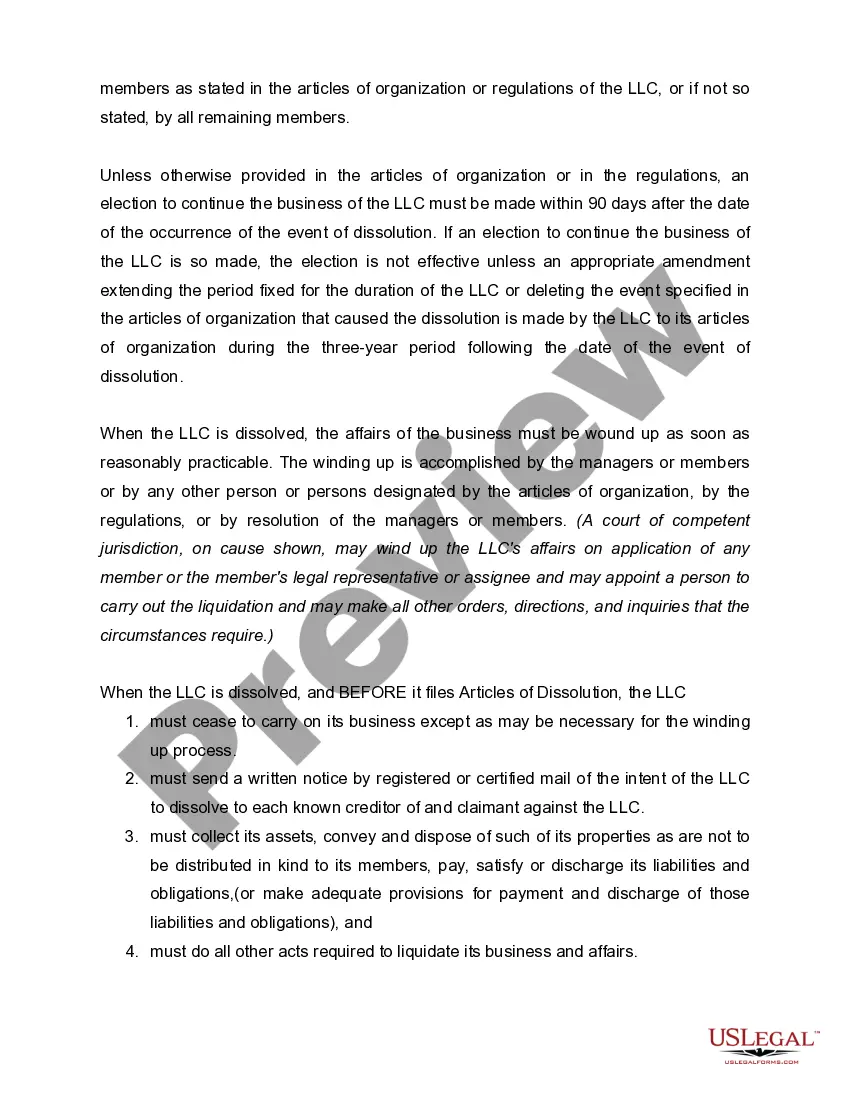

Unless otherwise provided in the articles of organization or in the regulations, an election to continue the business of the LLC must be made within 90 days after the date of the occurrence of the event of dissolution. If an election to continue the business of the LLC is so made, the election is not effective unless an appropriate amendment extending the period fixed for the duration of the LLC or deleting the event specified in the articles of organization that caused the dissolution is made by the LLC to its articles of organization during the three-year period following the date of the event of dissolution.

When the LLC is dissolved, the affairs of the business must be wound up as soon as reasonably practicable. The winding up is accomplished by the managers or members or by any other person or persons designated by the articles of organization, by the regulations, or by resolution of the managers or members. (A court of competent jurisdiction, on cause shown, may wind up the LLC's affairs on application of any member or the member's legal representative or assignee and may appoint a person to carry out the liquidation and may make all other orders, directions, and inquiries that the circumstances require.)

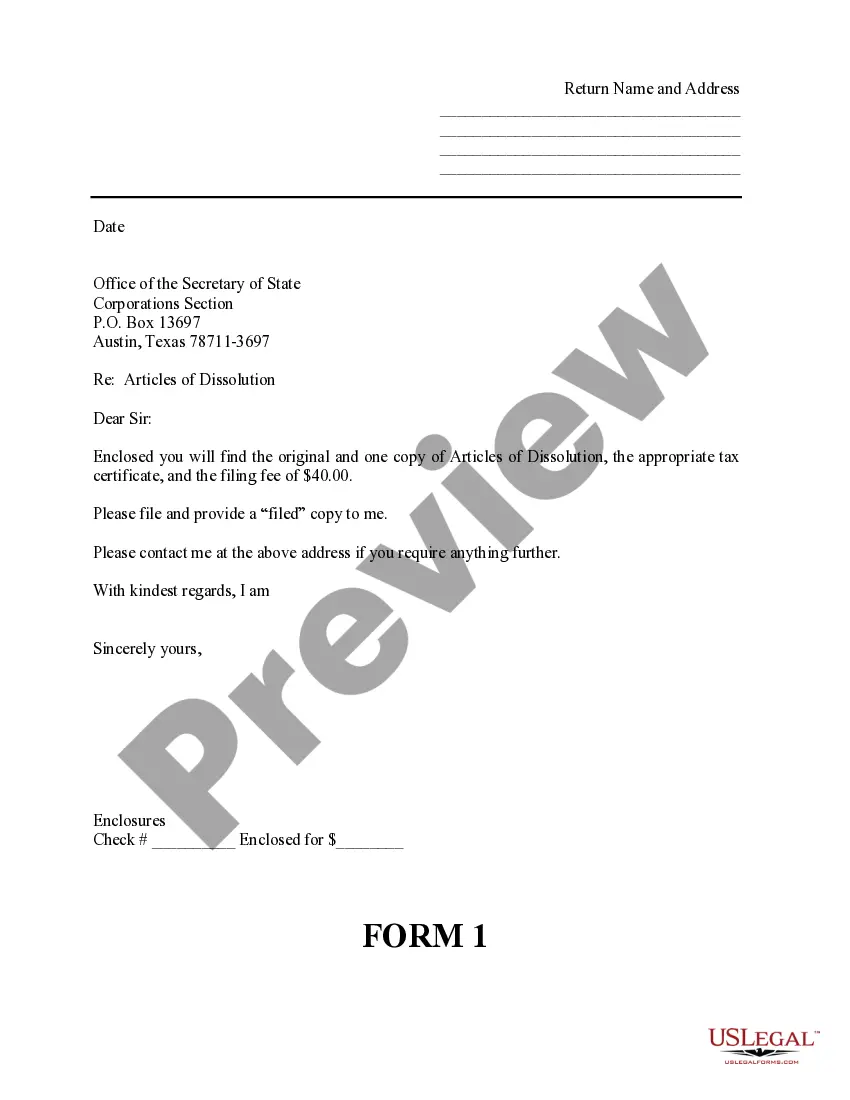

When the LLC is dissolved, and BEFORE it files Articles of Dissolution, the LLC

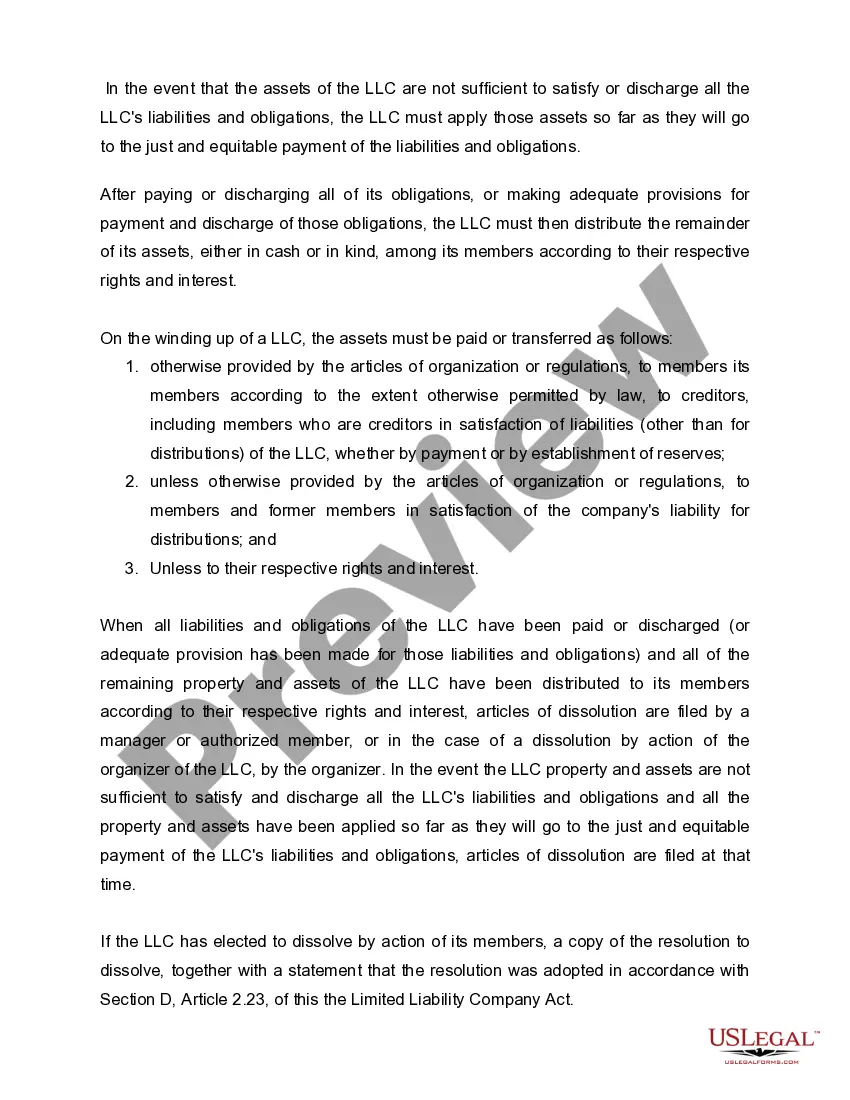

After paying or discharging all of its obligations, or making adequate provisions for payment and discharge of those obligations, the LLC must then distribute the remainder of its assets, either in cash or in kind, among its members according to their respective rights and interest.

On the winding up of a LLC, the assets must be paid or transferred as follows:

If the LLC has elected to dissolve by action of its members, a copy of the resolution to dissolve, together with a statement that the resolution was adopted in accordance with Section D, Article 2.23, of this the Limited Liability Company Act.

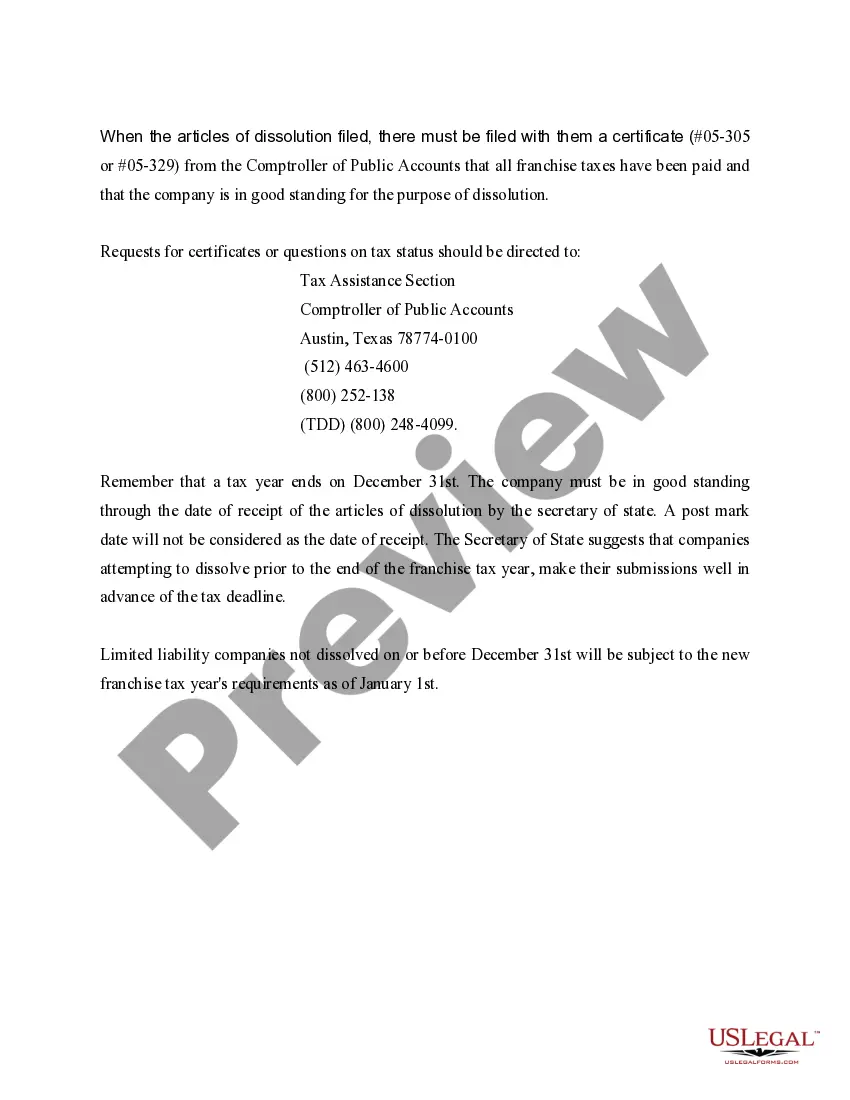

When the articles of dissolution filed, there must be filed with them a certificate (#05-305 or #05-329) from the Comptroller of Public Accounts that all franchise taxes have been paid and that the company is in good standing for the purpose of dissolution.

A tax year ends on December 31st. The company must be in good standing through the date of receipt of the articles of dissolution by the secretary of state. A post mark date will not be considered as the date of receipt. The Secretary of State suggests that companies attempting to dissolve prior to the end of the franchise tax year, make their submissions well in advance of the tax deadline.

Limited liability companies not dissolved on or before December 31st will be subject to the new franchise tax year's requirements as of January 1st.

Note: All Information and Previews are subject to the Disclaimer

located on the main forms page, and also linked at the bottom of all search

results.

Legal definition

Texas Dissolution Package to Dissolve Limited Liability Company LLC

LIMITED LIABILITY COMPANY DISSOLUTION

STATUTORY REFERENCE:

Texas Statutes: Business Organization Code; Title 1, Chapter 11 & Title 3, Chapter 101, Subchapter L

DISCUSSION

A Texas limited liability company (LLC) is dissolved and it must wind up its business affairs upon the happening of the first to occur of the following:

- the period fixed for the duration of the LLC expires;

- the occurrence of events specified in the articles of organization or in the regulations to cause dissolution;

- the action of the members to dissolve the LLC;

- if no capital has been paid into the LLC, the act of a majority of the managers or members named in the articles of organization to dissolve the limited liability company;

- except as otherwise provided upon the death, expulsion, withdrawal pursuant to or as provided in the articles of organization or regulations, bankruptcy, or dissolution of a member or the occurrence of any other event which terminates the continued membership of a member in the LLC; or

- entry of a decree of judicial dissolution under Section 6.02 of this Act.

Unless otherwise provided in the articles of organization or in the regulations, an election to continue the business of the LLC must be made within 90 days after the date of the occurrence of the event of dissolution. If an election to continue the business of the LLC is so made, the election is not effective unless an appropriate amendment extending the period fixed for the duration of the LLC or deleting the event specified in the articles of organization that caused the dissolution is made by the LLC to its articles of organization during the three-year period following the date of the event of dissolution.

When the LLC is dissolved, the affairs of the business must be wound up as soon as reasonably practicable. The winding up is accomplished by the managers or members or by any other person or persons designated by the articles of organization, by the regulations, or by resolution of the managers or members. (A court of competent jurisdiction, on cause shown, may wind up the LLC's affairs on application of any member or the member's legal representative or assignee and may appoint a person to carry out the liquidation and may make all other orders, directions, and inquiries that the circumstances require.)

When the LLC is dissolved, and BEFORE it files Articles of Dissolution, the LLC

After paying or discharging all of its obligations, or making adequate provisions for payment and discharge of those obligations, the LLC must then distribute the remainder of its assets, either in cash or in kind, among its members according to their respective rights and interest.

On the winding up of a LLC, the assets must be paid or transferred as follows:

If the LLC has elected to dissolve by action of its members, a copy of the resolution to dissolve, together with a statement that the resolution was adopted in accordance with Section D, Article 2.23, of this the Limited Liability Company Act.

When the articles of dissolution filed, there must be filed with them a certificate (#05-305 or #05-329) from the Comptroller of Public Accounts that all franchise taxes have been paid and that the company is in good standing for the purpose of dissolution.

A tax year ends on December 31st. The company must be in good standing through the date of receipt of the articles of dissolution by the secretary of state. A post mark date will not be considered as the date of receipt. The Secretary of State suggests that companies attempting to dissolve prior to the end of the franchise tax year, make their submissions well in advance of the tax deadline.

Limited liability companies not dissolved on or before December 31st will be subject to the new franchise tax year's requirements as of January 1st.

Note: All Information and Previews are subject to the Disclaimer

located on the main forms page, and also linked at the bottom of all search

results.

Sorry, this device is not supported

Please open this page on your desktop computer.