Texas Dissolution Package to Dissolve Limited Liability Company LLC

TEXAS

LIMITED LIABILITY COMPANY DISSOLUTION

STATUTORY REFERENCE:

Â

Texas Statutes: Business Organization Code; Title 1, Chapter 11

& Title 3, Chapter 101, Subchapter L

DISCUSSION

A Texas limited liability company (LLC) is dissolved and it must wind

up its business affairs upon the happening of the first to occur of the

following:

-

the period fixed for the duration of the LLC expires;

-

the occurrence of events specified in the articles of organization or in

the regulations to cause dissolution;

-

the action of the members to dissolve the LLC;

-

if no capital has been paid into the LLC, the act of a majority of the

managers or members named in the articles of organization to dissolve the

limited liability company;

-

except as otherwise provided upon the death, expulsion, withdrawal pursuant

to or as provided in the articles of organization or regulations, bankruptcy,

or dissolution of a member or the occurrence of any other event which terminates

the continued membership of a member in the LLC; or

-

entry of a decree of judicial dissolution under Section 6.02 of this Act.

A LLC is not upon the happening of an event of dissolution if there is

at least one remaining member, and the business of the LLC is continued

by the vote of that/those members as stated in the articles of organization

or regulations of the LLC, or if not so stated, by all remaining members.

Unless otherwise provided in the articles of organization or in the

regulations, an election to continue the business of the LLC must be made

within 90 days after the date of the occurrence of the event of dissolution.

If an election to continue the business of the LLC is so made, the election

is not effective unless an appropriate amendment extending the period

fixed for the duration of the LLC or deleting the event specified in the

articles of organization that caused the dissolution is made by the LLC

to its articles of organization during the three-year period following

the date of the event of dissolution.

When the LLC is dissolved, the affairs of the business must be wound

up as soon as reasonably practicable. The winding up is accomplished by

the managers or members or by any other person or persons designated by

the articles of organization, by the regulations, or by resolution of the

managers or members. (A court of competent jurisdiction, on cause shown,

may wind up the LLC's affairs on application of any member or the member's

legal representative or assignee and may appoint a person to carry out

the liquidation and may make all other orders, directions, and inquiries

that the circumstances require.)

When the LLC is dissolved, and BEFORE it files Articles of Dissolution,

the LLC

must cease to carry on its business except as may be necessary for the

winding up process.

must send a written notice by registered or certified mail of the intent

of the LLC to dissolve to each known creditor of and claimant against the

LLC.

must collect its assets, convey and dispose of such of its properties as

are not to be distributed in kind to its members, pay, satisfy or discharge

its liabilities and obligations, (or make adequate provisions for payment

and discharge of those liabilities and obligations), and

must do all other acts required to liquidate its business and affairs.

In the event that the assets of the LLC are not sufficient to satisfy

or discharge all the LLC's liabilities and obligations, the LLC must apply

those assets so far as they will go to the just and equitable payment of

the liabilities and obligations.

After paying or discharging all of its obligations, or making adequate

provisions for payment and discharge of those obligations, the LLC must

then distribute the remainder of its assets, either in cash or in kind,

among its members according to their respective rights and interest.

On the winding up of a LLC, the assets must be paid or transferred

as follows:

to the extent otherwise permitted by law, to creditors, including members

who are creditors in satisfaction of liabilities (other than for distributions)

of the LLC, whether by payment or by establishment of reserves;

unless otherwise provided by the articles of organization or regulations,

to members and former members in satisfaction of the company's liability

for distributions; and

unless otherwise provided by the articles of organization or regulations,

to members its members according to their respective rights and interest.

When all liabilities and obligations of the LLC have been paid or discharged

(or adequate provision has been made for those liabilities and obligations)

and all of the remaining property and assets of the LLC have been distributed

to its members according to their respective rights and interest, articles

of dissolution are filed by a manager or authorized member, or in the case

of a dissolution by action of the organizer of the LLC, by the organizer.

In the event the LLC property and assets are not sufficient to satisfy

and discharge all the LLC's liabilities and obligations and all the property

and assets have been applied so far as they will go to the just and equitable

payment of the LLC's liabilities and obligations, articles of dissolution

are filed at that time.

If the LLC has elected to dissolve by action of its members, a copy

of the resolution to dissolve, together with a statement that the resolution

was adopted in accordance with Section D, Article 2.23, of this the Limited

Liability Company Act.

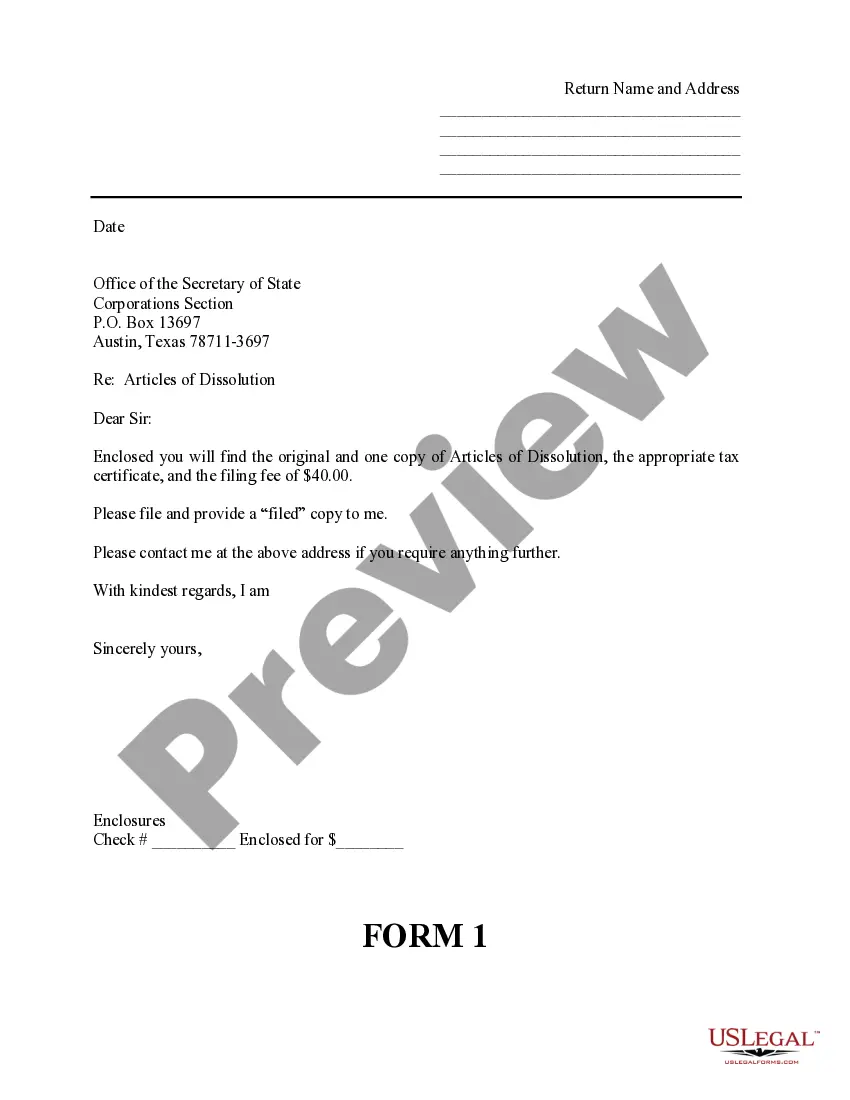

When the articles of dissolution filed, there must be filed with them

a certificate (#05-305 or #05-329) from the Comptroller of Public Accounts

that all franchise taxes have been paid and that the company is in good

standing for the purpose of dissolution.

A tax year ends on December 31st. The company must be in good standing

through the date of receipt of the articles of dissolution by the secretary

of state. A post mark date will not be considered as the date of receipt.

The Secretary of State suggests that companies attempting to dissolve

prior to the end of the franchise tax year, make their submissions well

in advance of the tax deadline.

Limited liability companies not dissolved on or before December 31st

will be subject to the new franchise tax year's requirements as of January

1st.

Note: All Information and Previews are subject to the Disclaimer

located on the main forms page, and also linked at the bottom of all search

results.