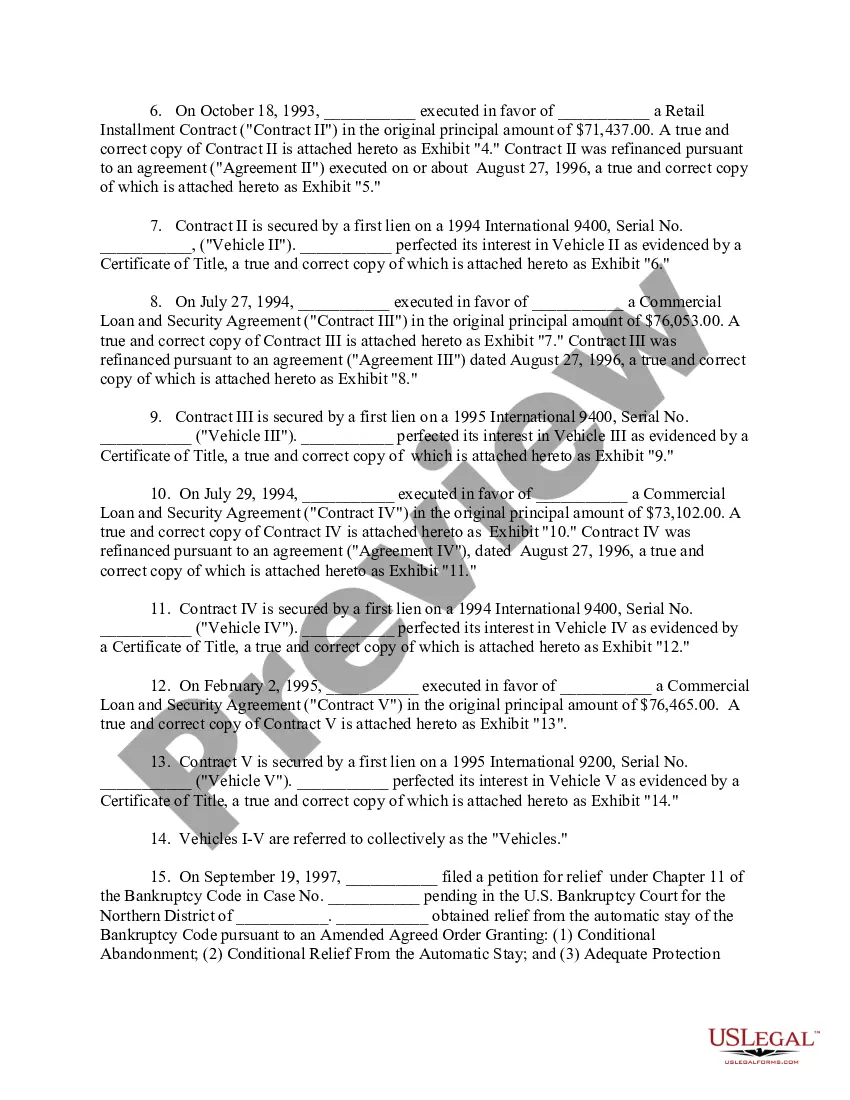

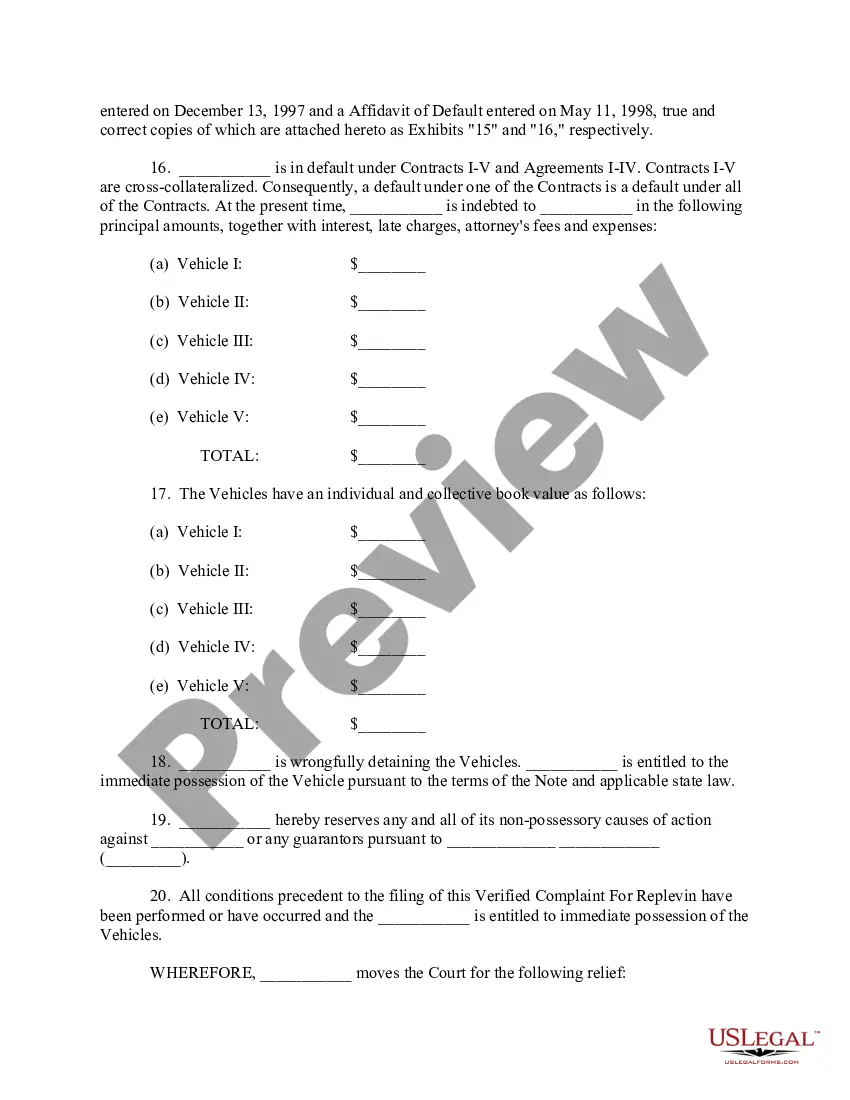

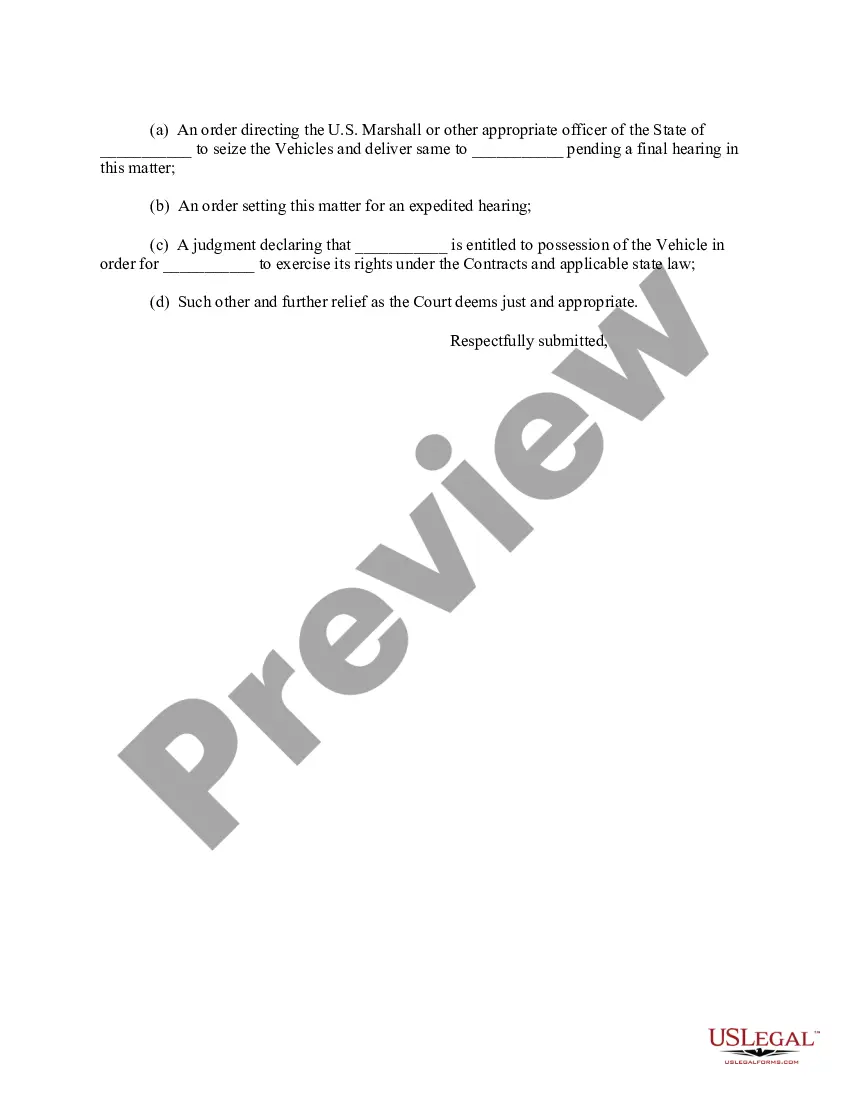

This form is a Verfied Complaint for Replevin. The plaintiff has filed this action against defendant in order to replevy certain property in the defendant's possession.

Repossession Form Document Without Comments In Nassau

Category:

State:

Multi-State

County:

Nassau

Control #:

US-000265

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

You are hereby notified that your description of motor vehicle, year, make, model and VIN #, was lawfully repossessed on Date because you defaulted on your loan with Credit Union Name. The vehicle is being held at location address of vehicle. be sold at public sale. A sale could include a lease or license.

After repossession, a consumer may have the option to redeem the vehicle before it is sold by paying the entire outstanding balance of the car loan, including interest, costs, and fees.

How many payments you can miss before you can expect car repossession depends entirely on your lender and their leniency. Most lenders won't begin repossession until you've missed three or more payments.

Ask For A Car Loan Modification – If you can see that you're having trouble paying your car loan avoid a future repossession by asking for a modification of your car loan before you fall behind on payments.

New York gives you the right to redeem or get back your repossessed vehicle by reinstating the contract. You reinstate your contract by paying any late/missing payments plus repo expenses such as towing, storage, and legal fees. But you must act quickly to do this.

Obtaining a repossession title involves completing specific paperwork to transfer ownership from the previous owner to the lienholder. This paperwork often includes an application for a repossession title, a bill of sale, and a certificate of repossession.

Dear Borrower Name: You are hereby notified that your description of motor vehicle, year, make, model and VIN #, was lawfully repossessed on Date because you defaulted on your loan with Credit Union Name. The vehicle is being held at location address of vehicle. be sold at public sale.

Know the Repo Laws of Your State. The first thing to know about how to repo a car is you need to be aware of how repo laws stand within the jurisdictions where you will conduct business. Make Sure the Debtor Is in Default. Locate and Verify the Car. Choose the Method to Repossess. Do Not Breach the Peace.

If a lender repossesses your collateral, your credit scores are likely to drop. Repossessions are typically reported to the three nationwide consumer reporting agencies (Equifax®, Transunion® and Experian®). Once they're recorded on your credit reports, they can impact your credit scores for up to seven years.

More info

Complete this form and bring it with the license plates, if any, to any Motor Vehicles office. This article covers how vehicle repossession works in New York state and what your rights are as a New Yorker.Address. Commissioner of Motor Vehicles (enter Name of Motor Vehicles office notified). Order Confirming Referee Report and Judgement of Foreclosure and Sale - Nassau County Template (Word Doc) Landlord and Tenant matters are brought in District Court, where you can sue for housing problems and evictions. 1. Gather information of the recent owner from records. We provide helpful tips and resources to help you file Chapter 7 bankruptcy in your state without a lawyer. Without effective communication,law enforcement cannot serve and protect the public. As the number of limited-English proficient individuals in this country. This document contains no pages.