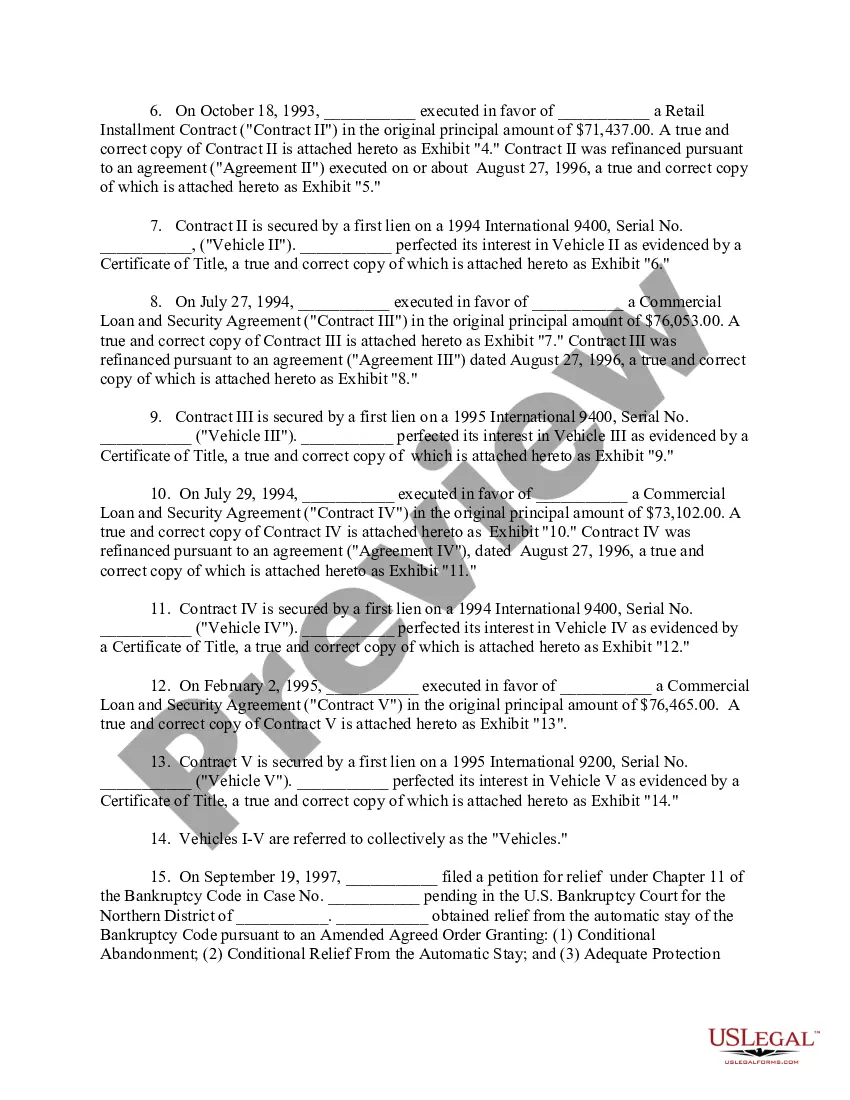

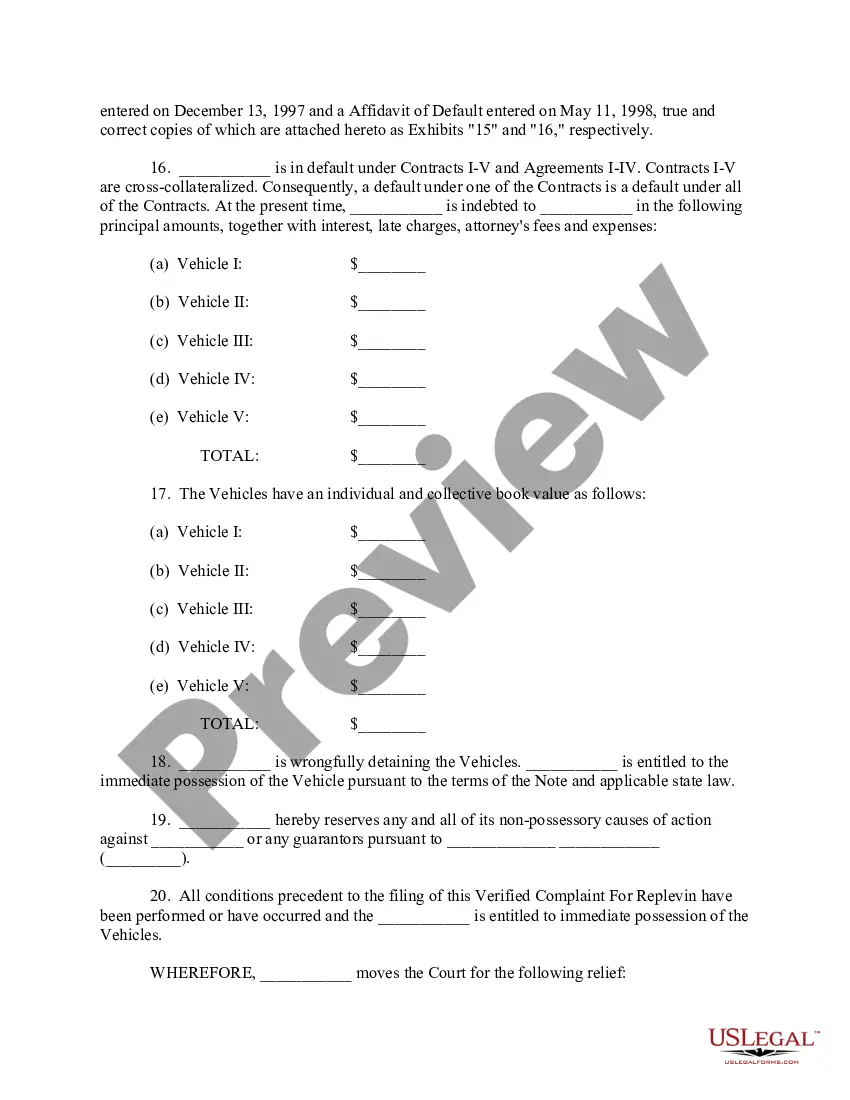

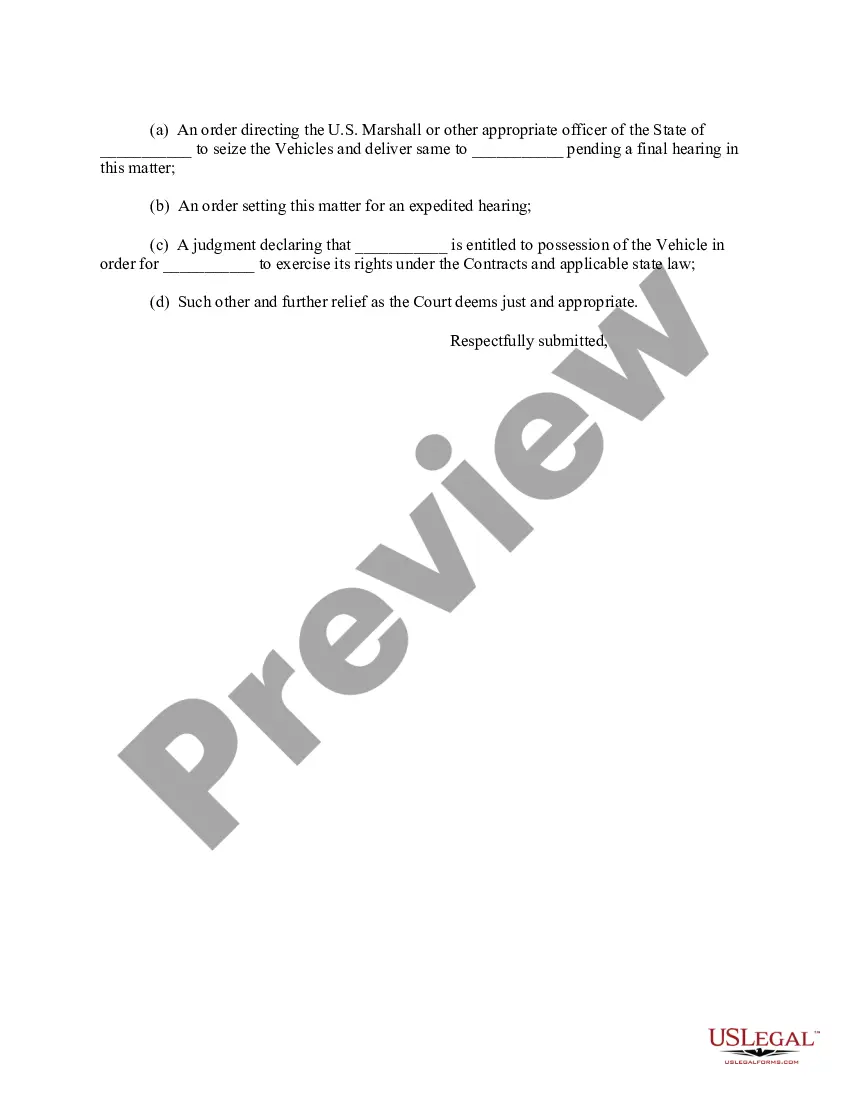

This form is a Verfied Complaint for Replevin. The plaintiff has filed this action against defendant in order to replevy certain property in the defendant's possession.

Foreclosure Letter For Home Loan In Nevada

Instant download

Description

Free preview

Form popularity

FAQ

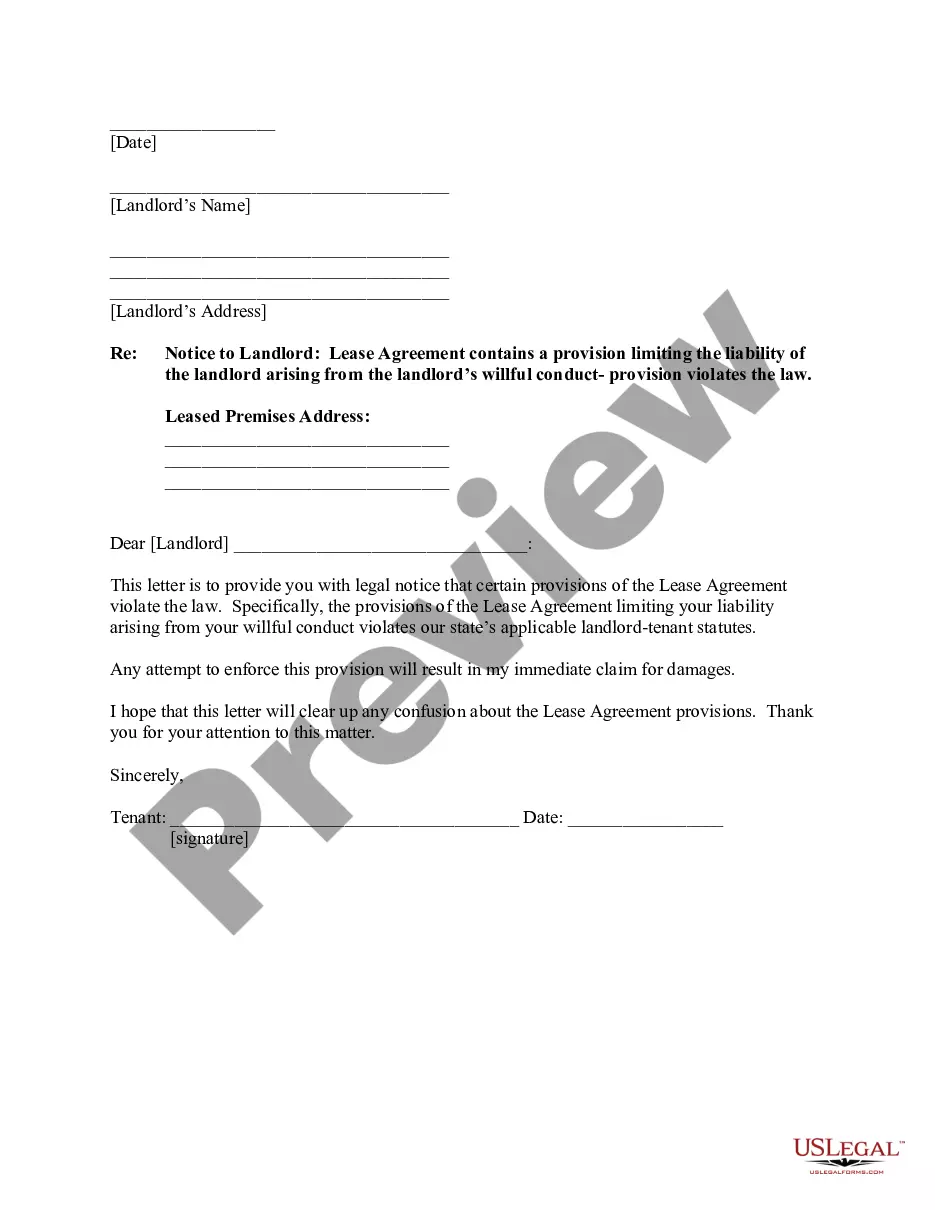

While the content of the letter will change depending on your situation, there are a few important aspects to include: Provide all details the best you can, including correct dates and dollar amounts. Explain how and when all situations were resolved. Detail why problems won't happen again.

Public records Throughout the foreclosure process, various legal notices must be filed in your County Recorder's Office. This information is public record and available to anyone. Just visit your county's office and you can search for a Notice of Default (NOD), lis pendens or Notice of Sale.

Like homeowners in other states, a Nevada homeowner usually gets plenty of time to find a way to work out a way to keep the home before the bank can sell it at a foreclosure sale. Under federal law, in most cases, the bank must wait at least 120 days before starting a foreclosure.

Again, the Nevada Homeowner's Bill of Rights requires that at least 30 calendar days before officially starting a foreclosure and at least 30 calendar days after the default, the servicer or loan owner must send you (the borrower) a notice that contains information about the account.

What to include in a hardship letter The date, your name, address and phone number. The lender/servicer and loan number. The date or approximate time frame when the hardship started. The expected timeframe of hardship — short term (six months or less) or long term. Describe your goal. State the facts, not emotions.

Sample 1: Personal Loan Closure Letter Dear Sir/Madam, I am writing to inform you that I have successfully repaid the personal loan with loan account number PL123456789. I request you to kindly process the closure of this loan account. Please find attached the necessary documents confirming the final repayment.

Does Nevada Law Allow for a Redemption Period After a Foreclosure? Nevada law allows for both judicial and non judicial foreclosures. If a lender pursues a foreclosure through the judicial system then the owner has a 1 year right of redemption following the foreclosure sale.

A servicer that receives a complete loss mitigation application more than 37 days before a foreclosure sale must take two steps within 30 days: • First, the servicer must evaluate the borrower for all loss mitigation options available to the borrower from the owner or investor of the borrower's mortgage loan.

More info

Your lender must record a Notice of Sale at least 21 days before the sale date and send the Notice of Sale to you. Nevada law requires three foreclosure notices (in addition to the preforeclosure notice): a notice of default, a danger notice, and a notice of sale.In this guide, I'll explain the process and timing for private mortgage lenders to complete a foreclosure in the state of Nevada. Learn about the Nevada foreclosure process and find out approximately how much time you'll have to explore alternatives. This process is called mortgage foreclosure. This booklet explains many of the terms, timelines and procedures involved in the foreclosure process in Arizona, California and Nevada. Of verifiable experience working in the real estate, mortgage, foreclosure or loan modification industries or applicable financial or legal fields. This is a final warning before the mortgage company begins to foreclose on a borrower's property. Among the most prominent features of the current housing crisis has been an unprecedented jump in the incidence of mortgage delinquencies and foreclosures. This clause enables the lender to sell the property without court intervention in the event of borrower default.