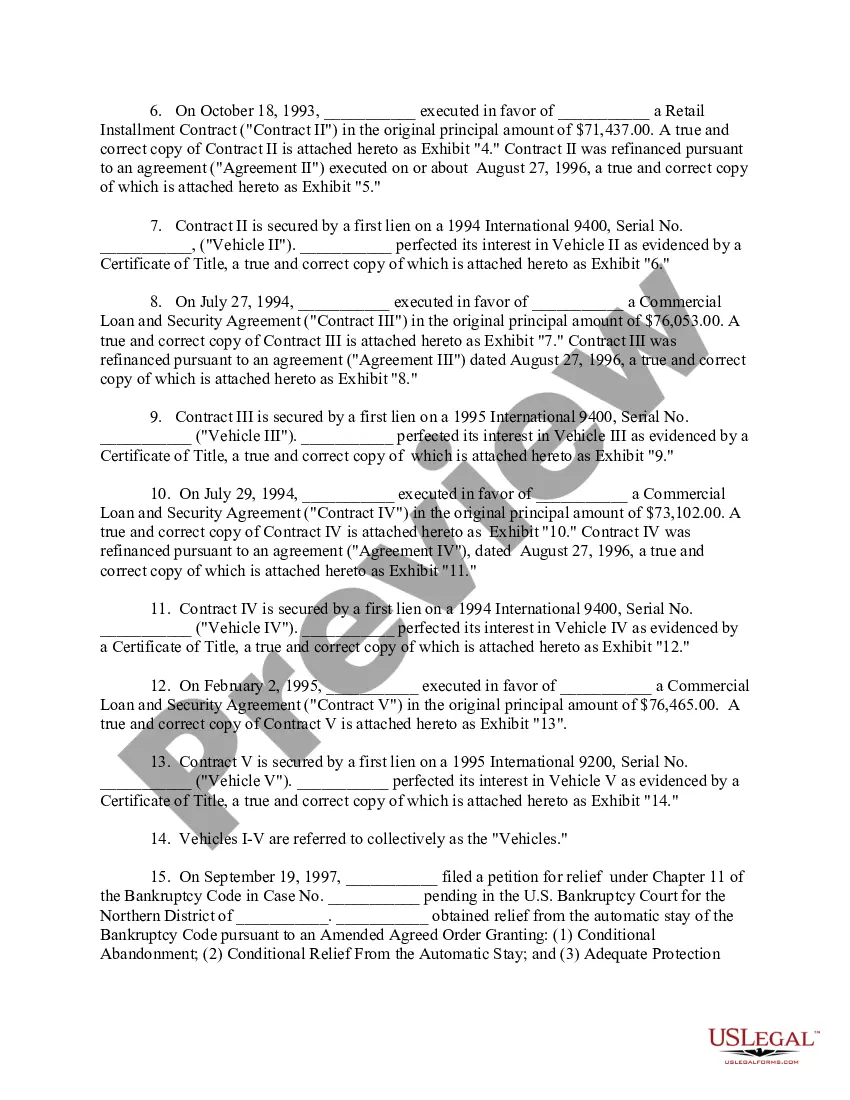

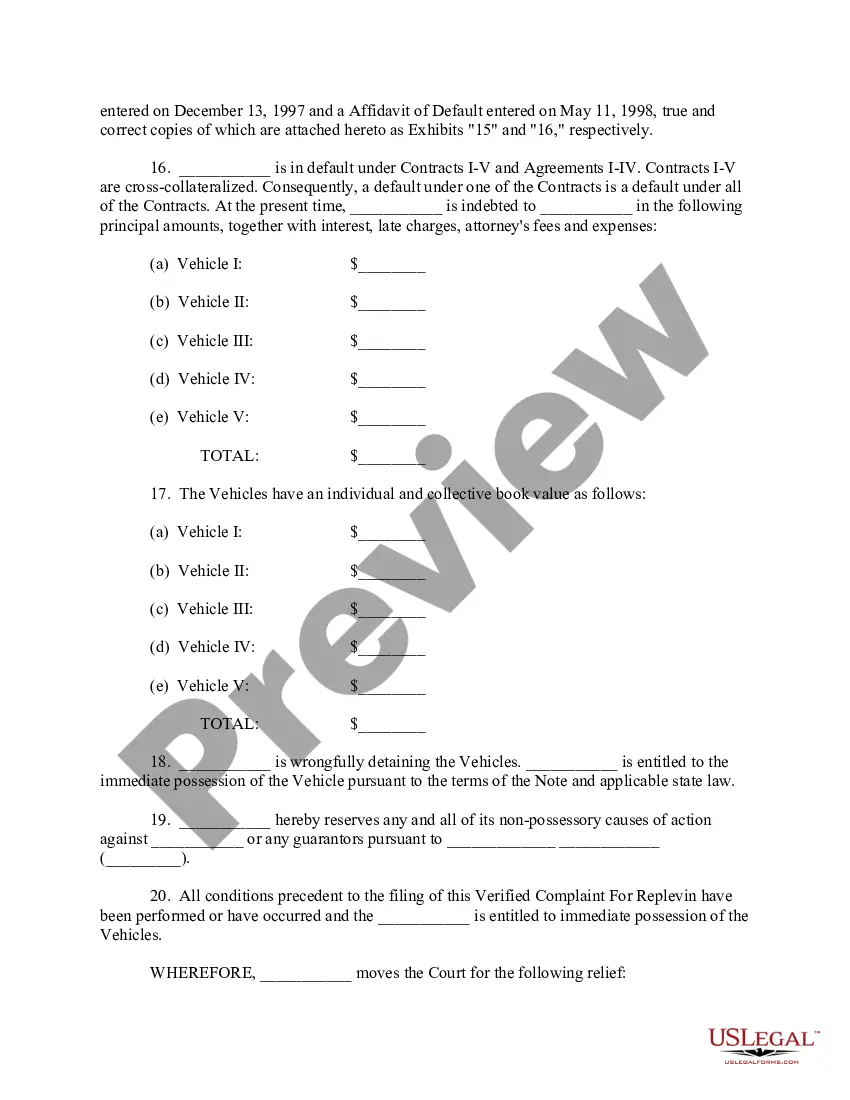

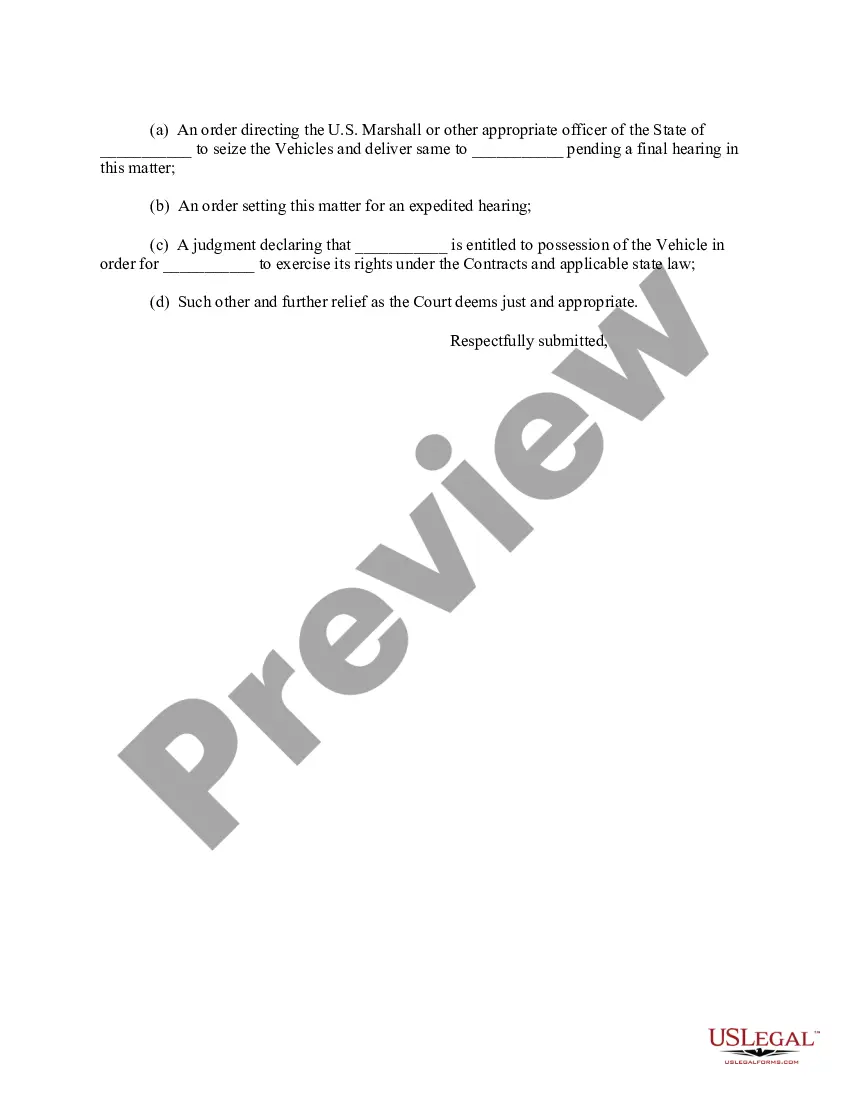

This form is a Verfied Complaint for Replevin. The plaintiff has filed this action against defendant in order to replevy certain property in the defendant's possession.

Complaint Repossession Document Form California In Pennsylvania

Instant download

Description

Free preview

Form popularity

FAQ

Direct Dispute with the Lienholder: Even though the lienholder has refused to remove the repossession, consider sending them a formal dispute letter. In the letter, outline the timeline of events, provide evidence of the insurance payout, and explain why the repossession should not be considered a default on your part.

To attempt to remove repossession from your credit report, you need to initiate a credit dispute and prove to the credit bureaus that the repossession is fraudulent, outdated or otherwise inaccurate.

In California, a consumer's vehicle can be taken from them if they miss payments on their loan or if they violate any terms of their agreement. This process is known as repossession and the creditor has the right to repossess the consumer's vehicle if it holds a valid security interest in it.

Under Pennsylvania law, lenders can repossess a borrower's car if they default on the loan. Though this could mean letting your insurance lapse, most repos happen because borrowers get behind on their car payments. Your loan agreement will outline exactly what default means to your lender.

Ideally, you should start these negotiations before the repossession process. If you negotiate after repossession, however, you may be able to use any questionable actions by the lender during that process to help bolster your bargaining position.

Dispute Inaccurate Information Initiate a formal dispute with all necessary credit reporting agencies (CRAs) that issued the report containing the repossession. You can dispute a repossession online with all three credit reporting agencies, and this is the most efficient way to pursue removal: Experian. Equifax.

Reinstate the Loan Car repossession happens when you default on the loan, so you can get the car back by reinstating the loan. That means you'll catch up on your loan payments, so you no longer have an outstanding balance.

Although court judgments no longer appear on credit reports or factor into credit scores, they're still part of the public record. If a lender looks up your public records, this could make it harder to qualify for future loans.

You can also use websites like Carfax, Auto Trader, Buy It Now, eBay and CarsDirect. All these websites provide information about repossessed cars.

Under Pennsylvania law, lenders can repossess a borrower's car if they default on the loan. Though this could mean letting your insurance lapse, most repos happen because borrowers get behind on their car payments. Your loan agreement will outline exactly what default means to your lender.

More info

If the repo company breaches the peace, you can file a complaint with this department. If you missed payments and received harassing phone calls or threatening gestures, our California lawyers can sue for a wrongful repossession for you.I certify that I, or the firm, company, or corporation I am authorized to represent, am the legal owner within the meaning of California Vehicle Code. File a complaint online (opens in a new tab). California law permits cars to be repossessed after one late or missed loan payment. Complaint Information. Please explain your complaint: Try to be brief, but be sure to tell WHAT happened, WHEN it happened and WHERE it happened. Sit down and document everything that was left in the car. Get free legal advice and find a free or lowcost lawyer. If you suspect fraud on a debit transaction, you can now file a claim in the mobile app.