Complaint Repossession With Credit Card In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Bottom line. If you're having issues with a financial service provider – be it with overdraft fees, a HELOC or student loans – filing a complaint with the CFPB can help you get to a resolution.

Consistent with applicable law, we securely share complaints with other state and federal agencies to, among other things, facilitate: supervision activities, enforcement activities, and. monitor the market for consumer financial products and services.

Contact your card issuer via the phone number on the back of the card or the issuer website's live-agent chat. Tell the customer service representative that you think you were the victim of fraud. The agent may have you confirm recent transactions to be sure any authentic purchases are processed correctly.

When it comes to credit card debt relief, it's important to dispel a common misconception: There are no government-sponsored programs specifically designed to eliminate credit card debt. So, you should be wary of any offers claiming to represent such government initiatives, as they may be misleading or fraudulent.

We protect consumers from unfair, deceptive, or abusive practices and take action against companies that break the law. We arm people with the information, steps, and tools that they need to make smart financial decisions.

Once a company receives a complaint from the CFPB, it is responsible for responding within 15 calendar days. If the response is not final, the company is responsible for letting the CFPB know. They will then have up to 60 days to provide a final response.

We have supervisory authority over banks, thrifts, and credit unions with assets over $10 billion, as well as their affiliates.

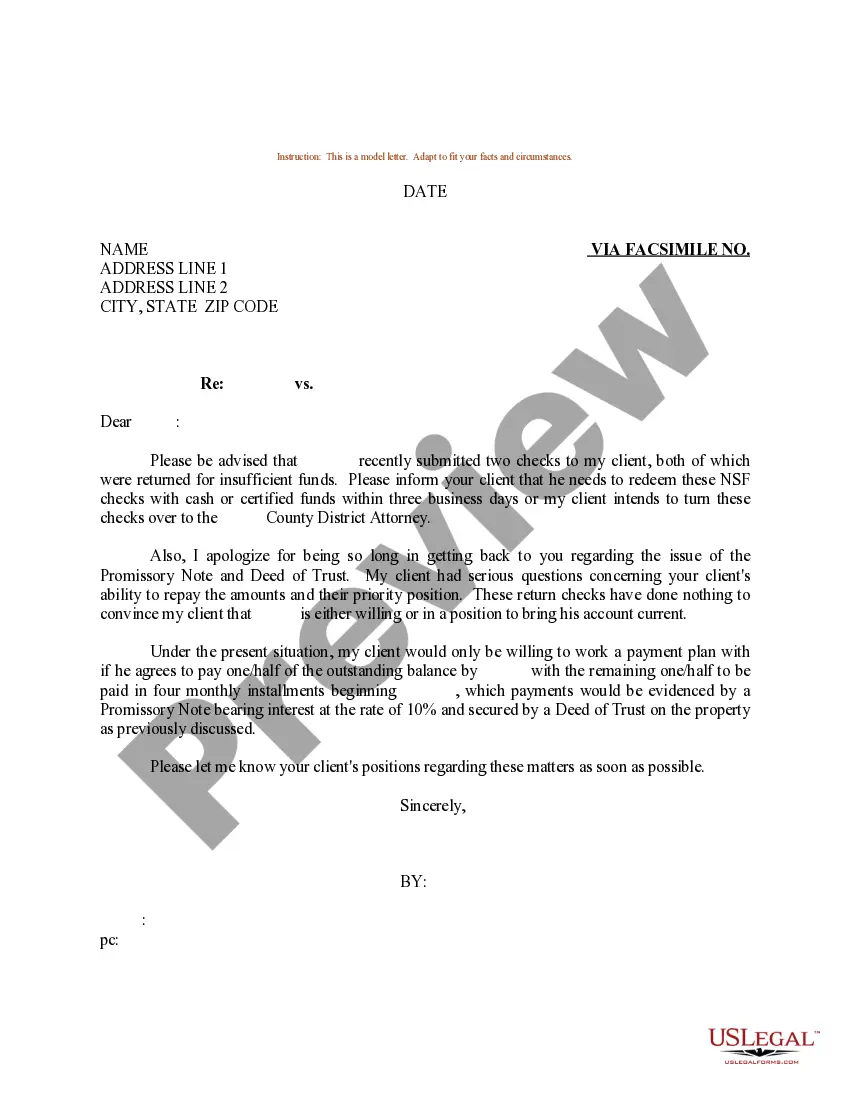

Direct Dispute with the Lienholder: Even though the lienholder has refused to remove the repossession, consider sending them a formal dispute letter. In the letter, outline the timeline of events, provide evidence of the insurance payout, and explain why the repossession should not be considered a default on your part.

Consistent with applicable law, we securely share complaints with other state and federal agencies to, among other things, facilitate: supervision activities, enforcement activities, and. monitor the market for consumer financial products and services.