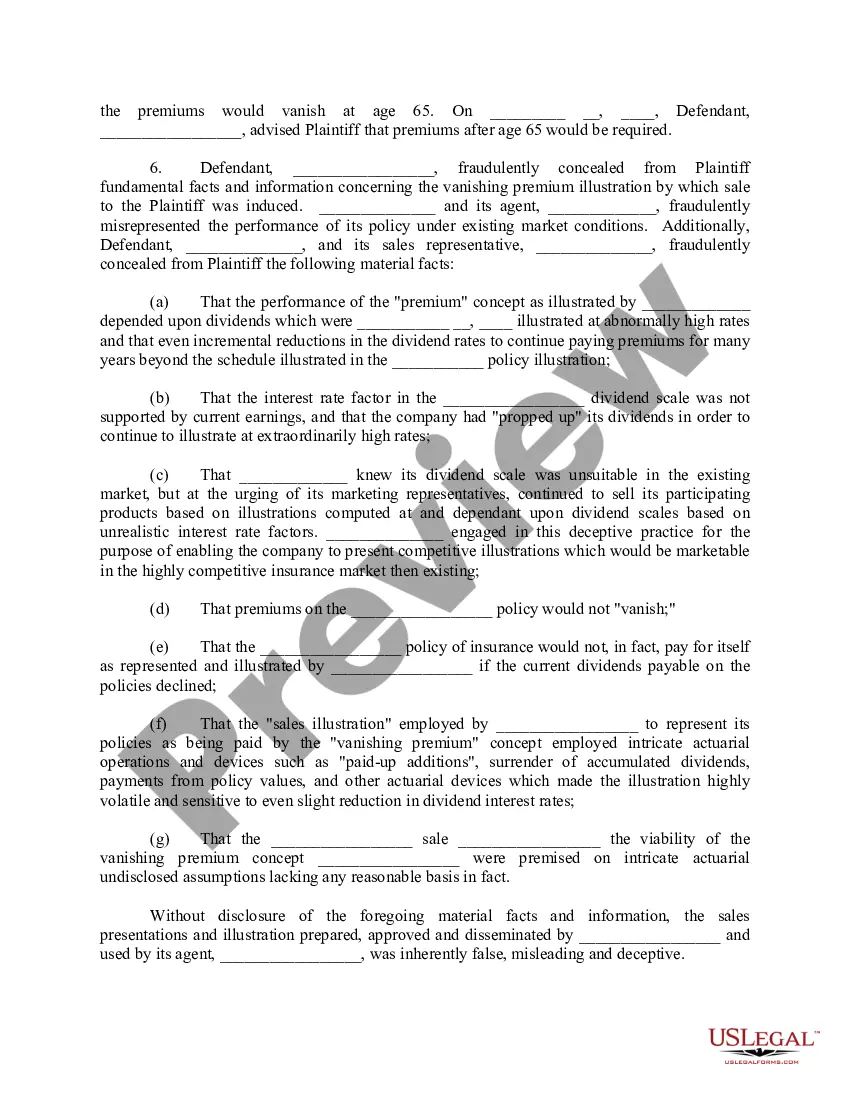

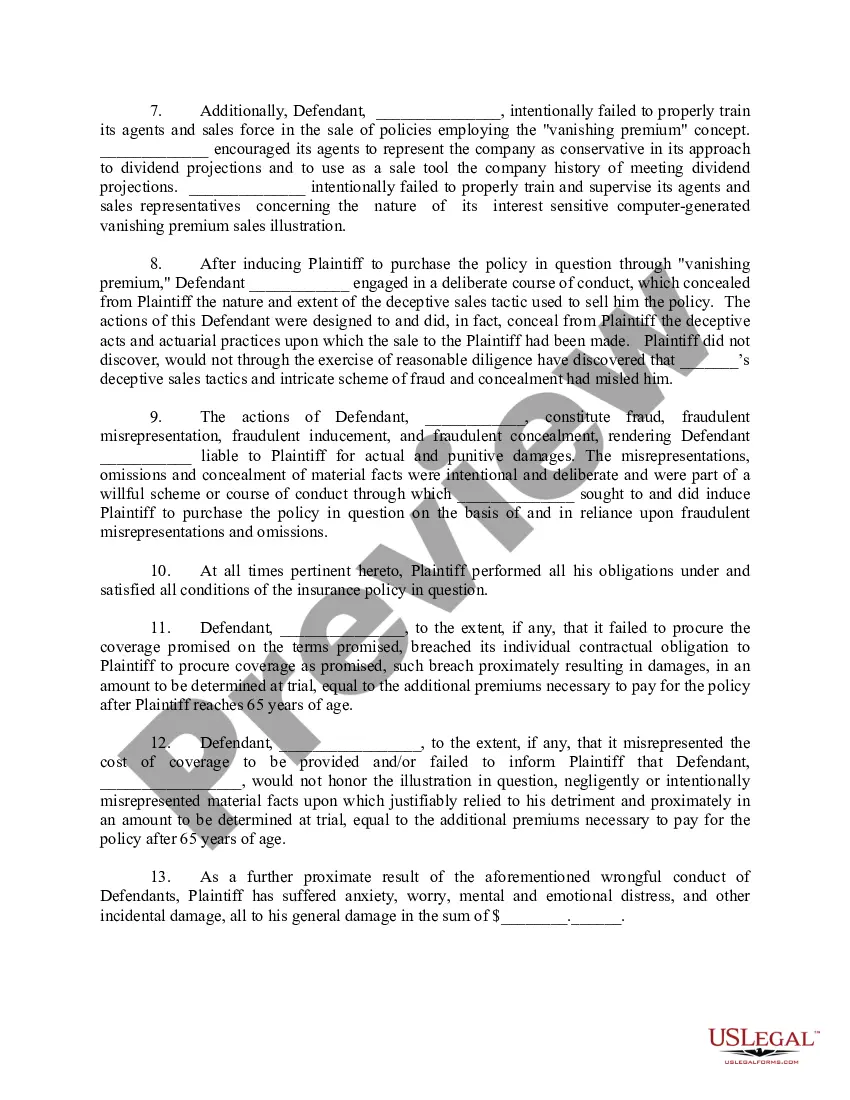

This is a Complaint pleading for use in litigation of the title matter. Adapt this form to comply with your facts and circumstances, and with your specific state law. Not recommended for use by non-attorneys.

Unfair Trade Practices In Insurance In Kings

Category:

State:

Multi-State

County:

Kings

Control #:

US-000289

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Misrepresentation Representing that goods or services are of a particular quality, style or model if that representation is untrue. Making false or misleading statements about the condition of used goods. Representing goods as new when they are used, deteriorated, altered or reconditioned.

What Is Unfair Claims Practice? Unfair claims practice is the improper avoidance of a claim by an insurer or an attempt to reduce the size of the claim. By engaging in unfair claims practices, an insurer tries to reduce its costs. However, this is illegal in many jurisdictions.

(These practices are commonly called misleading or unfair business practices.) They include false advertising, misrepresentation, tied selling, and failing to comply with regulations. Under consumer protection laws, they are illegal and can lead to compensatory or punitive damages.

Types of Unfair Trade Practices ① Refusal to Deal. ② Discriminatory Treatment. ③ Exclusion of a Competitor. ④ Unfair Solicitation of Customers. ⑤ Coercion of Transaction. ⑥ Abuse of Superior Bargaining Position. ⑦ Imposing Binding Conditional Trade. ⑧ Obstruction of Business Activities.

Refusing to Settle for Policy Limits: If an insurer unreasonably refuses to settle a liability claim for policy limits and exposes the insured's personal assets to enforcement of a judgment, this practice can constitute bad faith.

The correct answer is B) Refusing coverage based on age. An example of unfair trade practice of discrimination by an insurer is refusing coverage based on age, as it involves unequal treatment without actuarial justification.

An example of unfair trade practice of discrimination by an insurer is refusing coverage based on age, as it involves unequal treatment without actuarial justification. Charging lower rates for non-smokers, using actuarial tables, or providing safe driving discounts are lawful as they're based on risk evaluation.

In general, an insurance company must not falsely advertise or misrepresent the nature of an insurance policy or its benefits, discriminate between similarly situated individuals in determining benefits eligibility, engage in unfair claim settlement practices, or fail to maintain a record of grievances.

Some instances of unfair claims settlement practice may involve issues with timeliness on the part of insurers. Examples of specific timeliness issues could involve: Failure to provide a timely explanation for the denial of coverage or a low settlement offer.

More info

An unfair claims practice is what happens when an insurer tries to delay, avoid, or reduce the size of a claim that is due to be paid out to an insured party. Section 2. Definitions.Your first step in an unfair competition lawsuit is contacting an experienced attorney who can defend your company. The public interest (5 M.R.S.A. § 209). Before reaching out to the Consumer Services Division about your dispute, contact your insurance company and ask them to resolve the issue. Consumers and businesses can report business practices and behaviours that concern them. Insureds also may have claims pursuant to New Mexico's Unfair Trade Practices Act NMSA 1978 § 57-12-10. Acts or practices that may be unfair discrimination in the business of insurance in this state. Insurance fraud in the U.S. residential and commercial real estate construction industries. President Biden is driving a small business boom with American entrepreneurs filing a record nearly 20 million new business applications since he took office.