Contract For International Sale Of Goods With Foreign Currency In California

Description

Form popularity

FAQ

US Sales Tax for International Sellers. International retailers are still required to collect sales tax from US buyers if they have physical or economic nexus in one or more US states.

An international contract is an agreement signed between resident parties living in different countries to perform certain activities for a specific purpose.

Additionally, California enforces a use tax on goods purchased from out-of-state sellers, requiring compliance with state-based taxation on imported tangible personal property. It's crucial for businesses to consider both federal and state taxes when calculating total import costs.

Certain properties, or portions of properties, are exempt from taxation under the California Constitution. The most common types are homeowner, disabled veterans, welfare, charitable, and institutional exemptions. Visit the Assessor's Exemption webpage for more information.

The state's largest manufacturing export category is computer and electronic products, which accounted for $41.0 billion of California's total goods exports in 2023.

To be exempt as an export the property must be intended for a destination in a foreign country, it must be irrevocably committed to the exportation process at the time of sale, and must actually be delivered to the foreign country prior to any use of the property.

FINAL THOUGHTS ON THE CALIFORNIA IMPORT TAX (USE TAX) The California use tax rate is the same rate as the sales tax rate of 7.5% and is generally due on purchases made from out-of-state sellers or on items brought into the state for either storage or use.

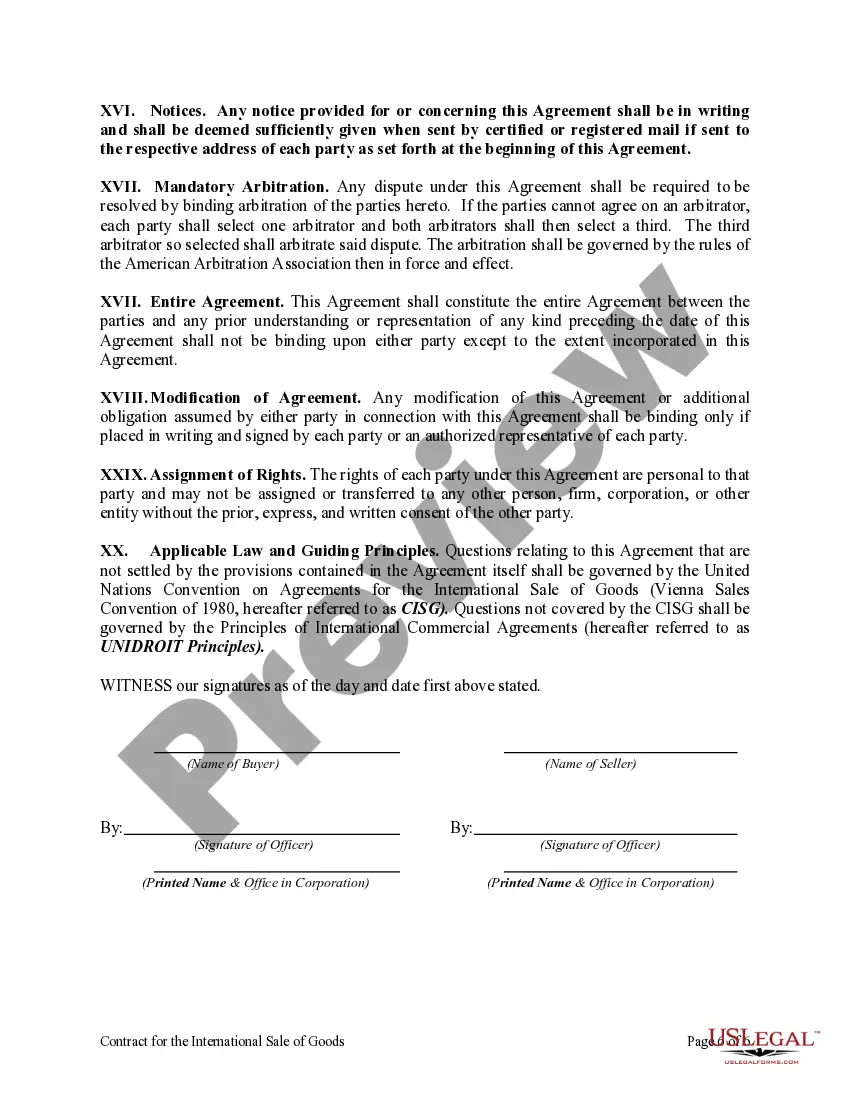

In an international business contract, it's essential to define the jurisdiction that will govern the contract and the laws that will apply in the event of a dispute. Your dispute resolution section should also detail the agreed-upon dispute resolution mechanism.