Loan Agreement Form Download With Collateral Philippines In Oakland

Description

Form popularity

FAQ

A contract, under Philippine law, becomes binding as soon as there is mutual consent between the parties, consideration (payment or exchange of services), and a lawful object (subject matter of the agreement). These elements are enough to form a valid and enforceable contract, even without notarization.

Lending agreements are governed by the Civil Code of the Philippines, along with other relevant laws such as the Lending Company Regulation Act and the Usury Law, although the latter is largely outdated due to the Central Bank's removal of interest rate ceilings.

While not required by law, having the promissory note notarized can provide additional legal protection and evidentiary weight in court should any dispute arise over its enforcement.

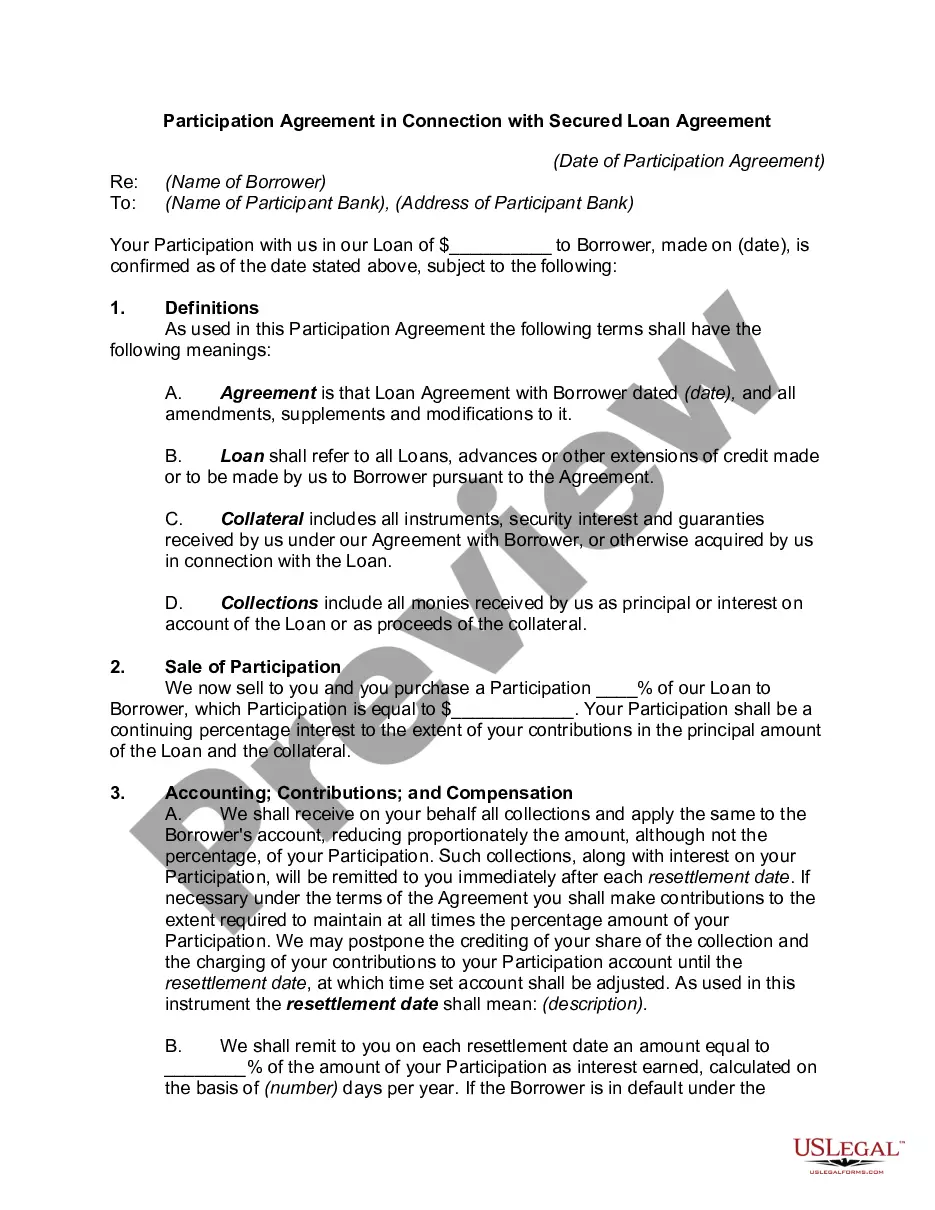

Examples of collateral documents are a security agreement, guarantee and collateral agreement, pledge agreement, deposit account control agreement, securities account control agreement, mortgage, and UCC-1s.

Non-Transferable Assets: Assets that are legally restricted from being transferred, such as government benefits, social security payments, or certain insurance policies, cannot be used as collateral since they cannot be seized or sold.

Collateral documents include any documents granting a security interest in collateral by the borrower, parent or subsidiary in favor of the lender and all other documents required to be executed or delivered pursuant to those documents. Collateral documents do not include guaranties.