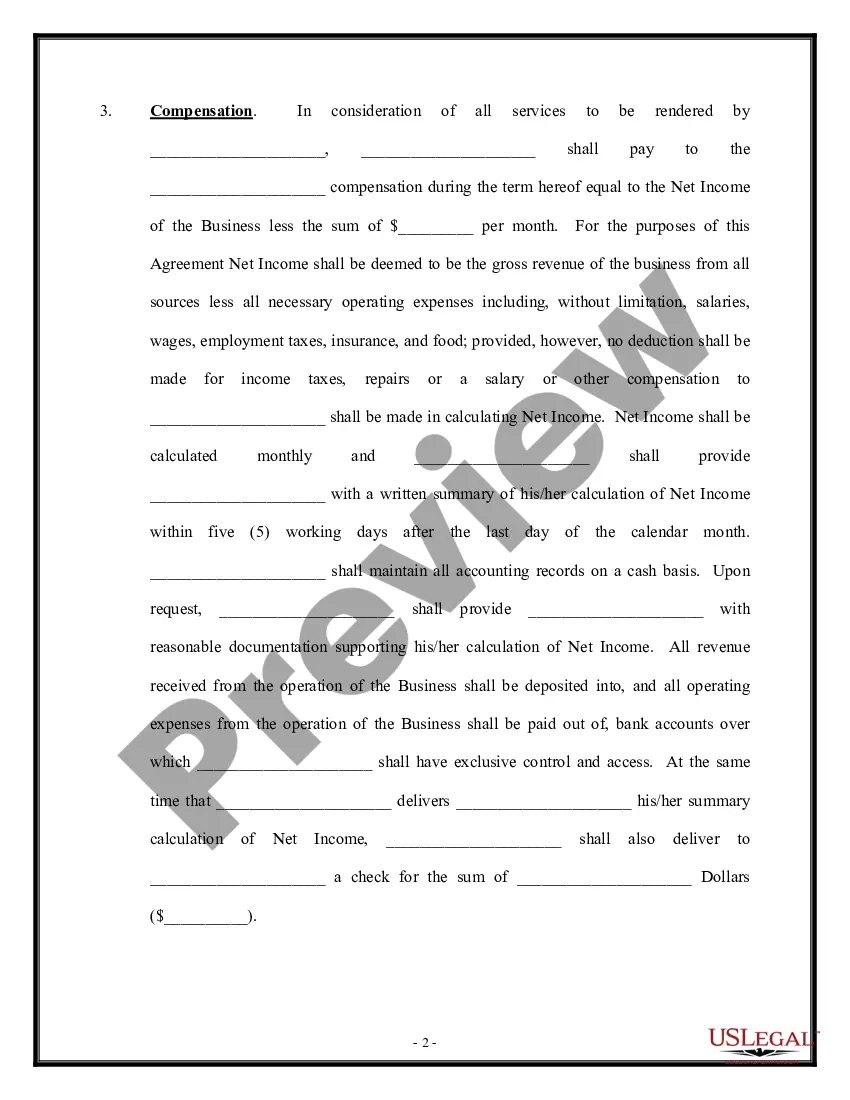

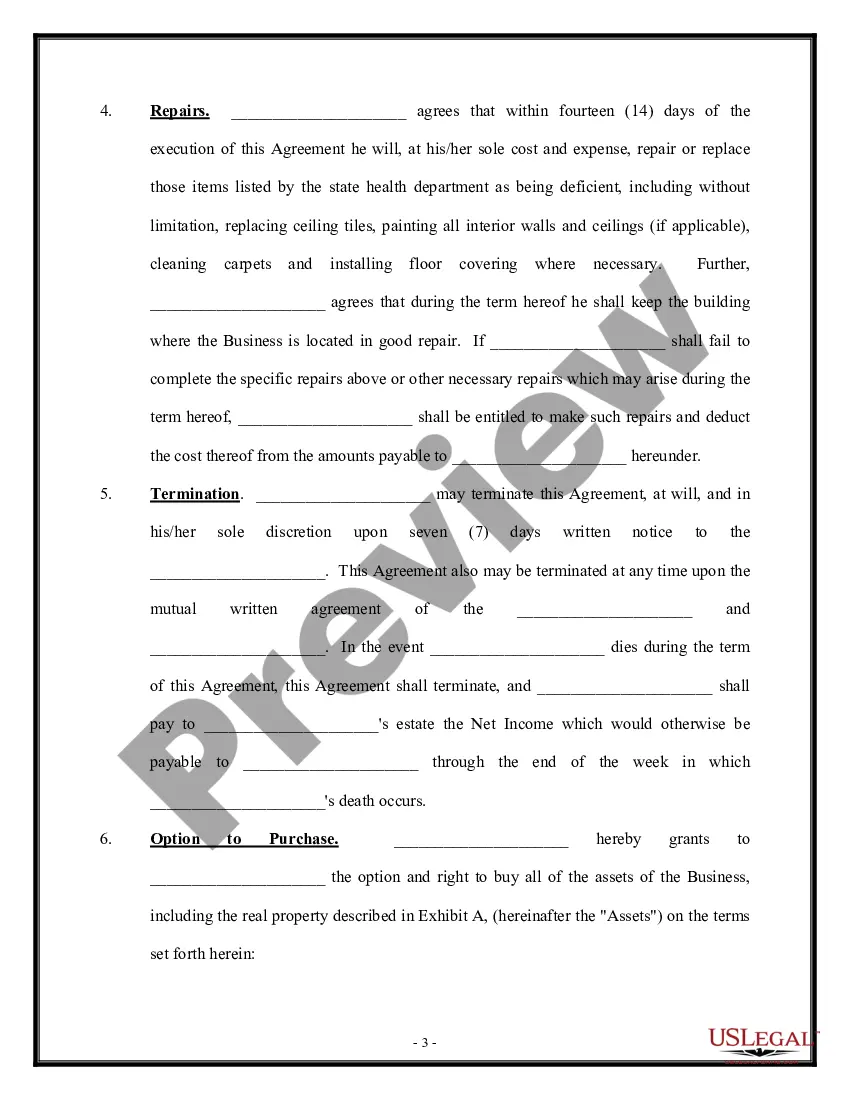

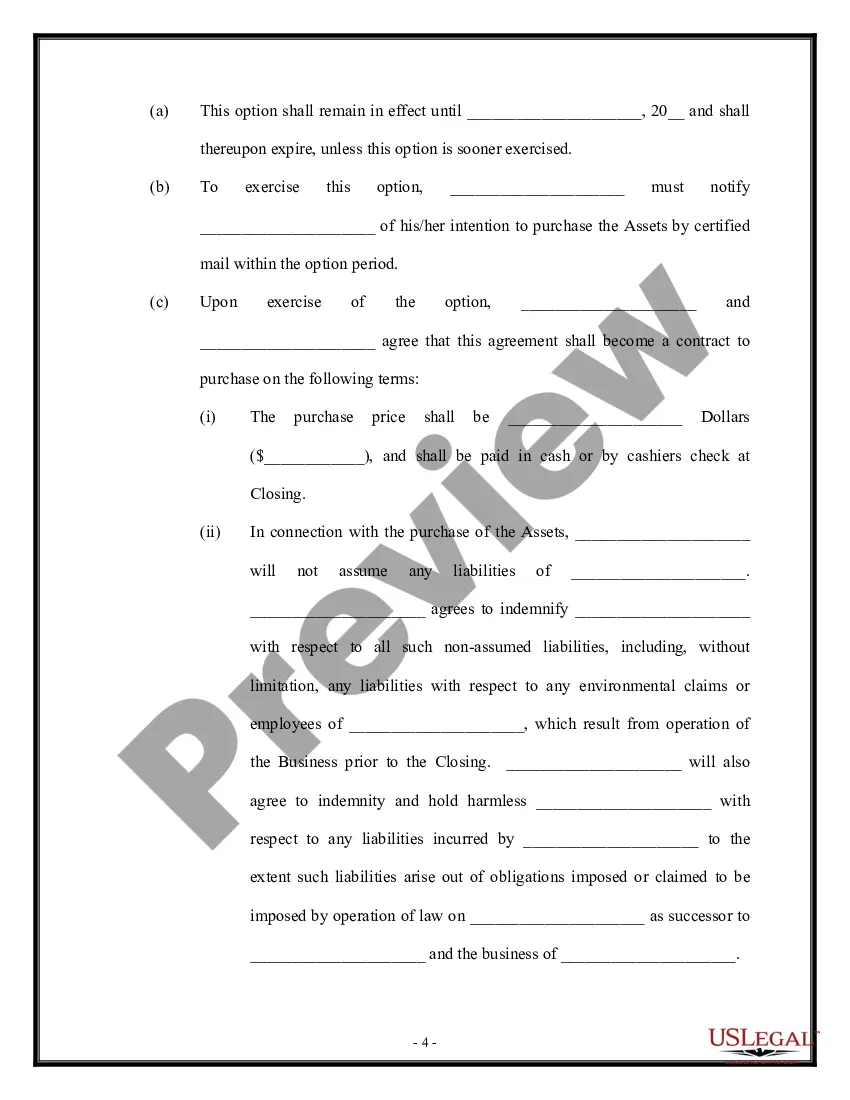

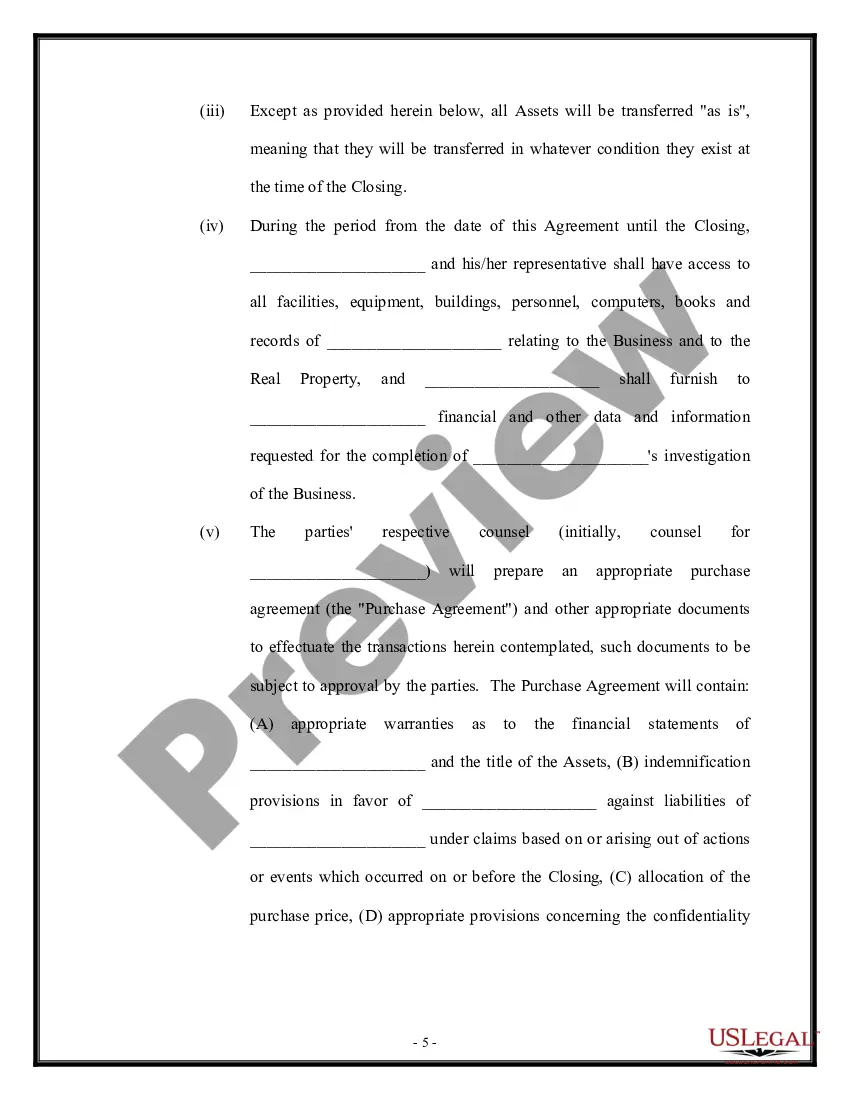

The parties have entered into an agreement whereby one party has been retained to manage and operate a certain business. Other provisions of the agreement.

All Business Purchase With Bitcoin In Florida

Category:

State:

Multi-State

Control #:

US-00059

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

There are two common ways to accept crypto as a merchant: through a crypto wallet or gateway. You can use a crypto wallet to accept directly from a customer's crypto wallet. However, the funds will remain in cryptocurrency form until you transfer them to a crypto exchange.

10 years ago: A $1 investment would be worth $277.66 since Bitcoin is up 26,967 percent from December 2014.

Widely accepted wallets in Florida include ZenGo, Ledger, MetaMask, Trust Connect and Atomic Wallet.

Complete IRS Form 8949 Summary: Report all your disposals of cryptocurrency — short-term and long-term — on Form 8949.

There are two common ways to accept crypto as a merchant: through a crypto wallet or gateway. You can use a crypto wallet to accept directly from a customer's crypto wallet. However, the funds will remain in cryptocurrency form until you transfer them to a crypto exchange.

The bottom line is that even though there is a lot of privacy around crypto transactions, the IRS will find out if you have taxable crypto transactions. If you don't report them, you stand to incur penalties and potentially even criminal charges.

Tax forms from Coinbase If you earned less than $600 in crypto income, you won't receive a 1099-MISC form from Coinbase. If you're a US customer who traded futures, you'll receive a 1099-B for this activity by email and in Coinbase Taxes.

Buying crypto as an LLC is more or less the same as when you buy as an individual. You simply acquire crypto through accounts associated with the LLC, as you would as an individual trader. Many popular exchanges support institutional accounts, including Coinbase, Kraken, and Binance.

Because cryptocurrency transactions are pseudo-anonymous, many investors believe that they cannot be traced. This is not true. Most major blockchains have publicly visible transactions. That means that the IRS can track crypto transactions simply by matching 'anonymous' transactions to known individuals.

Key Takeaways. The IRS treats cryptocurrency as property, meaning that when you buy, sell or exchange it, this counts as a taxable event and typically results in either a capital gain or loss.

More info

First, you'll want to set yourself up with a good bitcoin payment processor. This will go a long way towards creating a more efficient experience.Title Partners of South Florida offers a unique service for Bitcoin, Ethereum and other cryptocurrency real estate transactions. Find the closest place to buy or spend your crypto assets anywhere in the world. As a crypto trader or crypto business you may want to consider an LLC to streamline taxes and protect assets. Here's what you need to know. Selling virtual currency in, from or into Florida may require a money services business license and the maintenance of an anti-money laundering program. Florida does not address the sales and use tax treatment of transactions involving bitcoin or other virtual currency. Georgia. At this time, Florida has no state income tax. The law defines virtual currency under FL Stat § 560.103 and explicitly includes virtual currency transmitters in the scope of FL Stat § 560.