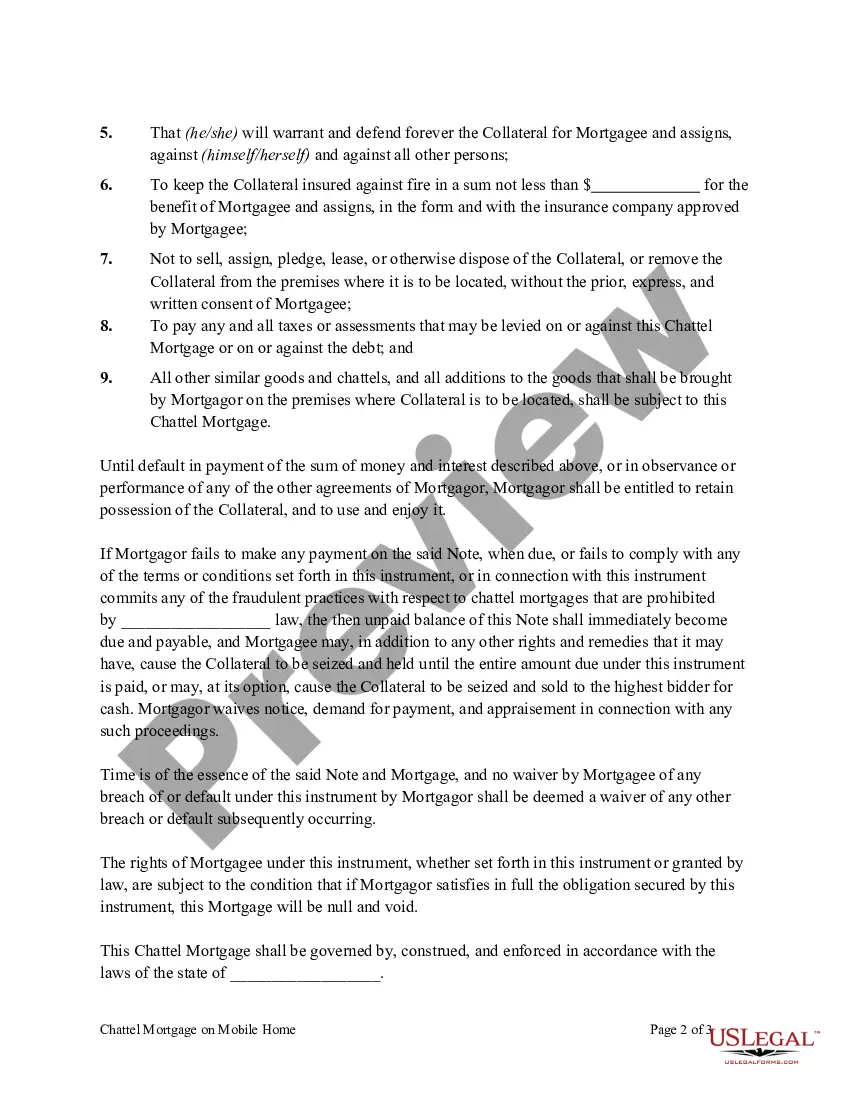

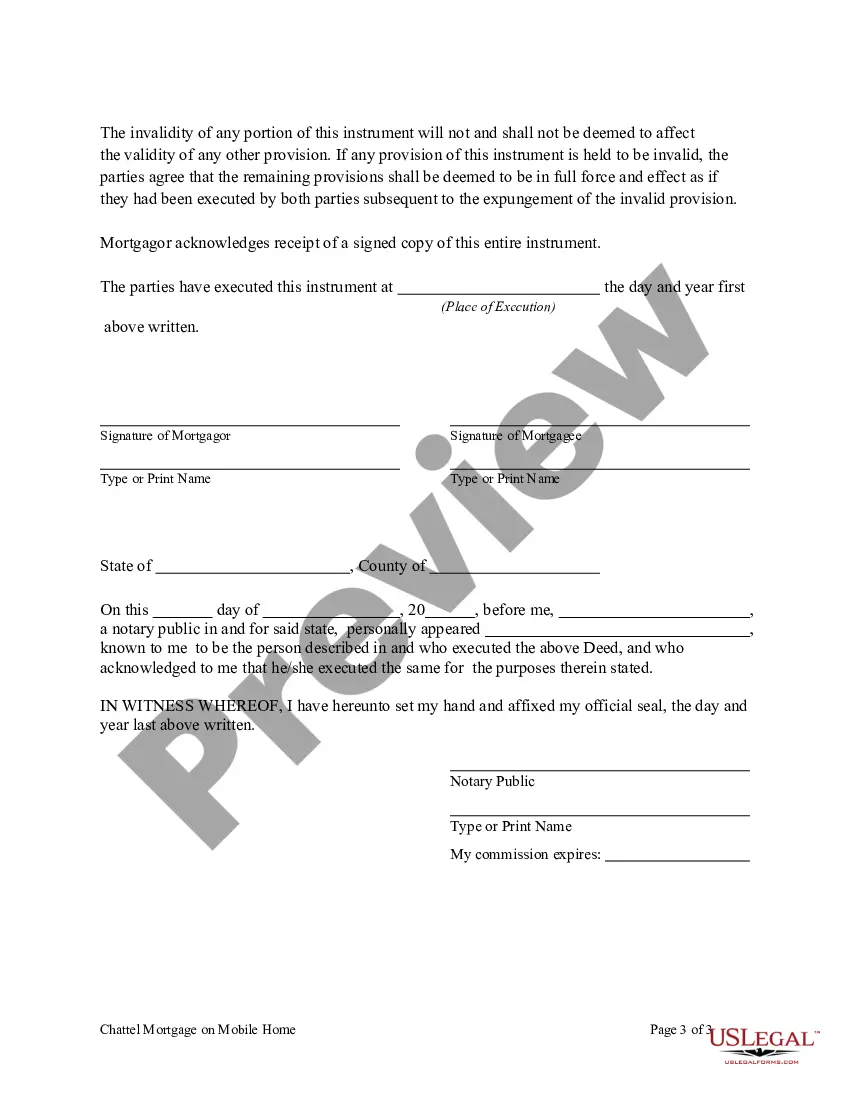

Chattel Mortgage Form With Extra Judicial Foreclosure In Arizona

Description

Form popularity

FAQ

A judicial foreclosure begins when the lender files a lawsuit asking a court for an order allowing a foreclosure sale. If you don't respond with a written answer, the lender will automatically win the case. But if you choose to defend the foreclosure lawsuit, the court will review the evidence and determine the winner.

If the borrower's outstanding debt exceeds the property's current market value, the lender may refuse to proceed with a deed in lieu of foreclosure.

Once the property is sold at a foreclosure sale, the borrower generally loses ownership rights. However, in some cases, the borrower may have a redemption period to reclaim the property by paying off the debt in full.

Federal law states that a bank may initiate foreclosure after 120 days of missed payments.

Answer: After a judicial foreclosure in Arizona, the debtor or his successors in interest ordinarily may redeem at any time at any time within six months after the date of the sale (A.R.S. 33-12-1282).

In Arizona, the trustee starts the foreclosure process by the recording of a notice of sale in the county recorder's office. The notice must include the date, time, and place of the sale. The sale date can't be sooner than the 91st day after the notice of sale's recording date.

A Deed in Lieu of Foreclosure is a contractual agreement between a borrower and a lender. In this arrangement, the borrower willingly transfers the property to the lender, who, in turn, forgives the borrower's mortgage debt, thereby avoiding a lengthy foreclosure process.

Non-judicial foreclosures are the most commonly used form of foreclosure in Arizona, and are governed by Chapter 6.1 of Title 33 of the Arizona Revised Statutes (A.R.S. §§ 33-801 to 33-821).