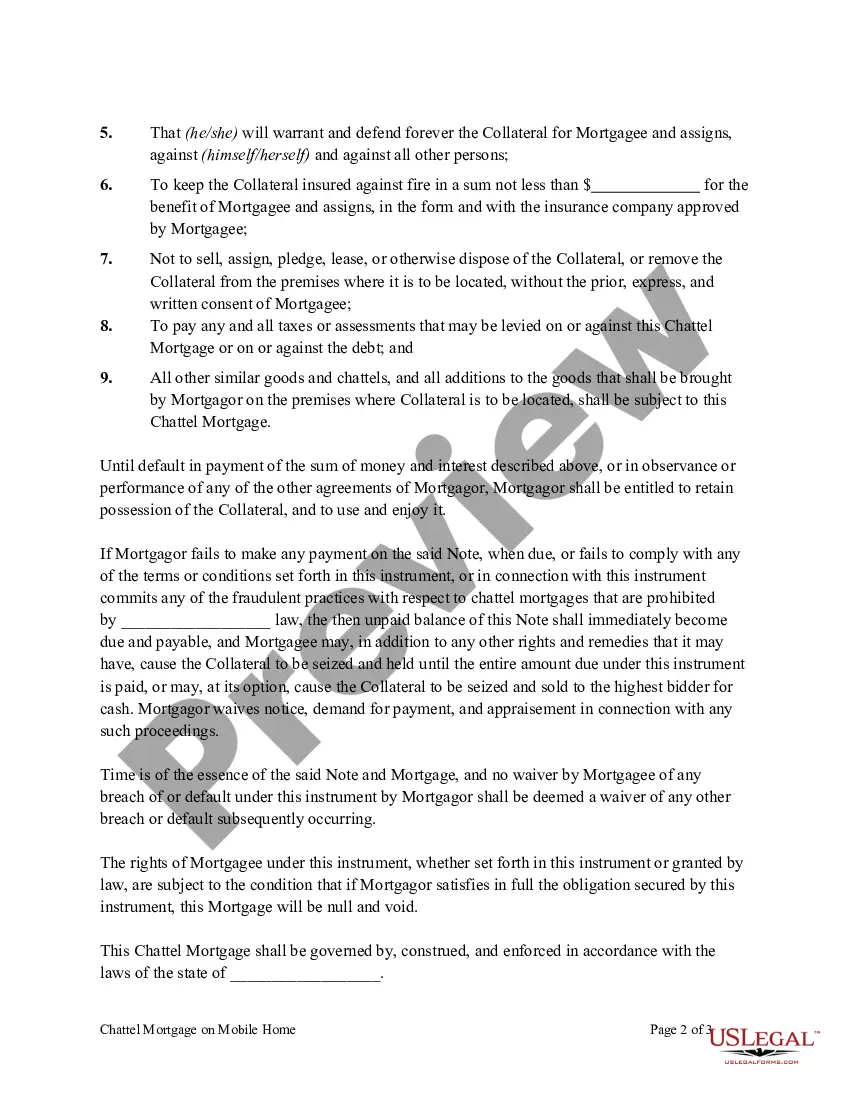

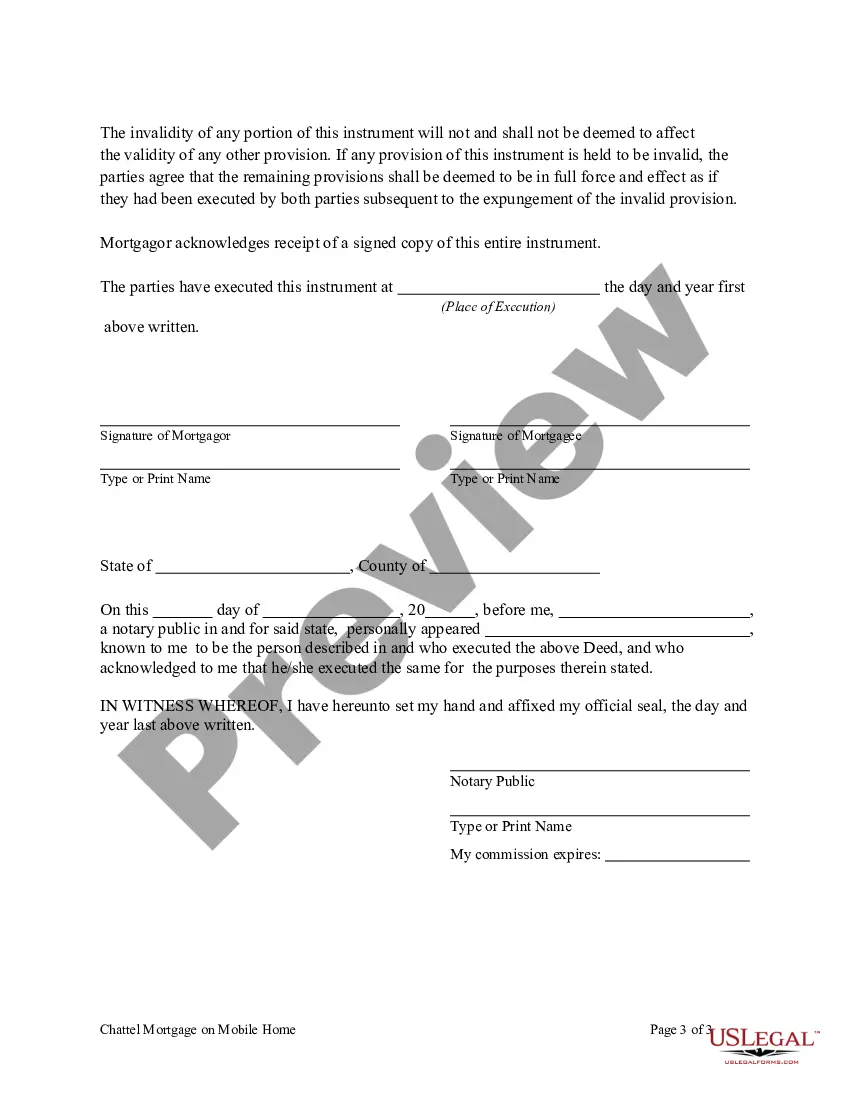

Chattel Mortgage Form With Balloon In California

Description

Form popularity

FAQ

Let's say a person takes out a $200,000 mortgage with a seven-year term and a 4.5% interest rate. Their monthly payment for seven years is $1,013. At the end of the seven-year term, they owe a $175,066 balloon payment.

However, the larger balloon payment at the end represents a substantial financial obligation that needs to be carefully planned and managed. Accounting Treatment: The balloon payment is usually recorded as a liability in the financial statements until it becomes due.

The most significant risk of a balloon mortgage is foreclosure if the borrower can't make the balloon payment at the end of the term. Foreclosure can result in the loss of the home, emotional distress, and impact the borrower's credit negatively, generally for seven years.

The low initial payments of a balloon mortgage may attract first-time homebuyers or those buying a full-time residence, but these may not be the ideal borrowers for lenders. The optimal buyers for a balloon mortgage are short-term homebuyers, experienced homeowners, real estate investors, and commercial developers.

What Is Prohibited In a Qualified Mortgage? Qualified mortgages prohibit risky practices like ballooning payments, interest-only periods, and negative amortization.

Balloon mortgages are short-term loans that begin with a series of fixed payments and end with a final, lump-sum payment. That one-time payment is called a balloon payment because it's often at least twice as much as the previous ones, leaving many borrowers with a final bill for tens of thousands of dollars (or more).

Potential Downsides of Balloon Mortgages for Homebuyers Foreclosure can result in the loss of the home, emotional distress, and impact the borrower's credit negatively, generally for seven years. The first balloon mortgage payments primarily cover the interest rather than the principal.

Balloon mortgages are short-term loans that begin with a series of fixed payments and end with a final, lump-sum payment. That one-time payment is called a balloon payment because it's often at least twice as much as the previous ones, leaving many borrowers with a final bill for tens of thousands of dollars (or more).

The term of a balloon mortgage is usually short (e.g., 5 years), but the payment amount is amortized over a longer term (e.g., 30 years). An advantage of these loans is that they often have a lower interest rate, but the final balloon payment is substantial.