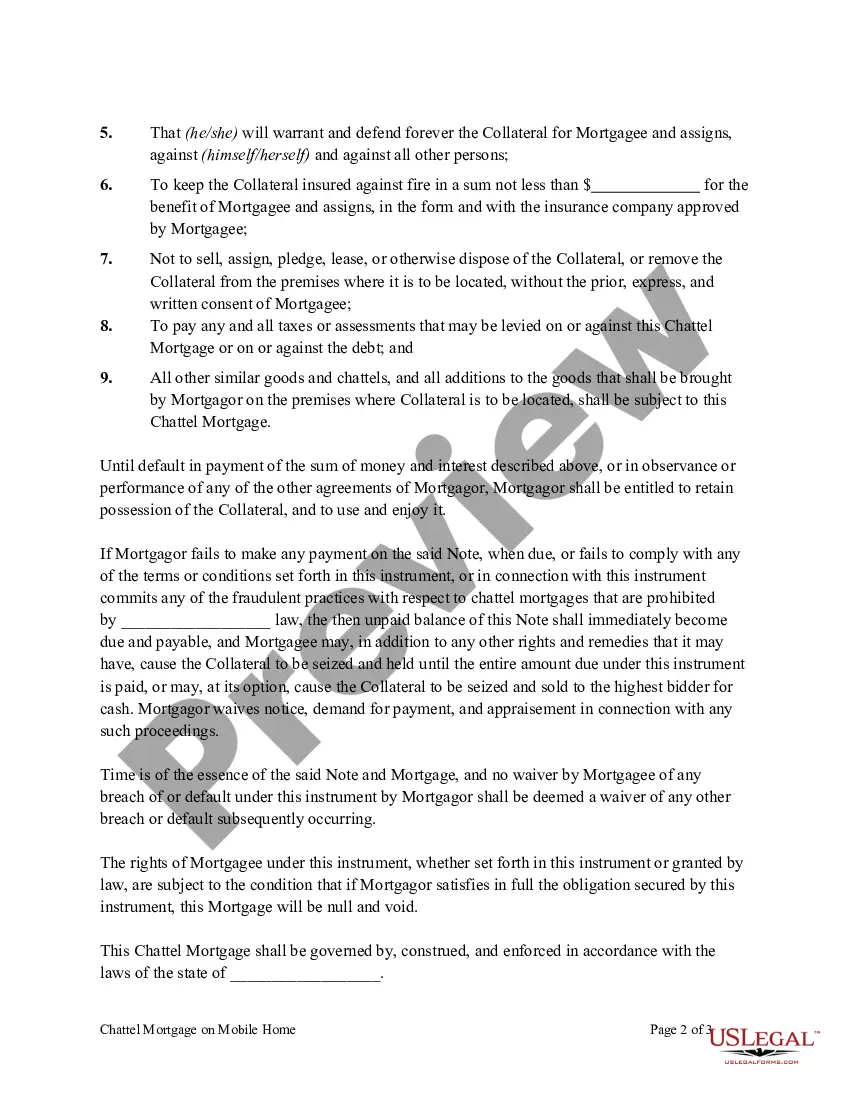

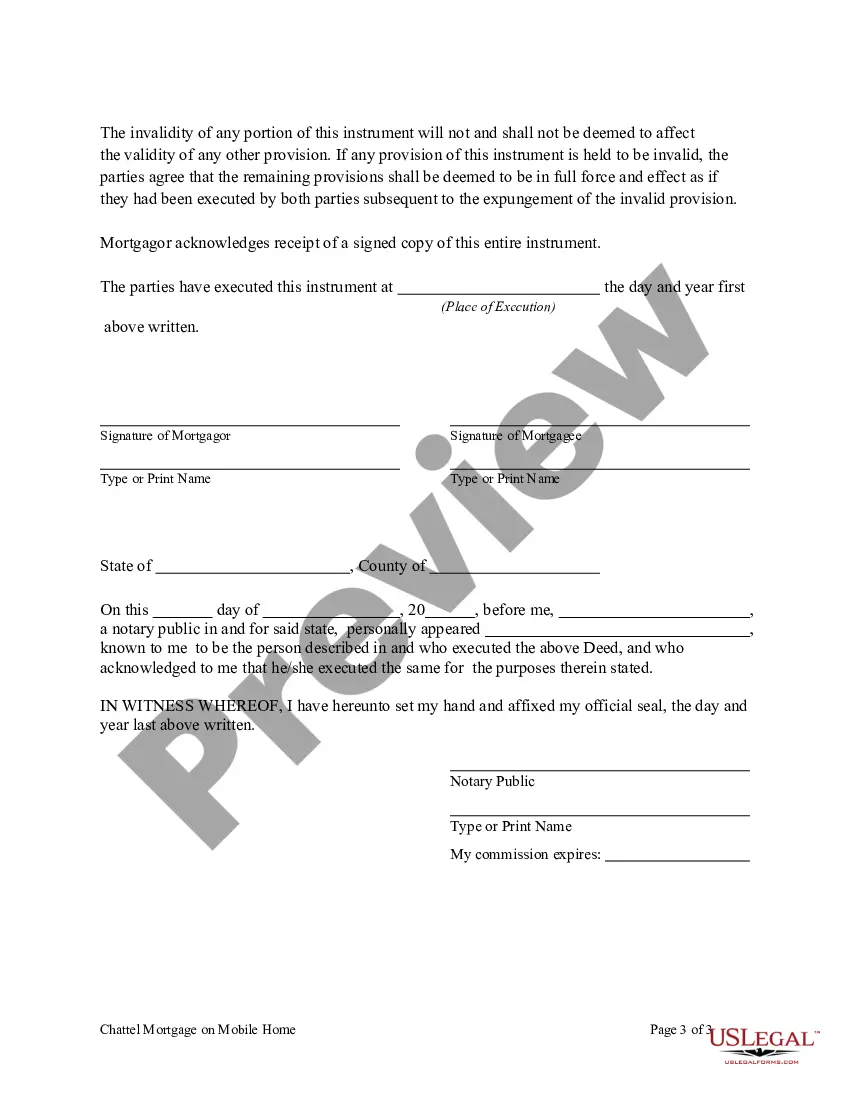

Chattel Mortgage Form With Extra Judicial Foreclosure In Cuyahoga

Description

Form popularity

FAQ

There are three main types of foreclosure: judicial, non-judicial, and strict. Judicial foreclosure is the most common. It is also the only type of foreclosure used in Ohio. Under Ohio law, a lender must get a court order to foreclose on your property.

Ohio is a judicial foreclosure state. This means that the Ohio court system oversees the foreclosure process, and banks must file a lawsuit and seek court approval in the form of a judgment before completing a foreclosure sale. Foreclosure is a complicated process.

In Ohio, the foreclosure process can take anywhere from six to 18 months or longer. How long will a foreclosure action or bankruptcy stay on my credit report? A foreclosure stays on your credit report for seven years, and a bankruptcy stays on for 10 years.

In Ohio, the foreclosure process can take anywhere from six to 18 months or longer. How long will a foreclosure action or bankruptcy stay on my credit report? A foreclosure stays on your credit report for seven years, and a bankruptcy stays on for 10 years.

Some states also provide foreclosed borrowers a redemption period after the foreclosure sale, during which they can buy back the home. In Ohio, you have a right to redeem up until the court confirms the sale. (Ohio Rev. Code § 2329.33).

Redemption Period: Next, the court has 30 days to confirm the sale, which means the entire process can take anywhere from a few days to a maximum of 90 days.

The states that had the shortest average foreclosure timelines (again, ing to ATTOM Data Solutions) in the third quarter of 2024 were: New Hampshire (165 days) Minnesota (172 days) Texas (181 days)

A nonjudicial mortgage foreclosure can take about 120 days, or four months, to complete. Judicial foreclosures vary depending on your state. In California, this process can take two to three years. If you've fallen behind on your mortgage payments, the threat of foreclosure can become overwhelming.

A mortgage servicer may not make a first notice or filing for foreclosure until the borrower is more than 120 days delinquent. The 120-day period under the rules is designed to give borrowers time to learn about workout options and file an application for mortgage assistance.