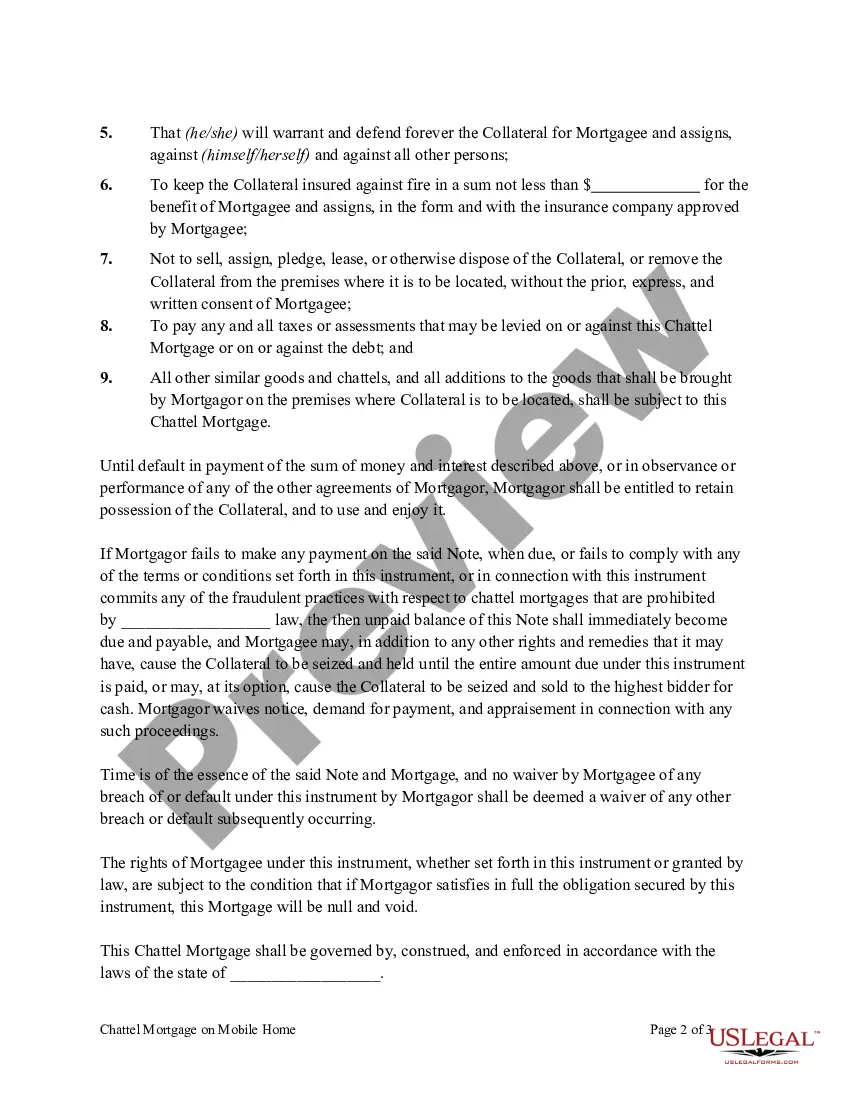

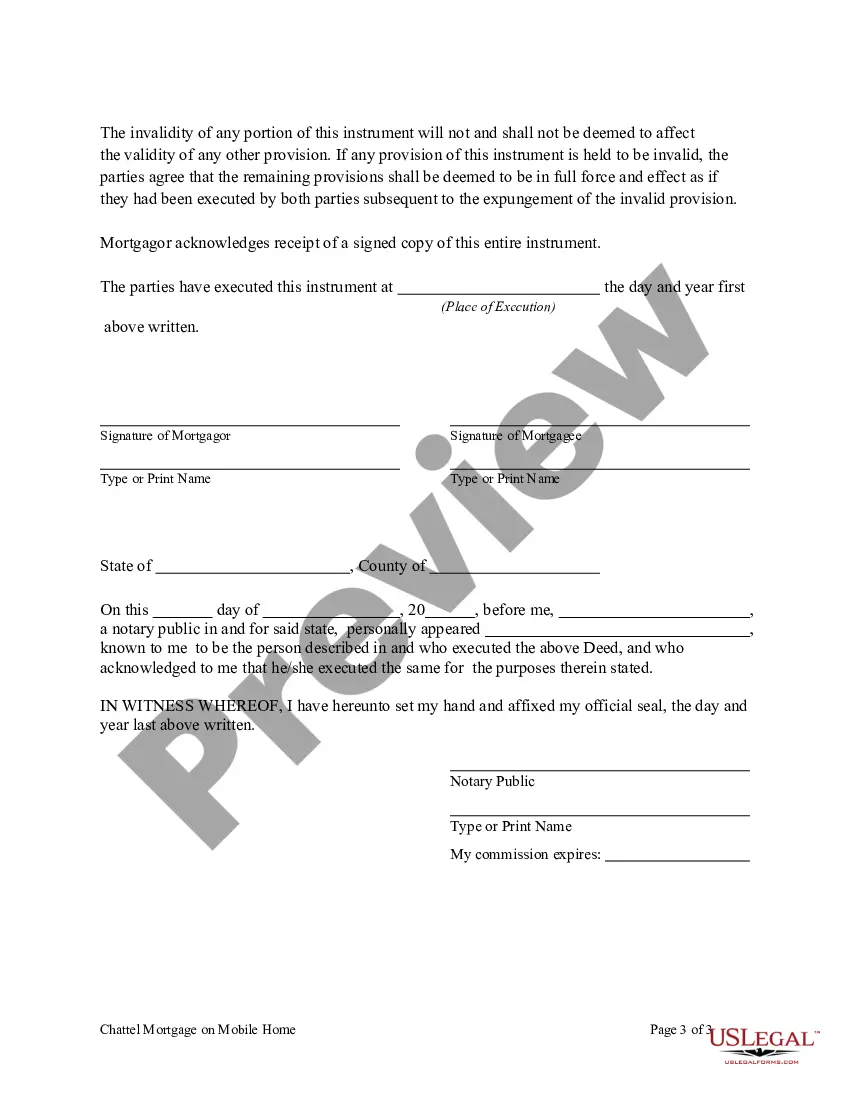

Chattel Mortgage Form With Balloon In Queens

Description

Form popularity

FAQ

The Bottom Line Chattel mortgages are a little-known but potentially good option if you're looking to finance a manufactured home or heavy equipment. These loans are smaller than conventional loans and tend to have higher rates, but they have shorter terms and quicker payoffs.

The downside of balloon payments Although a balloon-payment option can make your monthly payments more affordable, you're taking on extra debt to buy an asset that is depreciating – the value of your vehicle may end up less than the amount still owed.

In some cases, you may be able to negotiate with your finance provider to spread the balloon payment over monthly instalments – this is essentially what refinancing is. Doing this can help make the payment more manageable and reduce the financial strain of a large lump sum payment.

Balloon mortgages are short-term loans that begin with a series of fixed payments and end with a final, lump-sum payment. That one-time payment is called a balloon payment because it's often at least twice as much as the previous ones, leaving many borrowers with a final bill for tens of thousands of dollars (or more).

The traditional mortgage is only for stationary property. It's suited for long-term real estate investments. Chattel loans are for property that can be easily moved. They're also an option for borrowers who want their loans approved faster and with shorter repayment times.

Chattel is any tangible personal property that is movable. Examples of chattel are furniture, livestock, bedding, picture frames, and jewelry.