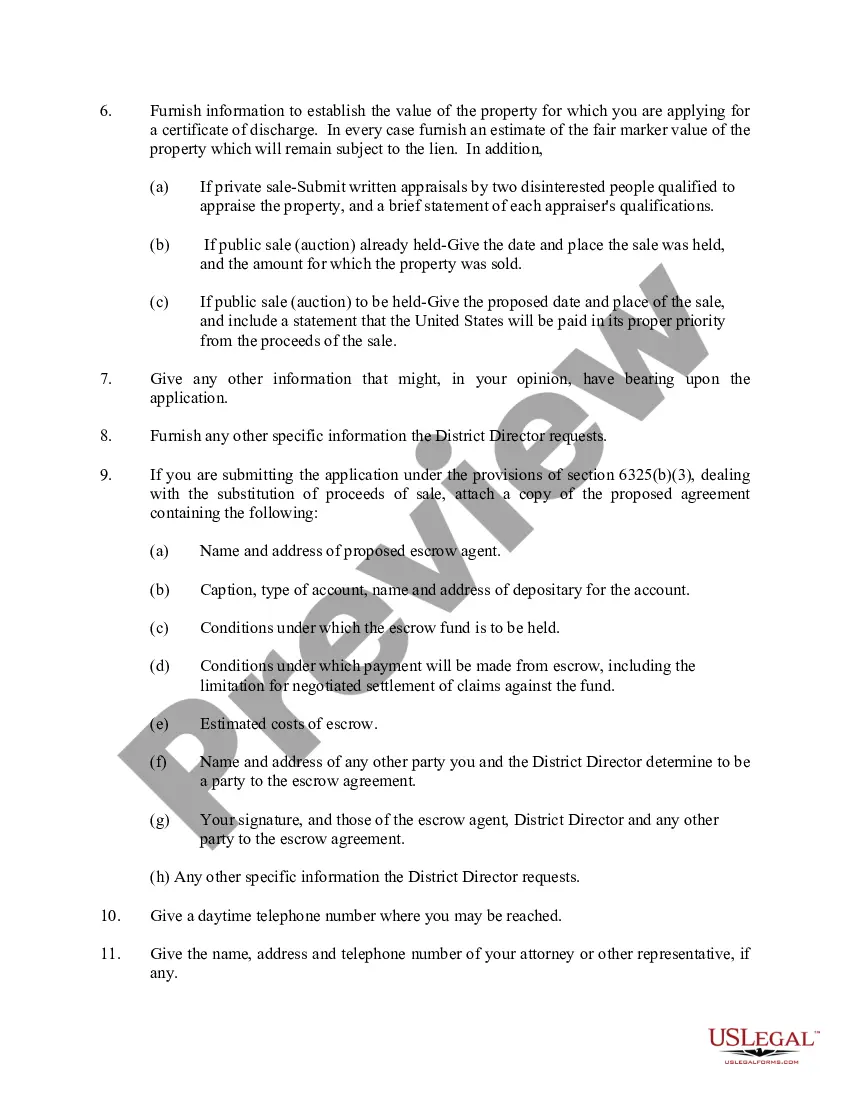

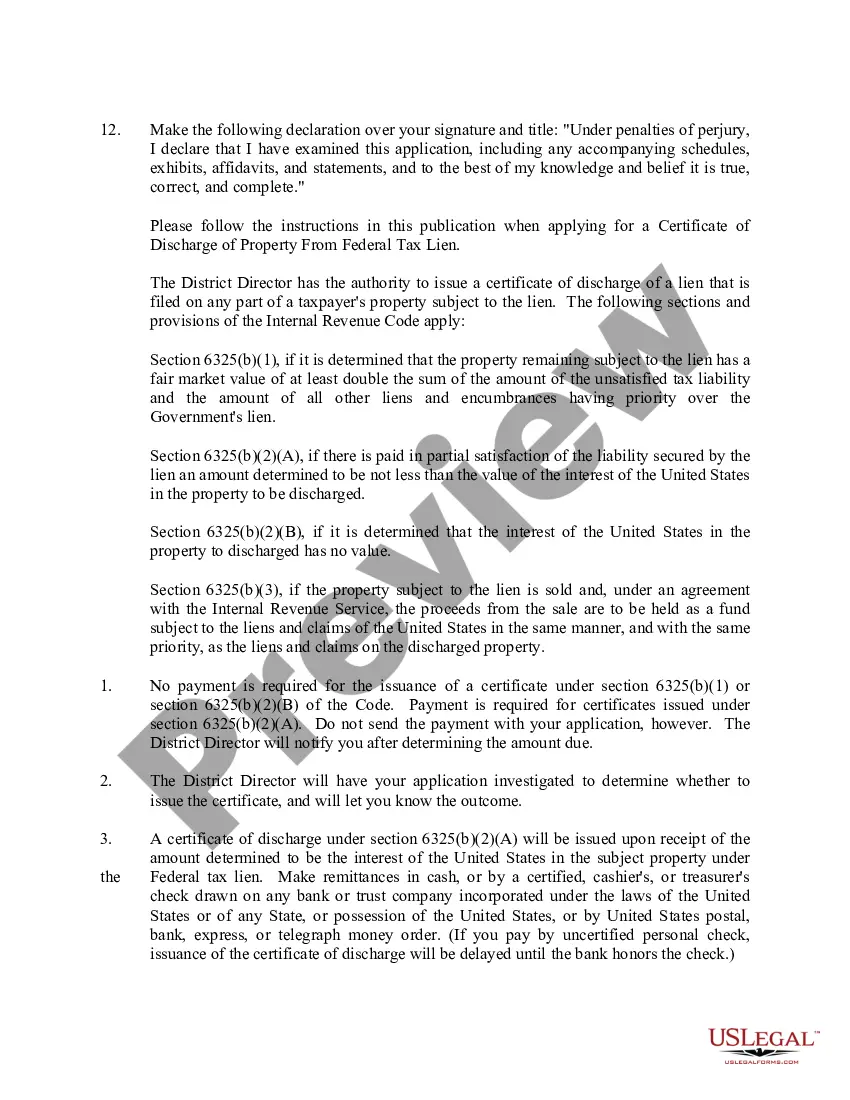

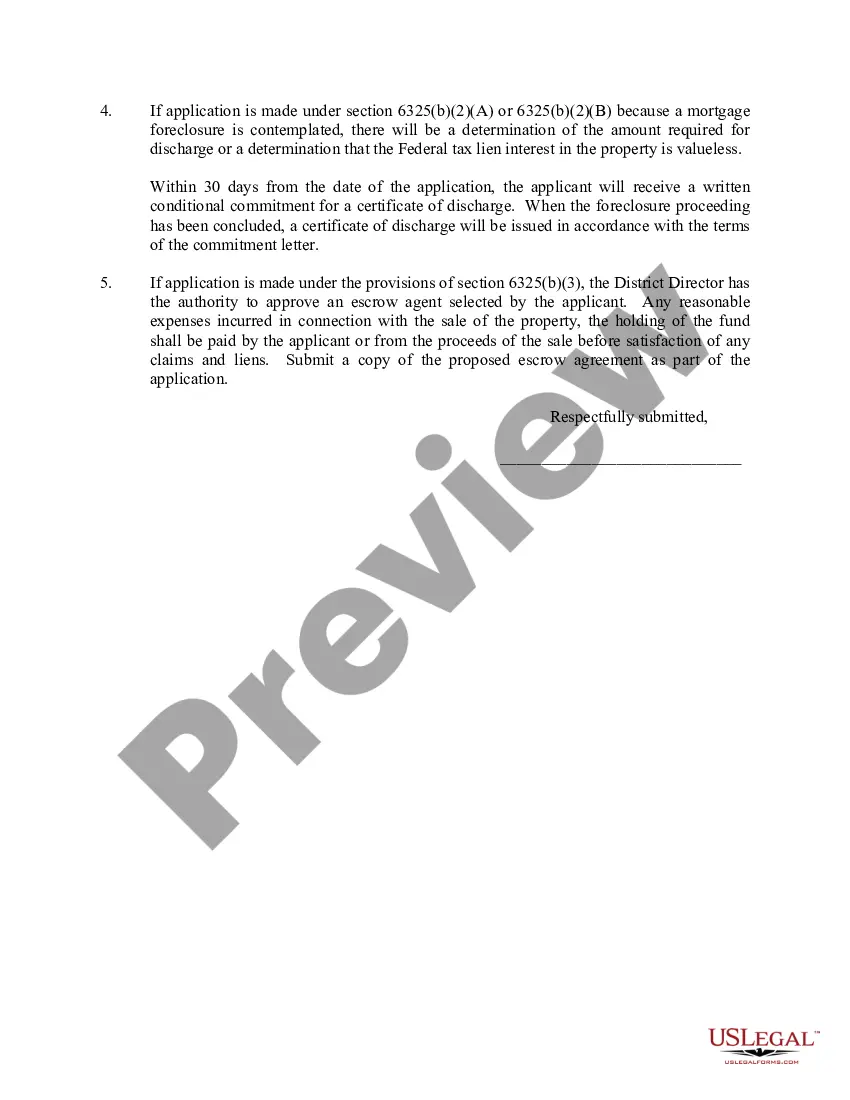

This form is an Application for Certificate of Discharge of IRS Lien. Use to obtain certificate of release when lien has been removed or satisfied. Check for compliance with your specific circumstances.

Publication 783 For 2023 In Cook

Category:

State:

Multi-State

County:

Cook

Control #:

US-00110

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

How to calculate and make estimated tax payments To calculate your estimated taxes, you will add up your total tax liability for the current year—including self-employment tax, individual income tax, and any other taxes—and divide that number by four.

If you were under 65 at the end of 2023 If your filing status is:File a tax return if your gross income is: Single $13,850 or more Head of household $20,800 or more Married filing jointly $27,700 or more (both spouses under 65) $29,200 or more (one spouse under 65) Married filing separately $5 or more1 more row

Report all your estimated tax payments on Form 1040, line 26. Also include any overpayment that you elected to credit from your prior year tax return.

Centralized Lien Operation — To resolve basic and routine lien issues: verify a lien, request lien payoff amount, or release a lien, call 800-913-6050 or e-fax 855-390-3530.

For a copy of the recorded certificate, you must contact the recording office where the Certificate of Release of Federal Tax Lien was filed. If the federal tax lien has not been released within 30 days of satisfying your tax liability, you can request a Certificate of Release of Federal Tax Lien.

Centralized Lien Operation — To resolve basic and routine lien issues: verify a lien, request lien payoff amount, or release a lien, call 800-913-6050 or e-fax 855-390-3530.

The IRS withholding lock-in letter cannot be removed once issued and can only be modified when the employee has shown compliance with the lock-in letter for three years.

A federal tax lien usually releases automatically 10 years after a tax is assessed if the statutory period for collection has not been extended and the IRS does not extend the effect of the Notice of Federal Tax Lien by refiling it.

A federal tax lien is valid for 10 years and 30 days from the date of assessment, unless prior to expiration of this period of limitations, the lien is properly refilled within the time allowed by law.

The standard deduction will increase by $900 for single filers and by $1,800 for joint filers (Table 2). The personal exemption for 2023 remains at $0 (eliminating the personal exemption was part of the Tax Cuts and Jobs Act of 2017 (TCJA).

More info

1. Complete Form 14135, Application for Certificate of Discharge of Federal Tax Lien attached with this publication. IRS Releases Publication 783 (2022), Instructions on How to Apply for Certificate of Discharge from Federal Tax Lien. DEC.Trusted Primary Care Practice serving Brooklyn, Queens, Staten Island, and Glendale, New York. To join the Public Health AmeriCorps program, check out the states below for opportunities with different organizations. This proposed rule would amend the regulations for certain HUD Public and Indian Housing and Housing Programs. The second of the UN's 17 Sustainable Development Goals is to end hunger, achieve food security and improved nutrition and promote sustainable agriculture. 2023 Jun 16;205-533. Tax Analysts has obligations to protect all Tax Notes content. × SFelec,ℎ × FelecHeat).