Consumer Investigative Release Format In Clark

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

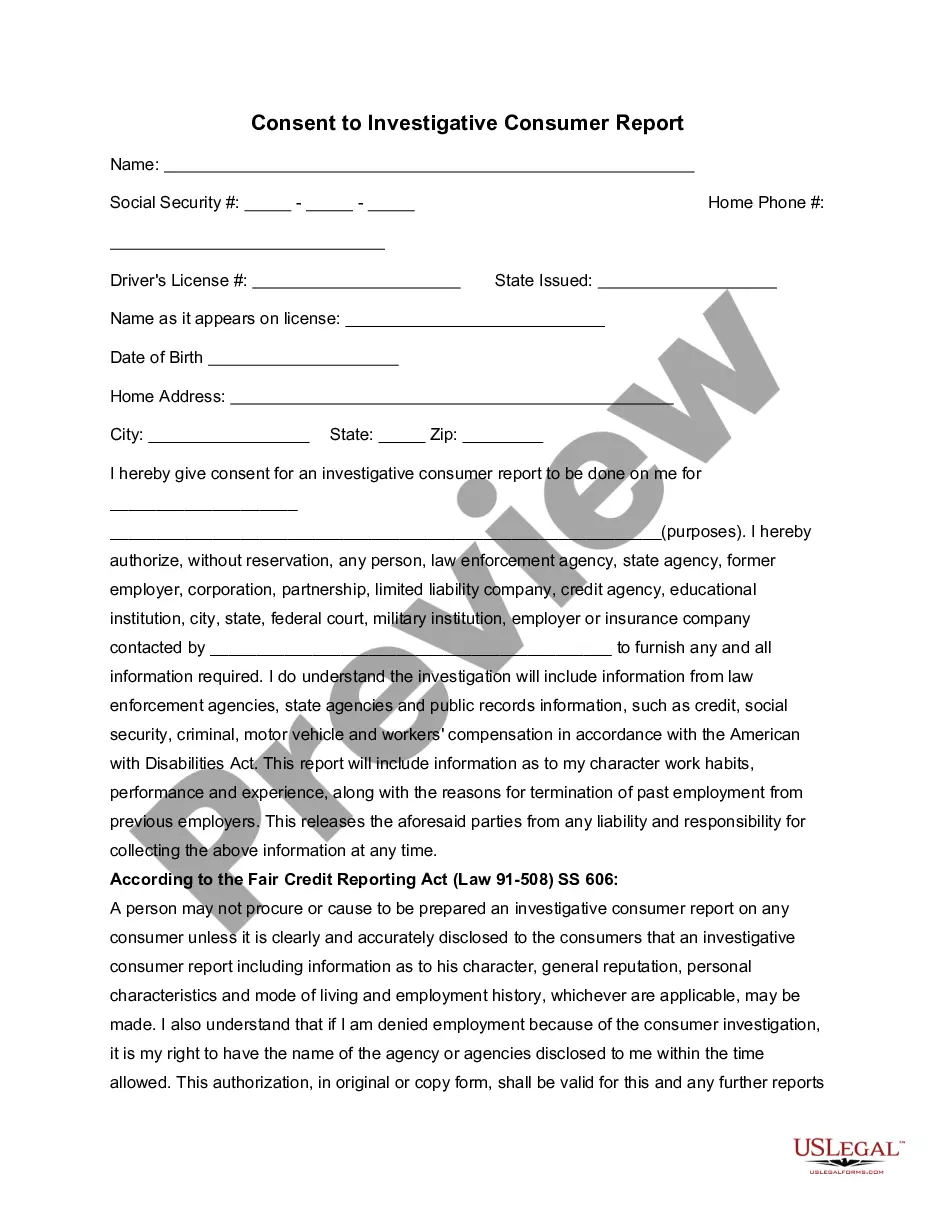

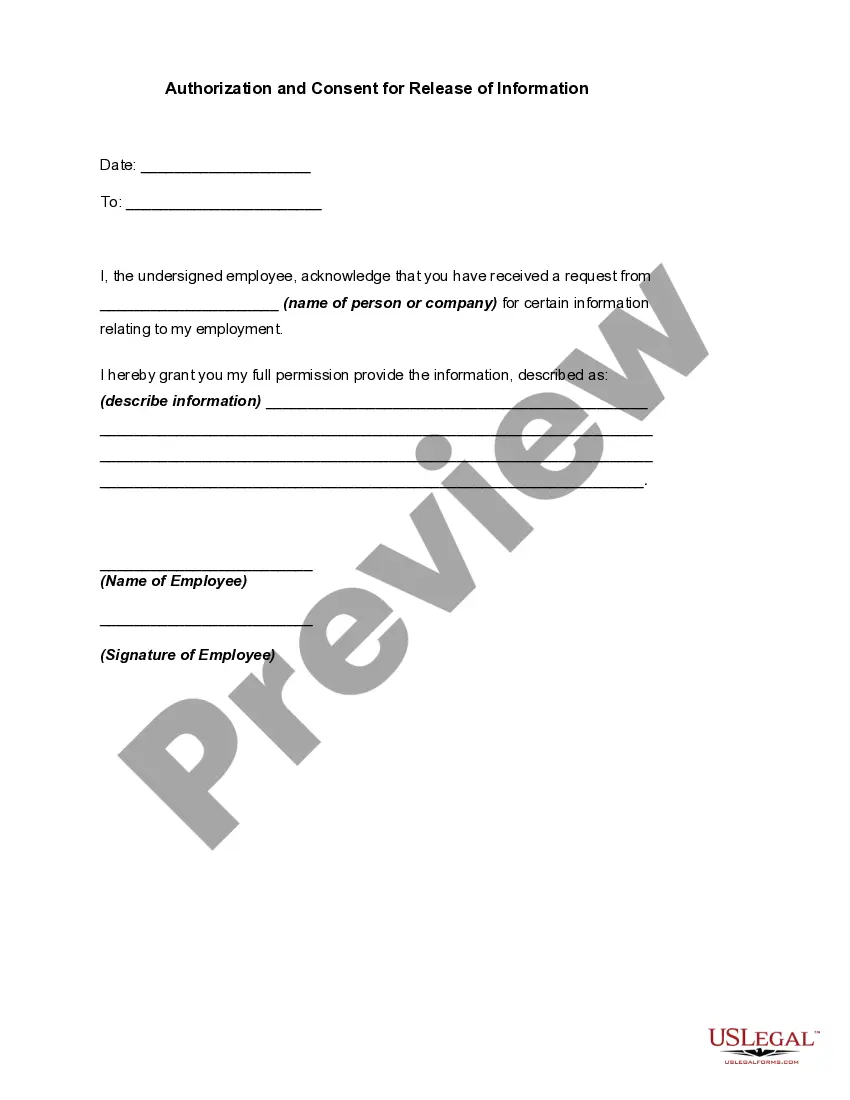

This disclosure shall be made in a writing mailed, or otherwise delivered, to the consumer not later than five days after the date on which the request for such disclosure was received from the consumer or such report was first requested, whichever is the later.

This disclosure shall be made in a writing mailed, or otherwise delivered, to the consumer not later than five days after the date on which the request for such disclosure was received from the consumer or such report was first requested, whichever is the later.

40 Calendar Days – Your insurer must immediately begin its investigation after receiving proof of claim. It must accept or deny your claim within 40 calendar days after receiving proof of claim unless the investigation cannot be completed within that time.

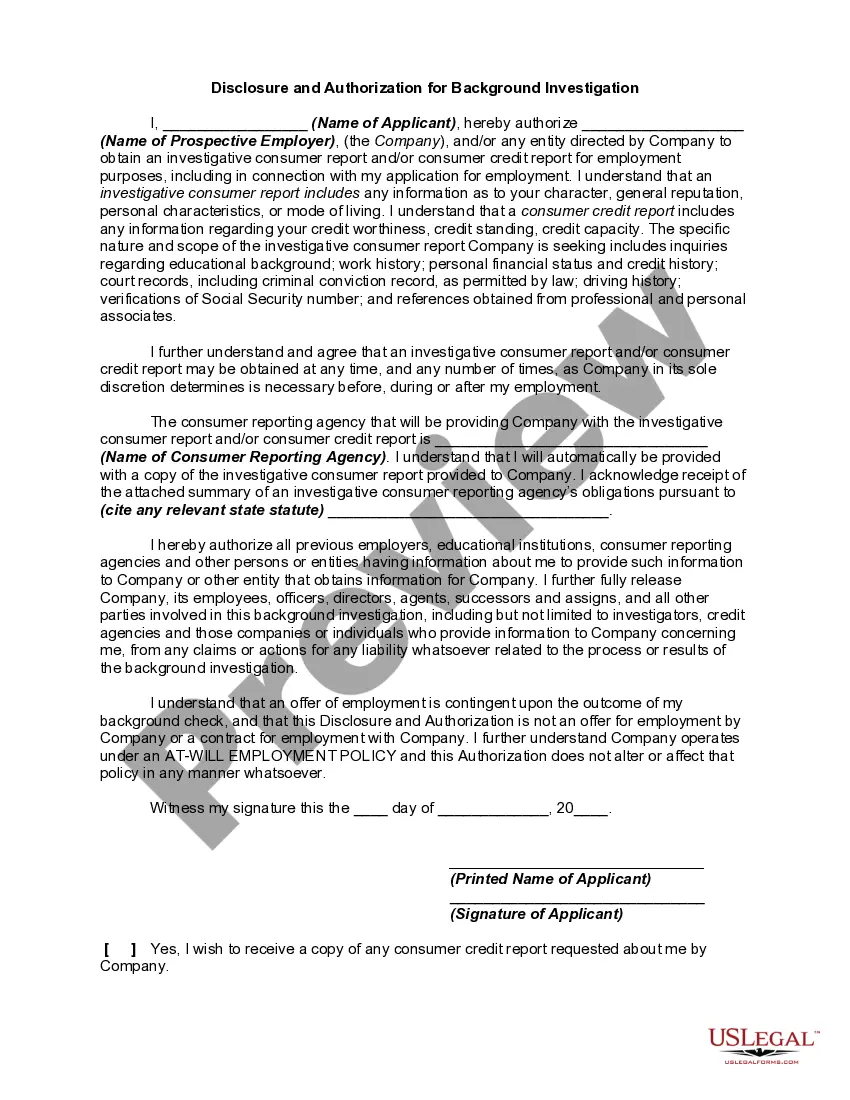

Notification of Investigative Consumer Report ing to federal law, specifically the Fair Credit Reporting Act (FCRA), an insurer must notify a consumer in writing about the acquisition of an investigative consumer report within 3 days of making that request.

These obligations include giving written notice that you may request or have requested an investigative consumer report, and giving a statement that the person has a right to request additional disclosures and a summary of the scope and substance of the report. (See 15 U.S.C.

Section 1681a of the Fair Credit Reporting Act defines an “investigative consumer report” as “a consumer report or portion thereof in which information on a consumer's character, general reputation, personal characteristics, or mode of living is obtained through personal interviews with neighbors, friends, or ...

The bank must identify itself and certify to the reporting agency (consumer reporting agency) the purposes for which the information is sought. It must also certify that the information will be used for no other purpose (16 CFR 607).

Except as otherwise provided in section 1681k of this title, a consumer reporting agency shall not furnish an investigative consumer report that includes information that is a matter of public record and that relates to an arrest, indictment, conviction, civil judicial action, tax lien, or outstanding judgment, unless ...

A consumer reporting agency must also include a summary of consumer rights with the disclosure to the consumer. This ensures the consumer is informed about their rights under the Fair Credit Reporting Act (FCRA). Details such as the firm's name and address, and privacy policies are also typically included.

A consumer report may contain information such as a person's credit characteristics, rental history, or criminal history. These reports are covered by the FCRA.