Meeting Annual Consider Withholding In Wake

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Shareholders who cannot attend the meeting in person are encouraged to vote by proxy, which can be done online or by filling out and mailing a form.

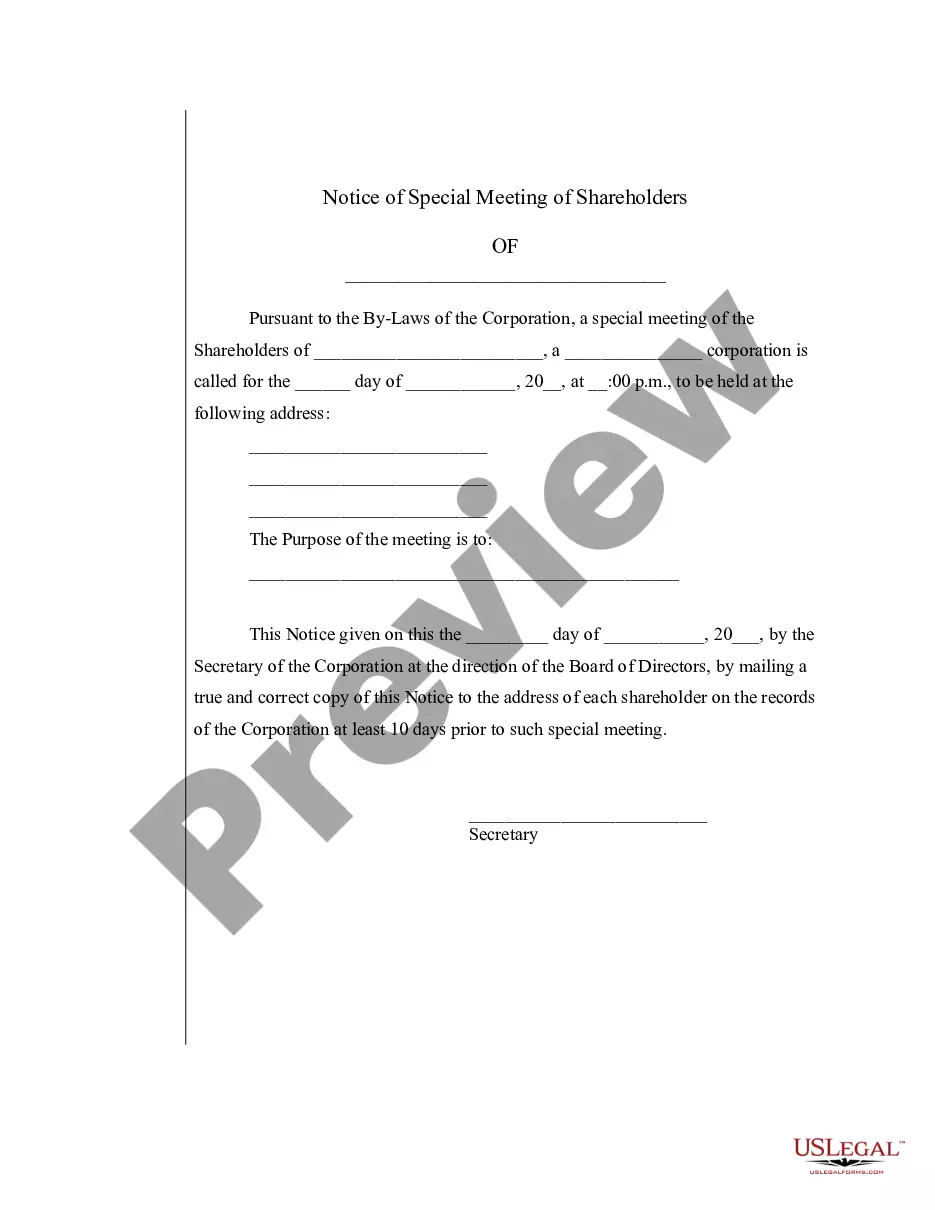

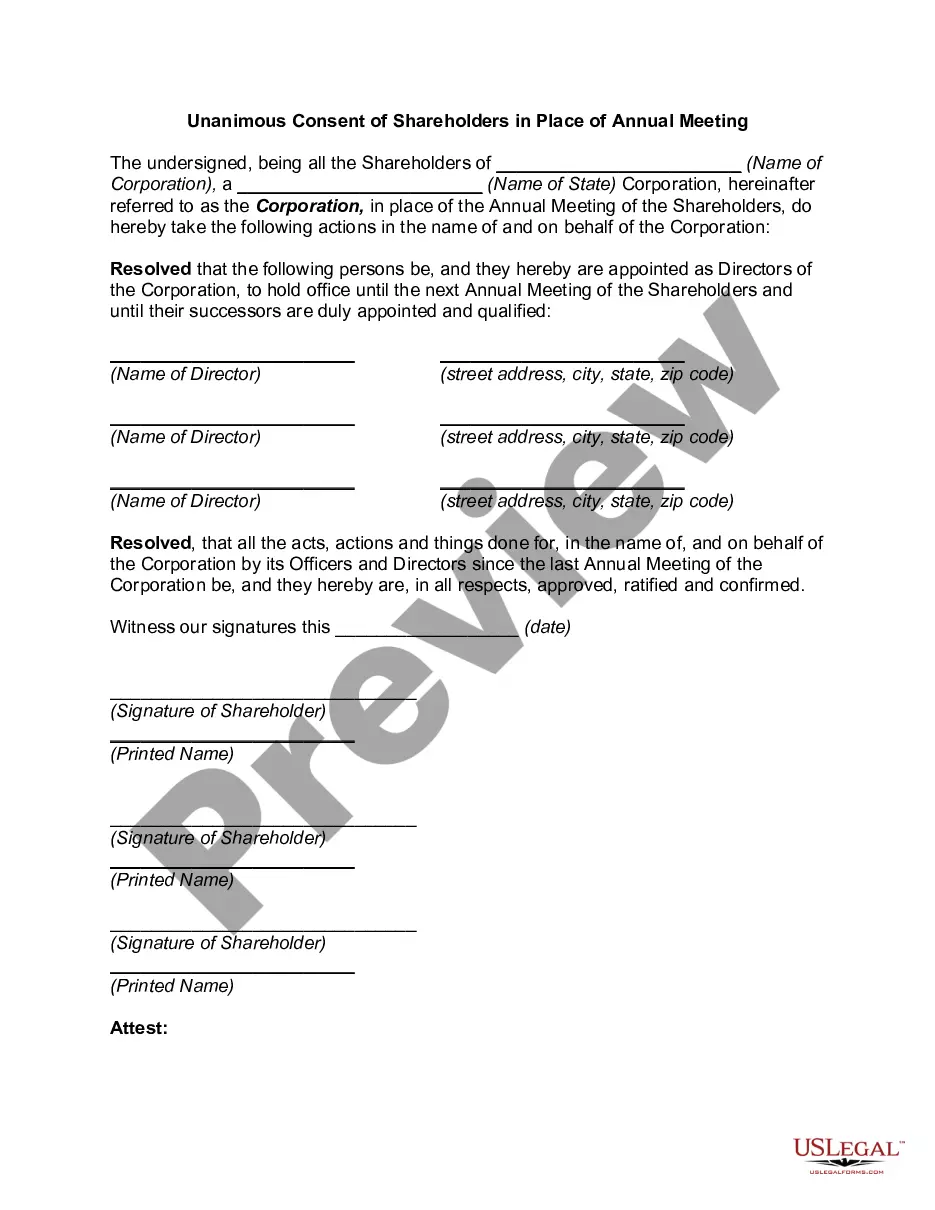

Both California Corporations and California S-Corps are required to hold an annual meeting for shareholders. These meetings are pivotal for fostering transparency, discussing business strategy, and making essential corporate decisions.

Not complying with regulations regarding annual shareholder meetings can put your company, and its owners, at personal risk for liability.

The annual shareholder meeting is usually scheduled shortly after the end of the fiscal year. This timing allows for discussion and review of the previous year's financial performance. Some of the meeting activities may also be necessary for the annual corporate report, which most states require.

Withholding tax payments There are two ways to register. To register online, apply with the Department of Labor on their website. To register by phone, call the Department of Labor at 888-899-8810 or 518-457-4179.

Directors who fail to follow the AGM requirements can be prosecuted in court, and may also face disqualification or debarment from being a director. In addition, ACRA can impose composition fines on companies that do not hold the required AGMs.

If your business is set up and registered as a Corporation, you're required by law to hold an annual shareholder meeting and to document the meeting with minutes.

Withholding tax is a set amount of income tax that an employer withholds from an employee's paycheck. Employers remit withholding taxes directly to the IRS in the employee's name. The tax withholding is a credit against the employee's annual income tax bill.

2 Box 1 ages Safe Harbor Under this method, the monthly premium for selfonly coverage must not exceed 9.02% of the employee's 2 Box 1 wages, which is the employee's gross income minus pretax deductions. The coverage must be affordable for all the months the employee is eligible.

Calculating Estimated Tax Payments – Safe Harbor Method Another way individuals can avoid penalties is by pre-paying a "safe harbor" amount equal to 100% of the previous year's tax. The safe harbor amount for high income taxpayers is paying in 110% of the previous year's tax.