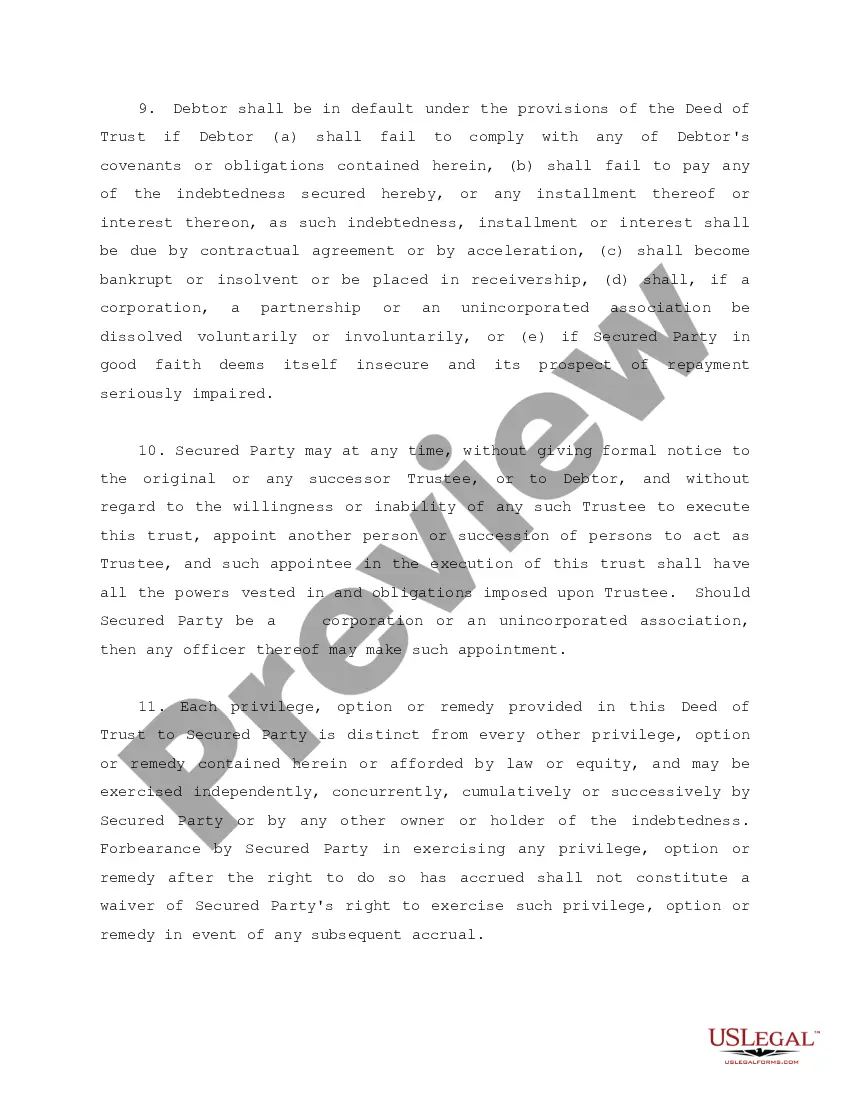

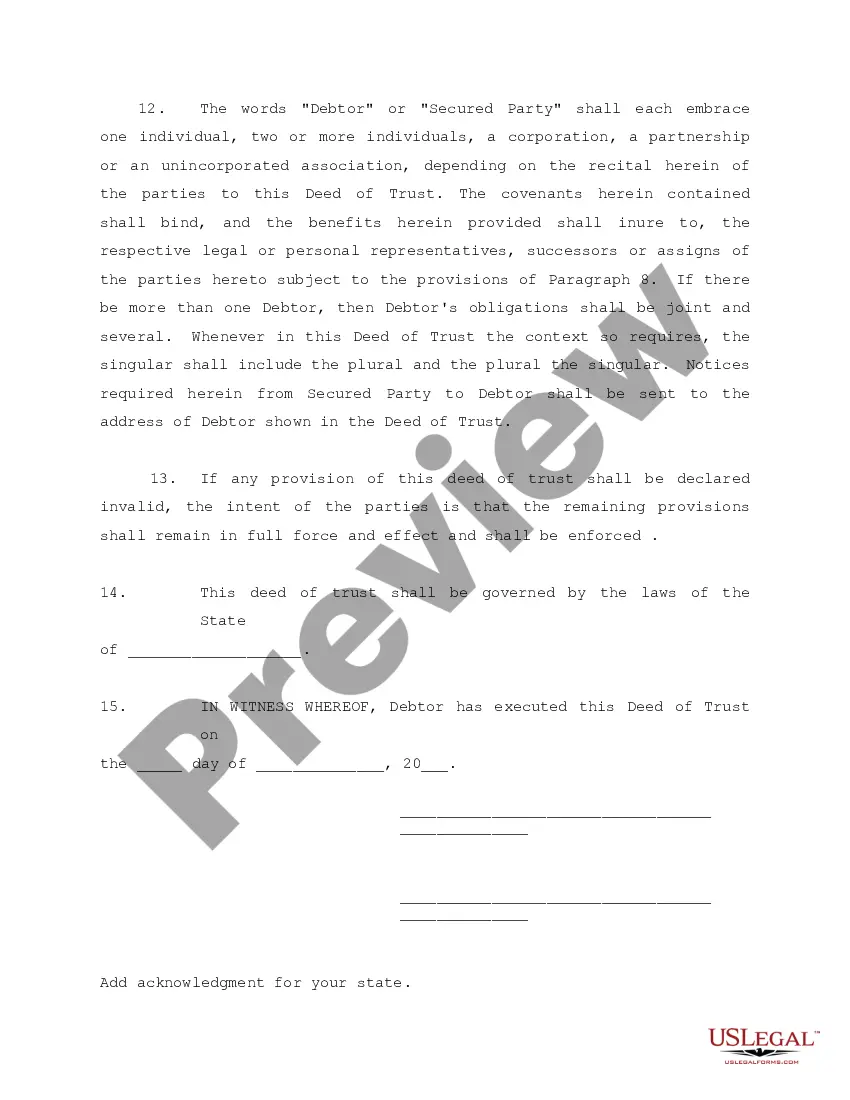

Debtor is obligated to pay the secured party attorneys fees. In consideration of the indebtedness, debtor conveys and warrants to trustee certain property described in the land deed of trust.

Secured Debt Any For Bad Credit In Tarrant

State:

Multi-State

County:

Tarrant

Control #:

US-00181

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Yes it does actually work. Collectors rarely actually validate the debt because most of the debts in fact are not valid. Some just back off because receiving a well worded debt validation letter means you have consulted the FDCPA (or at least a good debt/credit forum) and know what you're doing.

If you get an unexpected call from a debt collector, here are several things you should never tell them: Don't Admit the Debt. Even if you think you recognize the debt, don't say anything. Don't provide bank account information or other personal information. Document any agreements you reach with the debt collector.

Once you dispute the debt, the debt collector must stop all debt collection activities until it provides you with proof that you actually owe the debt. If the debt collector can't provide you with that proof, it will never bother you again.

Federal law requires collection agencies to provide debt validation notices, so you don't need to request one. In some cases, a collector may provide the validation letter as its initial communication to you. If not, they must provide it within five days of their first communication, either in the mail or via email.

You have three options: deny, admit, or deny for lack of knowledge. As a rule of thumb, lawyers advise you to deny, deny, deny. Let the plaintiff prove your responsibility for the debt. Include your affirmative defenses: These are reasons why you think the plaintiff is wrong to sue you.

Its called a verification of debt letter. write to them and ask for verification of debt (preferably itemized). send it by certified mail with return receipt (where they attach a little postcard to the back and stamp it when it gets delivered). they have 30 days to reply with proof.

A writ of garnishment allows a creditor to seize property from a debtor that is being held by a third party. While some property is exempt from garnishment in Texas, such as wages, other property such as bank accounts and stocks may be subject to garnishment.

Texas law gives someone 4 years to bring a lawsuit for unpaid debt. This time period is commonly referred to as the statute of limitations. Once the time period is up, a person is prohibited from filing suit to recover the debt. This means the debt is time-barred.

Common consumer debts like credit cards, medical bills, and personal loans typically cannot result in wage garnishment in Texas. However, exceptions include unpaid taxes, child support, alimony, federal student loans, and defaulted federal loans.

Common consumer debts like credit cards, medical bills, and personal loans typically cannot result in wage garnishment in Texas. However, exceptions include unpaid taxes, child support, alimony, federal student loans, and defaulted federal loans.

More info

To meet the needs of every borrower, TCCU offers a range of personal loans, both secured and unsecured to meet your lending needs. The secure online auto credit application is short, easy to complete in just a very few minutes.At Greater Texas Credit Union, we offer unsecured loans (loans without collateral) at great rates to our great members. Loans are available for both students and parents. Fill out our initial bankruptcy questionnaire and we will get back to you regarding your case. For any questions or concerns please call . Apply for a Fort Worth property tax loan! Low Fixed Rates, No Credit Check. Debt Claims This form must be completed and submitted when an original petition is filed in justice court. Many forms for debt claim cases in Texas in Spanish.