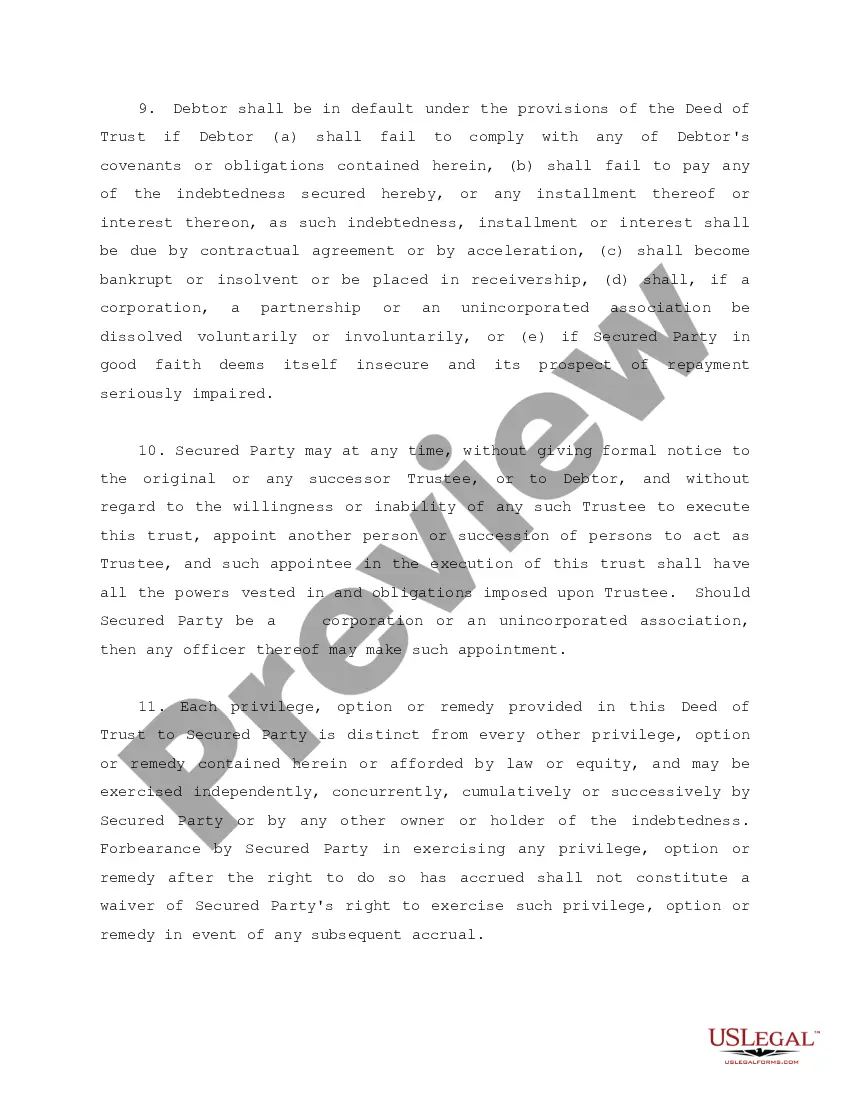

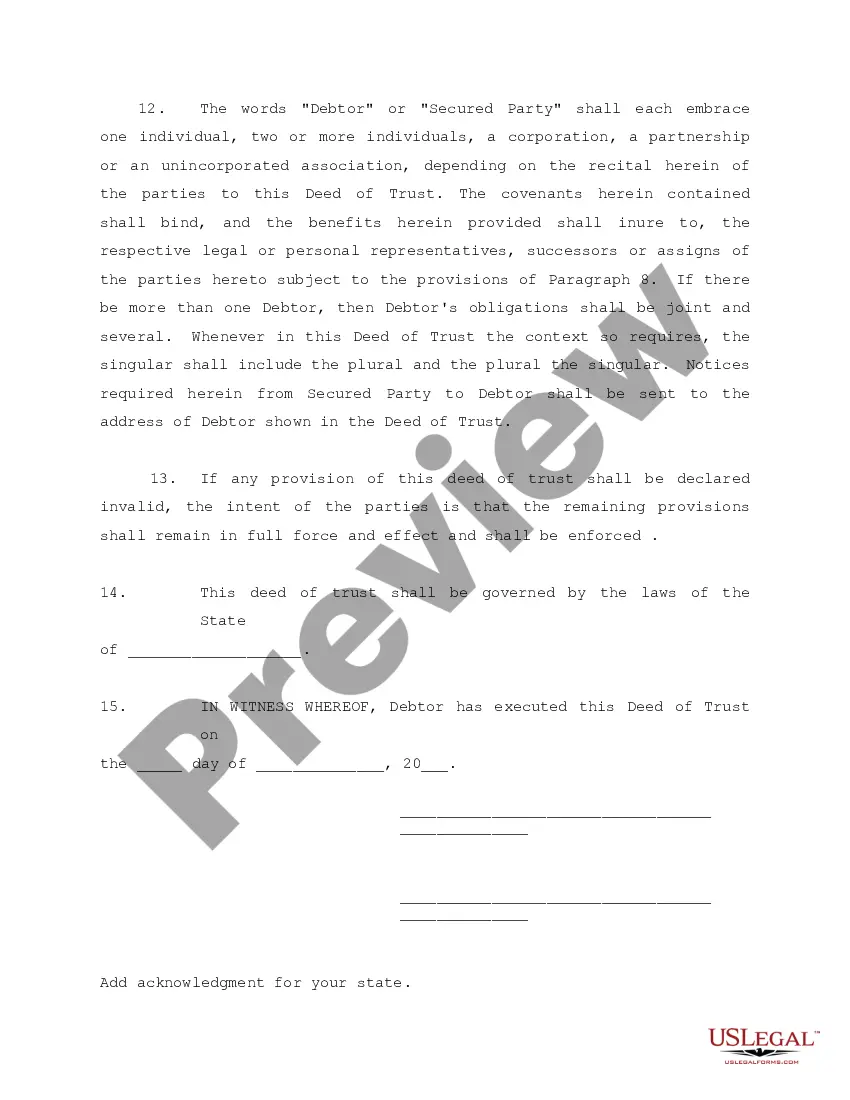

Debtor is obligated to pay the secured party attorneys fees. In consideration of the indebtedness, debtor conveys and warrants to trustee certain property described in the land deed of trust.

Secured Debt Any With A Sinking Fund In Utah

State:

Multi-State

Control #:

US-00181

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Sinking funds are in 'trust' for the scheme and should not be returned to lessees upon assignment, or at any time. Interest earned on funds should be added to the funds unless the lease states otherwise. If funds are held in 'trust' then a tax will be charged on the interest earned.

Sinking fund payments are usually made to a trust company or sinking fund trustee and are just as binding on the issuer as interest payments, e.g., failure to make sinking fund payments entitles the bondholders to the same legal rights as default in payments of interest.

Disadvantages of Sinking Funds Limited Flexibility. Funds set aside in a sinking fund are typically not accessible for other purposes, limiting financial flexibility. Potential Shortfall.

Sinking funds are in 'trust' for the scheme and should not be returned to lessees upon assignment, or at any time. Interest earned on funds should be added to the funds unless the lease states otherwise. If funds are held in 'trust' then a tax will be charged on the interest earned.

An independent trustee will invest the corporation's annual deposits with the goal of the sinking fund balance growing to approximately $20 million by the time the bonds come due in 20 years. The corporation will report the bond sinking fund balance in the investments section of its balance sheet.

Answer and Explanation: A bond sinking fund would be categorized as an investment on the balance sheet. These are long-term assets.

Example of Reporting a Sinking Fund on the Balance Sheet A corporation's bond sinking fund appears in the first noncurrent asset section of the corporation's balance sheet. This section is likely to have the heading Investments.

A sinking fund is typically listed as a noncurrent asset—or long-term asset—on a company's balance sheet and is often included in the listing for long-term investments or other investments.

A sinking fund is typically listed as a noncurrent asset—or long-term asset—on a company's balance sheet and is often included in the listing for long-term investments or other investments. Companies that are capital-intensive usually issue long-term bonds to fund purchases of new plant and equipment.

More info

All income from the investment of sinking fund money shall be deposited to that sinking fund and used for the payment of debt service on the refunding bonds. There is created a special revenue fund within the County of the First Class Highway Projects Fund entitled "2010 Salt Lake County Revenue Bond Sinking Fund."Sinking Fund Installment" means the amount of money which is required to be deposited into the Sinking Fund Account in each Bond Fund Year as specified in the. (iv) All remaining funds, if any, in the Sinking Fund after all of the payments required to be made into the Bond Fund and Reserve. Provides technical assistance and debt issuance in formation to public agencies, as well as to all sec tors of the municipal finance industry. The notes may not be redeemed prior to maturity and there will not be any sinking fund. The amount of sinking fund and how invested. Many debts can be discharged - or wiped away - in a bankruptcy proceeding. The debtor is no longer legally obligated to repay any debt that has been discharged.