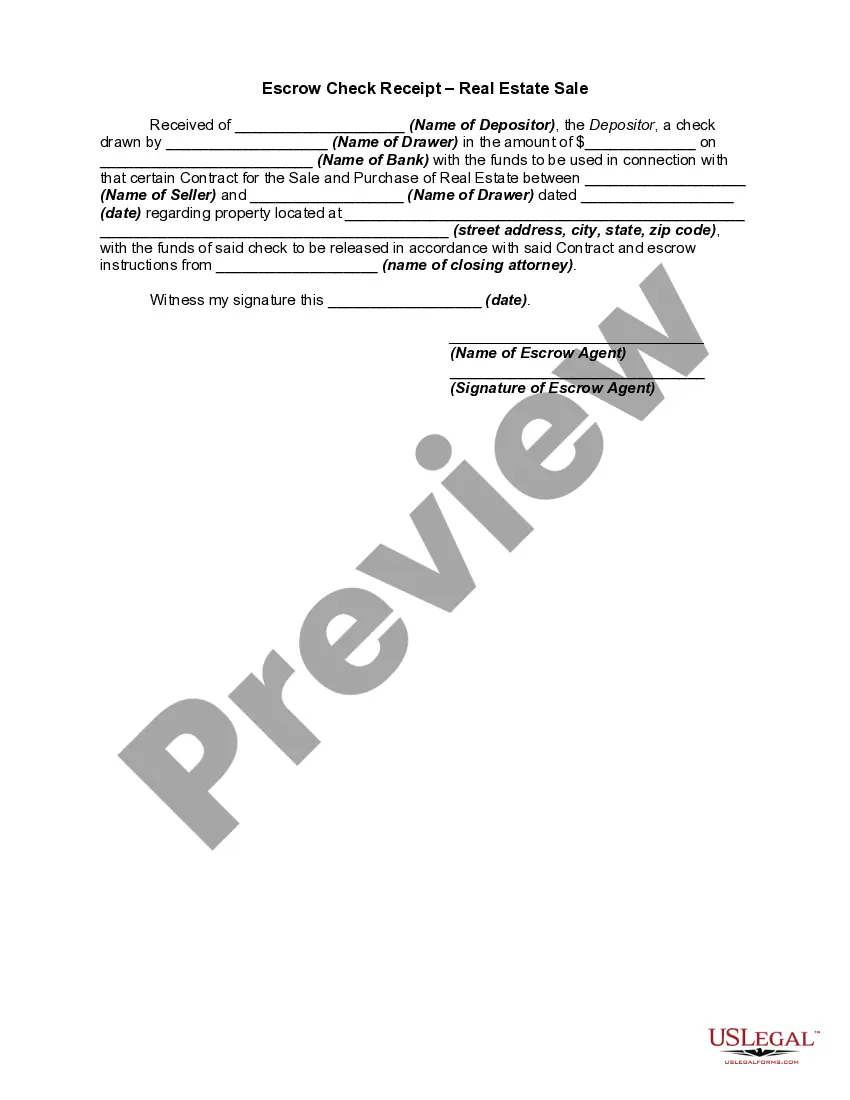

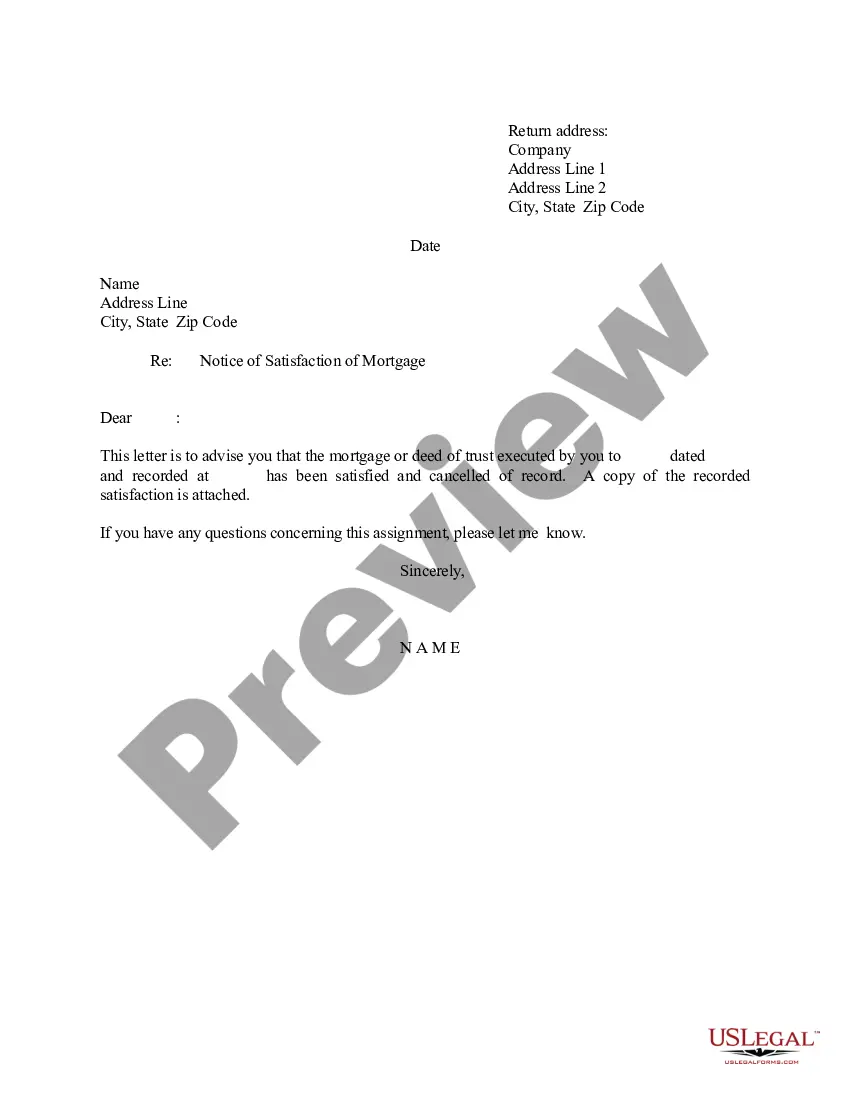

Escrow Seller Does For Home Insurance In Wayne

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Switching home insurance companies when you have an escrow account. Inform your mortgage lender: Let your mortgage company know that you're planning to switch home insurance companies. They'll need to update your escrow account with your new insurance information.

Who Does The Escrow Agent Work For? Escrow agents act as neutral third parties in these types of transactions. They serve the escrow agreement, and as such, they don't work for either the buyer or the seller.

You can easily change insurance companies. Get quotes from several agents, showing them your current coverage and telling them you want similar or better coverage. Or, visit with an independent insurance agent who can do a lot of the footwork for you.

Steps to change homeowners insurance providers Review your current policy. Determine your policy needs. Research different providers and get quotes. Confirm the mortgage clause for your lender. Buy your new policy. Cancel your existing policy. Contact your lender. Send your premium refunds to the new escrow account.

Inform your mortgage company of your insurance change so they can direct homeowners insurance payments from your escrow account to the correct insurer. Simply send a copy of your homeowners insurance declarations page and your former policy's cancellation notice to your lender.

The funds stay in the escrow account until the sale closing unless the transaction falls through. In that case, the funds are kept by the seller or returned to the buyer depending on the reason the contract isn't completed.

Homeowners insurance policies do not automatically cancel when a house is sold. The responsibility lies with the policyholder (the seller, in this case) to inform the insurance company about the sale of the house and request cancellation or transfer of the policy, depending on the circumstances.

No, it's not a good thing. Having taxes and insurance in escrow provides financial security and prevents surprise expenses. It's a common practice for mortgage lenders and can help you budget effectively. If it's not in escrow, you should consider setting up your own system to ensure you're covered.

The home you sell is considered yours until the closing process is finalized. At closing, once the buyer officially owns the home, you can cancel your coverage. Until that time, your homeowners insurance policy should remain in place to provide protection should anything happen to the home.