Loan Payoff Letter Format For Audit In San Antonio

Description

Form popularity

FAQ

We're all familiar with the basic concept of setup and payoffs: early on in your screenplay, you set up some detail/scenario that may seem irrelevant, but later on will yield a result that hopefully your audience wasn't anticipating (the payoff).

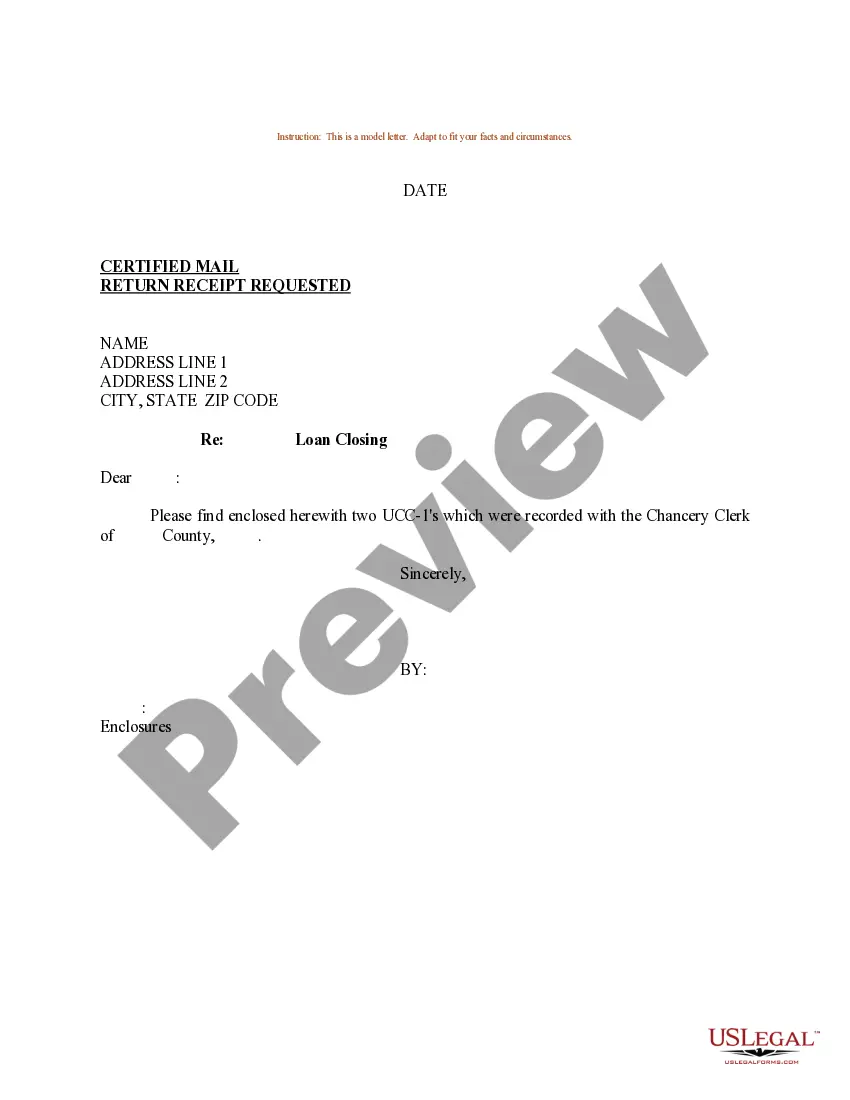

1 filing is good for five years. After five years, it is considered lapsed and no longer valid. Should your debtor remain in debt to you and encounter financial difficulty or file for bankruptcy, you have no secured interest if your UCC1 filing has lapsed.

The Texas Uniform Commercial Code may be a good alternative for consumers who have a lemon law related claim in Texas. The Texas “UCC” is beneficial in that the statute of limitation (the time period for which the consumer must file suit) is four years.

All UCC's that are filed with the County Clerk are valid for (5) years. Any statement that expires may be continued with the Secretary of State. If the statement remains effective past July 01, 2002, a new UCC will need to be filed. Please direct any questions to the Texas Secretary of State.

Visit your secretary of state's office To do so you will generally need to make a trip in person down to your secretary of state's office. Once there, you will be able to swear under oath that you've satisfied the debt in full and wish to request for the UCC-1 filing to be removed.

Visit your secretary of state's office To do so you will generally need to make a trip in person down to your secretary of state's office. Once there, you will be able to swear under oath that you've satisfied the debt in full and wish to request for the UCC-1 filing to be removed.

To get a payoff letter, ask your lender for an official payoff statement. Call or write to customer service or make the request online. While logged into your account, look for options to request or calculate a payoff amount, and provide details such as your desired payoff date.

The statement is provided by the mortgage servicer and can be requested at any time. Accurate payoff information is crucial for managing financial decisions related to property ownership.

The number you see on your mortgage statement is the principal balance, not the payoff amount. The payoff amount showing on the settlement statement takes into account the principal balance plus interest accrued for the number of days between the statement and a few days after the closing.