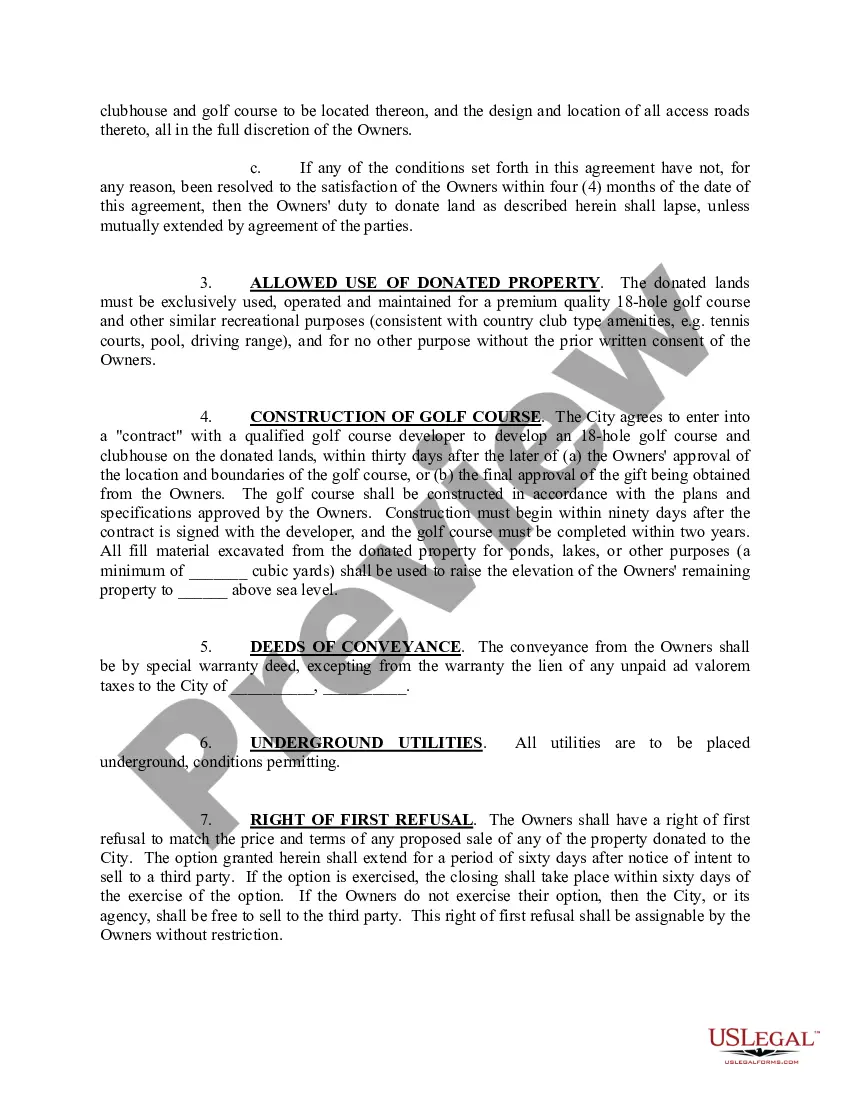

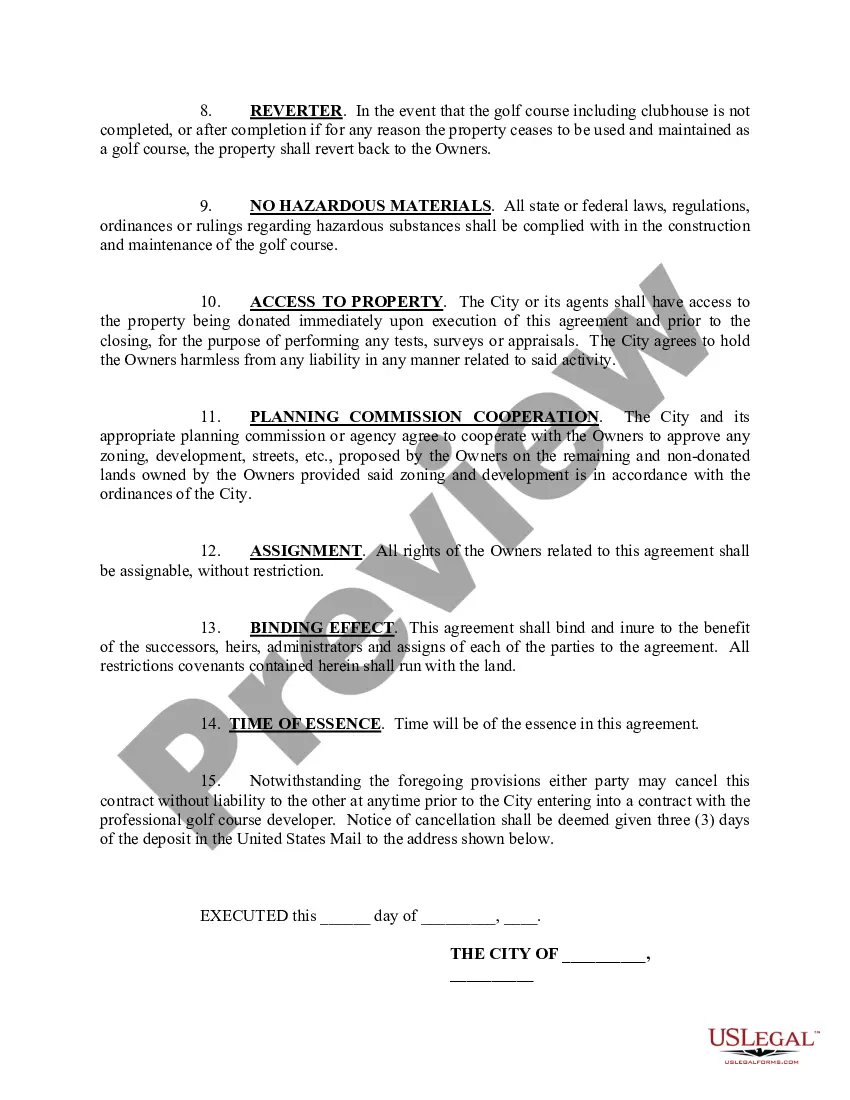

Wisconsin Agreement To Donate Real Estate To City Without Mortgage In Fairfax

Description

Form popularity

FAQ

Yes, it is entirely permissible to donate real estate to private foundations. However, such donations come with potential drawbacks that make them less common compared to donations to public charities.

A deed and an Electronic Wisconsin Real Estate Transfer Return (eRETR) must be completed to convey title to real estate. If you need additional information in regards to your inquiry you will have to consult with a title company or an attorney. You can also contact the Register of Deeds at (608) 266-4141.

Generally, land trusts will prevent real estate transfer taxes in states where transfer taxes apply. The reason is simple. For real estate transfer taxes, most states have an exemption for grantor trusts wherein the beneficiary is the same as the grantor.

A. Donated fixed assets shall be accounted for at the estimated fair market value on the date of acquisition.

Determining the value of donated property de- pends upon many factors. You should consider all the facts and circumstances connected with the property, including any recent transactions, in determining value. Value may also be based on desirability, use, condition, scarcity, and mar- ket demand for that property.

The company can record the donated asset by: Debiting a fixed asset account (at fair market value), and. Crediting contribution revenue.

The contributions must be made to a qualified organization and not set aside for use by a specific person. If you give property to a qualified organization, you can generally deduct the fair market value (FMV) of the property at the time of the contribution.

In short, the U.S. government expects foundations to use their assets to benefit society and it enforces this through section 4942 of the Internal Revenue Code, which requires private foundations to distribute 5% of the fair market value of their endowment each year for charitable purposes.

Real estate held for charitable purposes may be exempt from property tax, and the foundation may attain tax benefits by virtue of holding property utilized for charitable purposes.