Corporate Resolution For Sole Owner In Houston

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Voting Resolutions: Voting resolutions are used to make important decisions in the LLC. Voting resolutions require the approval of a certain number of members for the resolution to pass. Consent Resolutions: Consent resolutions are used when all members of the LLC agree to a certain action or decision.

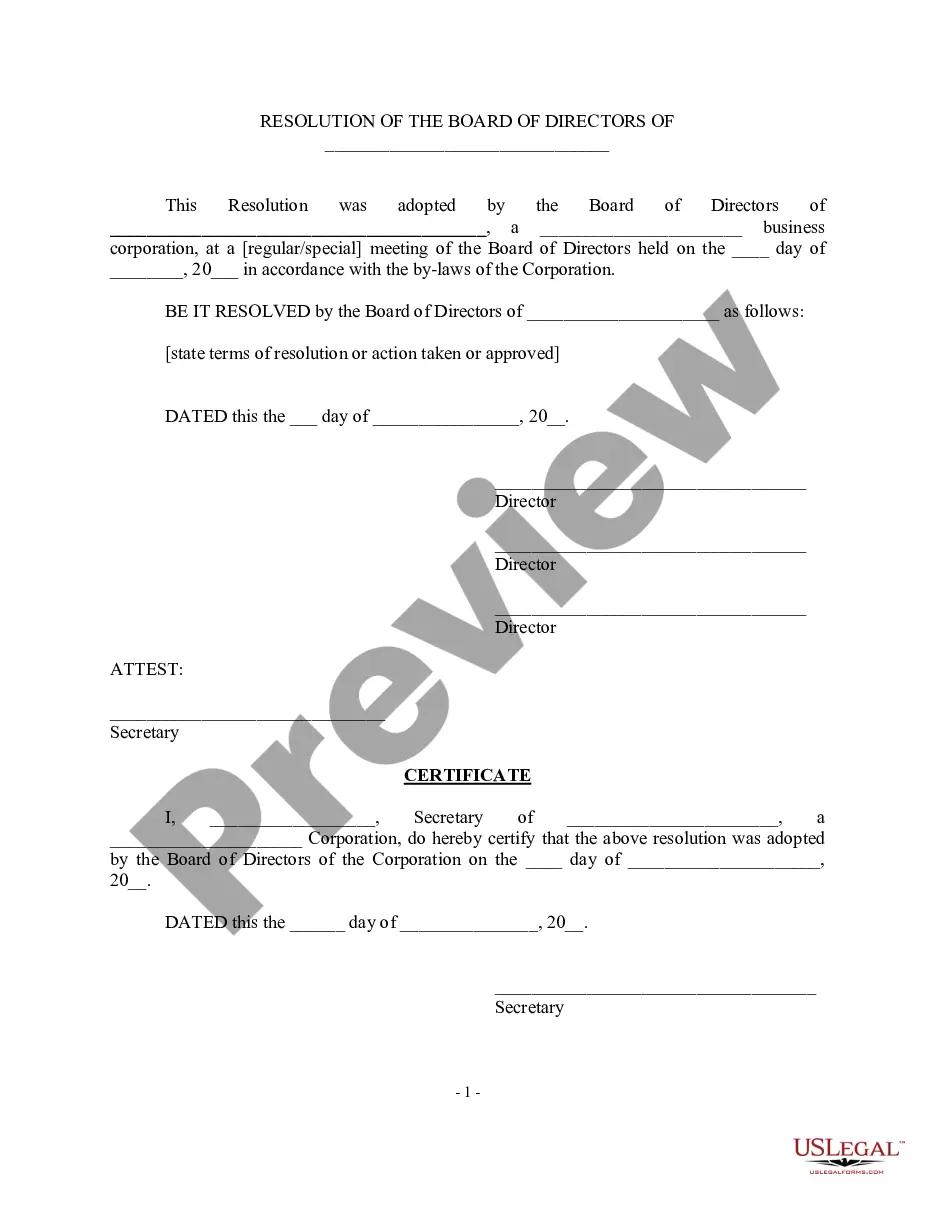

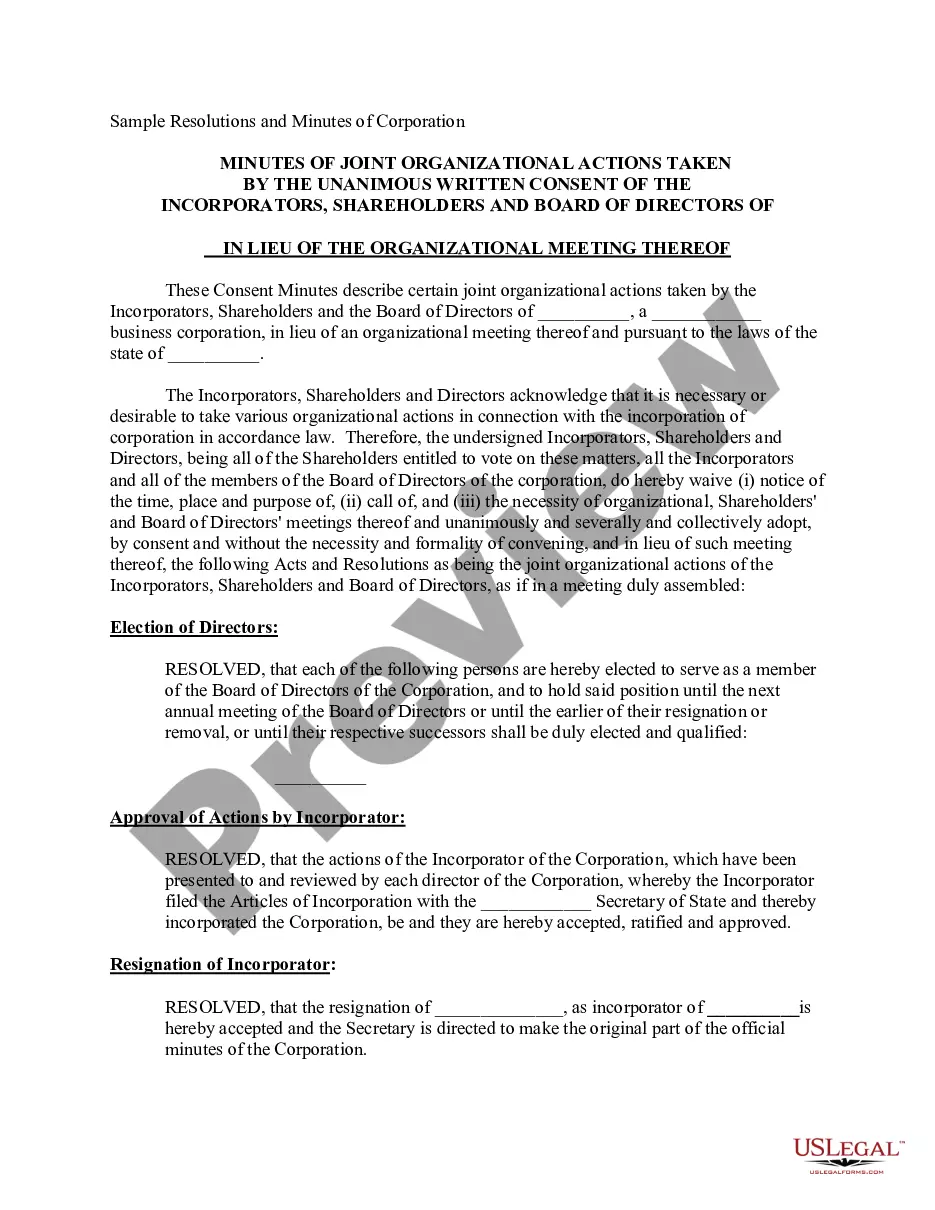

A corporate resolution is a written document created by the board of directors of a company detailing a binding corporate action. A board of directors is a group of people that act as a governing body on behalf of the shareholders of a company.

Typically, a board of directors will create corporate resolutions and sign them at a board meeting. Before the meeting, all board members should receive a meeting agenda that includes any decisions or actions to be resolved. Resolutions must follow a format approved by the state where the business is registered.

A corporate resolution generally involves major decisions such as the changing of ownership structure, voting in of new board members, or the sale of company shares. A corporate resolution is also generally used to authorize people to access corporate funds, sign checks and acquire loans on behalf of the corporation.

Single-member LLCs do not need resolutions, but they can still come in handy in certain situations, like if the company must defend itself in court. Documenting changes or actions not covered in the original bylaws or articles of incorporation can help an LLC protect itself from lawsuits or judicial investigations.

Typically, corporations require these documents when an agreement between the owners and the board may enable business transactions and decisions.

Single-member LLCs do not need resolutions, but they can still come in handy in certain situations, like if the company must defend itself in court. Documenting changes or actions not covered in the original bylaws or articles of incorporation can help an LLC protect itself from lawsuits or judicial investigations.

A sole proprietorship is a non-registered, unincorporated business run solely by one individual proprietor with no distinction between the business and the owner. The owner of a sole proprietorship is entitled to all profits but is also responsible for the business's debts, losses, and liabilities.

Unlike a corporation or LLC, a sole proprietorship is not a legal entity separate from its owner. Instead, the proprietor personally owns all the business assets. Thus, a sole proprietorship has no continuity of life. It automatically terminates by law upon the sole proprietor's death or disability.