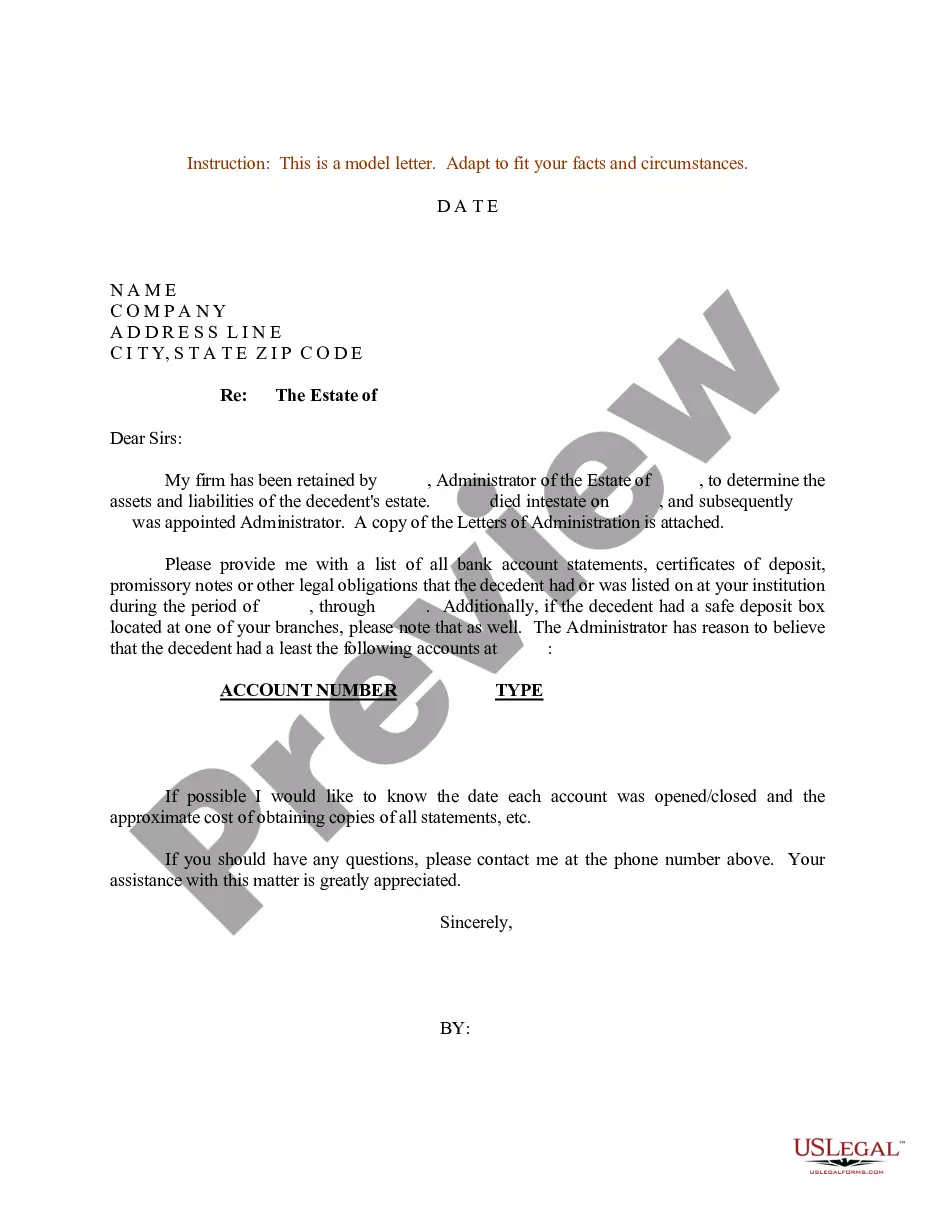

Letter Of Instruction To Bank After Death With Trust In Bexar

Description

Form popularity

FAQ

Bank Accounts Held in Trust After your death, when the person you chose to be your successor trustee takes over, the funds will be transferred to the beneficiary you named in your trust document. No probate will be necessary. To transfer the account to your trust, tell the bank what you want to do.

Also known as a letter of intent, a letter of instruction is specifically designed to express the deceased's final wishes—everything from how the estate plan should be carried out to the location of important documents and guidance for loved ones.

The bank is likely to ask for two forms of your identification (usually a passport or driver's licence, or a proof of address with a utility bill) and a copy of the will. If there's no will, the bank could ask for evidence of your relationship to the deceased. You'll also need the death certificate.

The bank needs to be notified of the accountholder's passing as soon as possible, as any bank accounts of the deceased remain active until the bank is notified of the death. This typically entails providing the original Death Certificate for verification purposes and the Will, if one is available.

The next of kin must notify their banks of the death when an account holder dies. This is usually done by delivering a certified copy of the death certificate to the bank, along with the deceased's name and Social Security number, bank account numbers, and other information.

“In trust for” (ITF) and “payable on death” (POD) are two designations that you can use to pass on bank accounts or other financial accounts after you're gone. The main difference between in trust for vs. payable on death is that the former has a trustee while the latter does not.

Steps to Closing Out a Trust After Death Step 1: Notify Beneficiaries and Creditors. The first task for the successor trustee is to notify both the beneficiaries and creditors. Step 2: Inventory and Value Assets. Step 3: Settle Debts and Taxes. Step 4: Distribute Assets to Beneficiaries. Step 5: Dissolve the Trust.

A payable on death (POD) designation means your bank account automatically transfers to a beneficiary upon the death of all account owners and co-owners. Setting up a POD beneficiary allows you to plan for the future and make your financial wishes clear.

The main drawback of a POD account is that it is not possible to name alternate beneficiaries to your account. If the person whom you nominated to receive the proceeds dies before you, then the contents of your account are automatically transferred to an estate or will.