This form is a sample letter in Word format covering the subject matter of the title of the form.

Letter Of Instruction To Bank After Death For Funeral In Nevada

Category:

State:

Multi-State

Control #:

US-0034LTR

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

What Not to Do When Someone Dies: 10 Common Mistakes Not Obtaining Multiple Copies of the Death Certificate. 2- Delaying Notification of Death. 3- Not Knowing About a Preplan for Funeral Expenses. 4- Not Understanding the Crucial Role a Funeral Director Plays. 5- Letting Others Pressure You Into Bad Decisions.

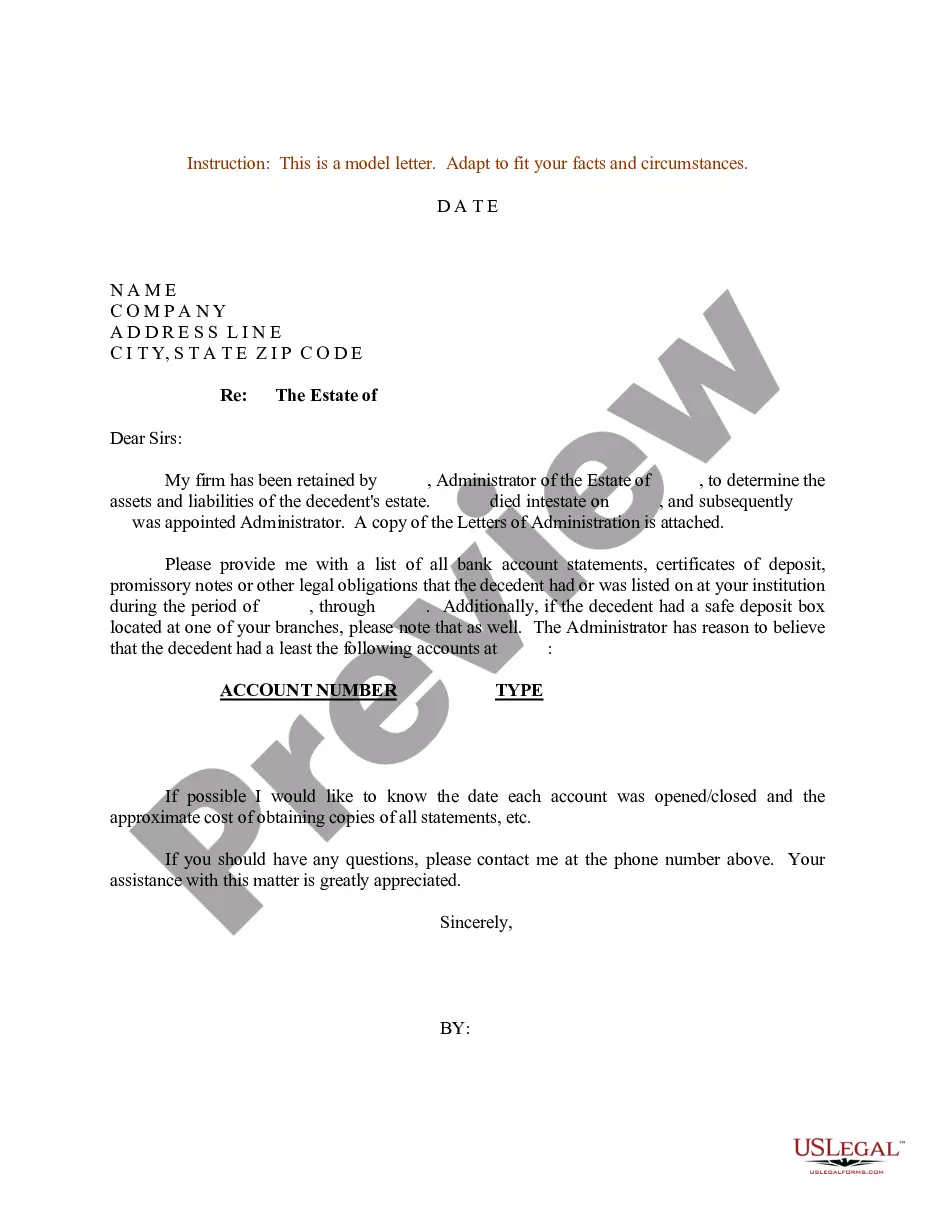

The bank is likely to ask for two forms of your identification (usually a passport or driver's licence, or a proof of address with a utility bill) and a copy of the will. If there's no will, the bank could ask for evidence of your relationship to the deceased. You'll also need the death certificate.

Your valid ID, such as a state-issued driver's license or ID card, U.S. passport, or military ID. Proof of death, such as certified copies of the death certificate. Documentation about the account and its owner, including the deceased's full legal name, Social Security number, and the bank account number.

If the account holder established someone as a beneficiary, the bank releases the funds to the named person once it learns of the account holder's death. After that, the financial institution typically closes the account. If the owner of the account didn't name a beneficiary, the process can be more complicated.

Family members or next of kin generally notify the bank when a client passes. It can also be someone who was appointed by a court to handle the deceased's financial affairs. There are also times when the bank learns of a client's passing through probate.

If there's a will without a named executor, the court will issue a Letter of Testamentary; if there's no will, the court will issue a Letter of Administration. Present either of these letters to the bank along with the death certificate to close the account.