This form is a sample letter in Word format covering the subject matter of the title of the form.

Letter Of Instruction To Bank After Death For Funeral In Pima

Category:

State:

Multi-State

County:

Pima

Control #:

US-0034LTR

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

The deceased person is likely to have ongoing standing orders and direct debits, so it's best to notify these organisations of the death as soon as possible to avoid receiving letters demanding outstanding payments.

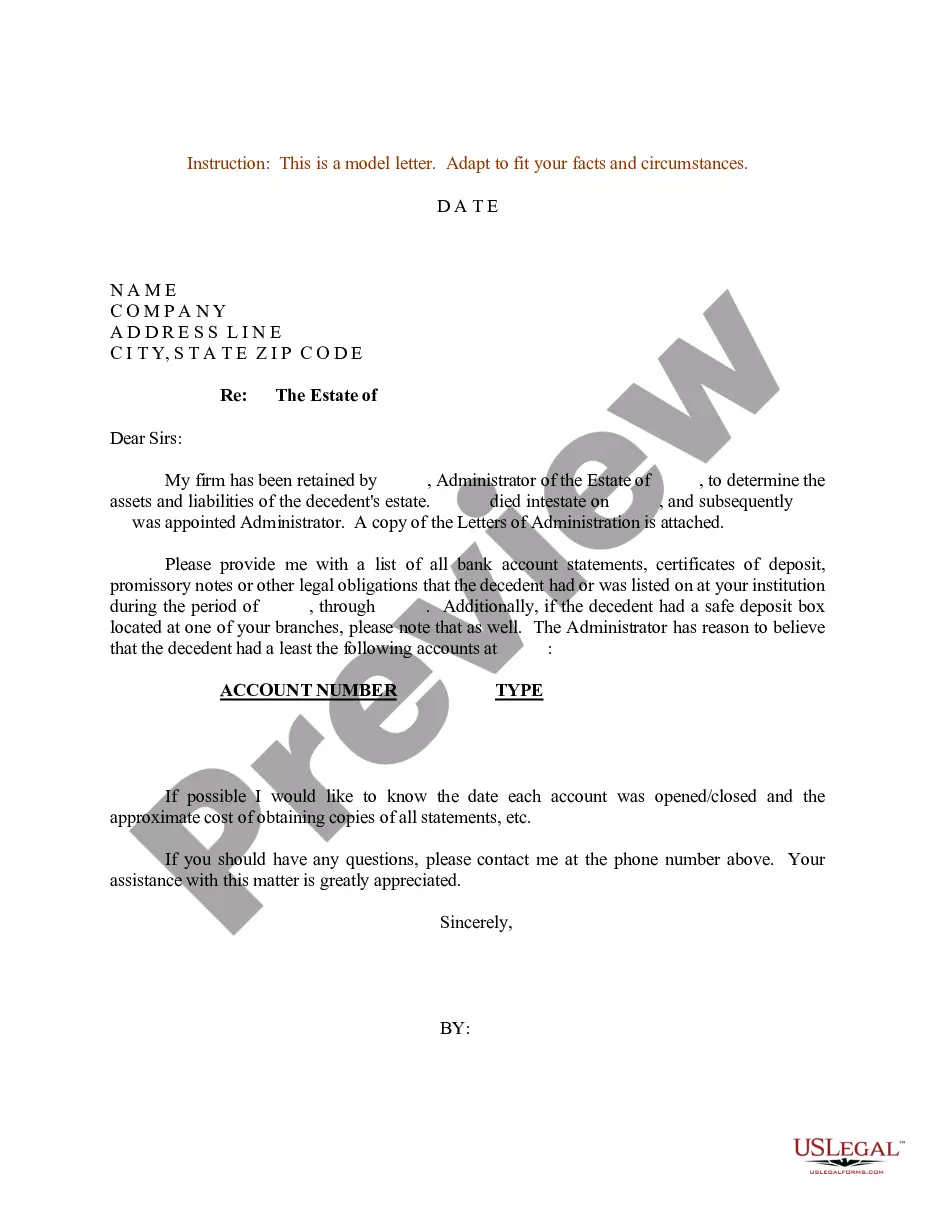

Family members or next of kin generally notify the bank when a client passes. It can also be someone who was appointed by a court to handle the deceased's financial affairs. There are also times when the bank learns of a client's passing through probate.

Your valid ID, such as a state-issued driver's license or ID card, U.S. passport, or military ID. Proof of death, such as certified copies of the death certificate. Documentation about the account and its owner, including the deceased's full legal name, Social Security number, and the bank account number.

To ensure that families dealing with the death of a family member have adequate time to review and restructure their accounts if necessary, the FDIC will insure the deceased owner's accounts as if he or she were still alive for six months after his or her death.

The bank needs to be notified of the accountholder's passing as soon as possible, as any bank accounts of the deceased remain active until the bank is notified of the death. This typically entails providing the original Death Certificate for verification purposes and the Will, if one is available.

The timeline is much shorter. California laws, for example, require that beneficiaries are notified within 60 days of the death.

After receiving notification of an account holder's death, a bank will take prompt steps to secure the assets. For an account owned by a single individual, this typically includes: Account status review: The bank reviews the account to confirm its ownership status and determine whether it has a beneficiary designation.

The next of kin must notify their banks of the death when an account holder dies. This is usually done by delivering a certified copy of the death certificate to the bank, along with the deceased's name and Social Security number, bank account numbers, and other information.

The bank is likely to ask for two forms of your identification (usually a passport or driver's licence, or a proof of address with a utility bill) and a copy of the will. If there's no will, the bank could ask for evidence of your relationship to the deceased. You'll also need the death certificate.