Donation Receipt Template For Nonprofits In Maricopa

Description

Form popularity

FAQ

In that case, all you need to provide in the donation receipt is the name and EIN of the organization, date of donation, and a description of the donated item. You should also add a note stating that the valuation of the item is the donor's income tax responsibility.

How to Reissue a Donation Receipt Open the Donation Record: Navigate to the donation record for which you need to reissue the receipt. Edit Personal Information. Modify the First Name. Restore the First Name. Download the Reissued Receipt:

However, you should be able to provide a bank record (bank statement, credit card statement, canceled check or a payroll deduction record) to claim the tax deduction. Written records, like check registers or personal notations, from the donor aren't enough proof. The records should show the: Organization's name.

In order to take a tax deduction for a charitable contribution to an IRS-qualified 501(c)(3) public charity, you'll need to forgo the standard deduction in favor of itemized deductions. That means you'll list out all of your deductions, expecting that they'll add up to more than the standard deduction.

Example 2: Individual Acknowledgment Letter Hi donor name, We're super grateful for your contribution of $250 to nonprofit's name on date received. As a thank you, we sent you a T-shirt with an estimated fair market value of $25 in exchange for your contribution.

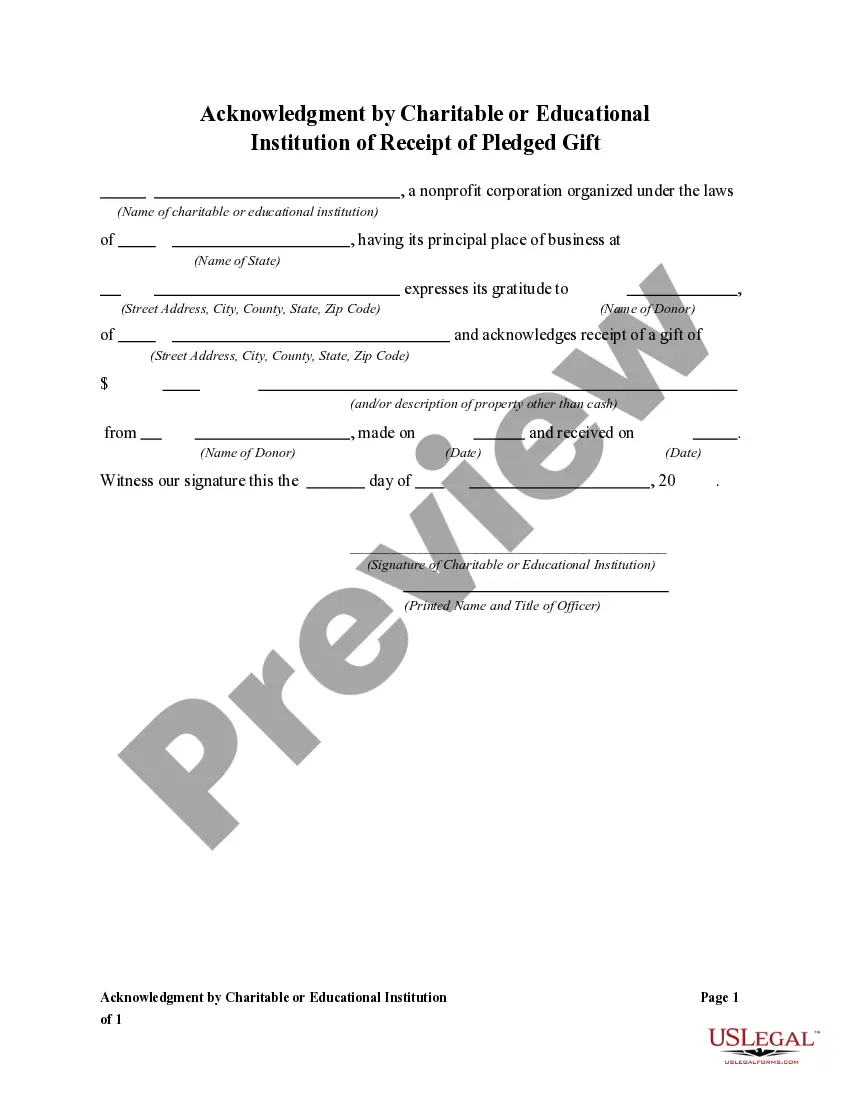

A donor can deduct a charitable contribution of $250 or more only if the donor has a written acknowledgment from the charitable organization. The donor must get the acknowledgement by the earlier of: The date the donor files the original return for the year the contribution is made, or.

The receipt can take a variety of written forms – letters, formal receipts, postcards, computer-generated forms, etc. It's important to remember that without a written acknowledgment, the donor cannot claim the tax deduction.

Charities are required to provide donors with receipts for charitable contributions over $250, which donors must have to substantiate their tax deductions.