Accounts Receivable Contract With Credit Card In Arizona

Description

Form popularity

FAQ

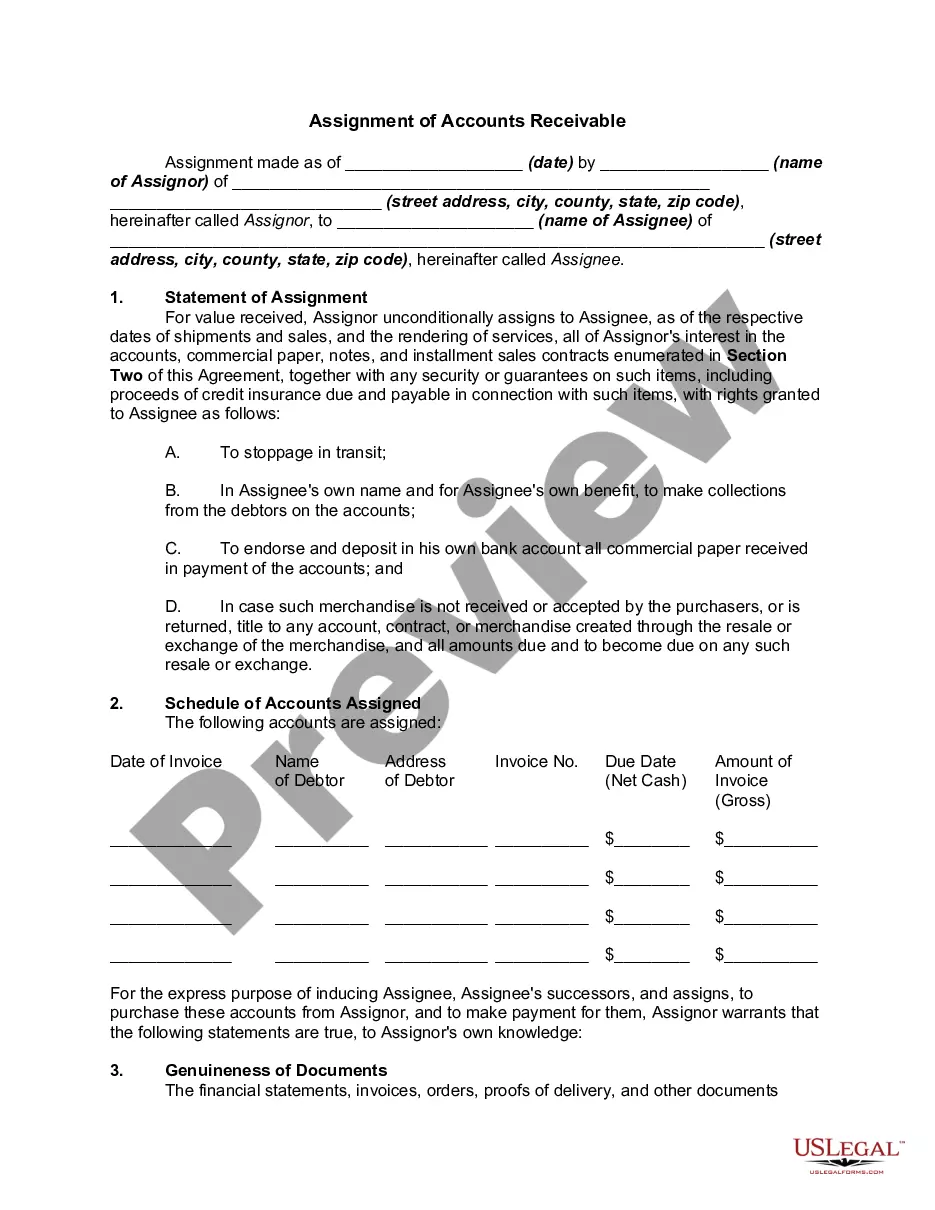

Therefore, when a journal entry is made for an accounts receivable transaction, the value of the sale will be recorded as a credit to sales. The amount that is receivable will be recorded as a debit to the assets. These entries balance each other out.

The 10-Step Accounts Receivable Process Develop a Credit Application Process. Create a Collection Plan. Compliance with Consumer Credit Laws. Send Out Invoices. Choose an Accounts Receivable Management System. Track the Collection Process. Log All Charges and Expenses in Real-time. Incentivize Early Payment Discounts.

The Accounts Receivable Process Explained Step 1: Receive Order. Step 2: Approve Credit. Step 3: Send Invoices. Step 4: Manage Collections. Step 5: Address Disputes. Step 6: Write off Uncollectible Debt. Step 7: Process Payments. Step 8: Handle Reporting.

Every transaction done on credit has to have an element of both accounts payable and accounts receivable. In this case, since Company A sells on credit to Company B, they are considered the “creditor” and Company B is the “debtor.” This means, in every transaction, there is always AP and AR involved.

Discussion. All DoD guidance and regulations indicate that sales of merchandise or services to an authorized customer using a credit card should be recorded as a receivable.

Accounts receivable is a debit, which is an amount that is owed to the business by an individual or entity.

Set Up Credit Cards In the Chart of Accounts: Create Liability accounts for each credit card you use. Add an Expense account for credit card interest & fees. Enter Beginning Balances for each credit card. Create a Journal called “Credit Cards” or you may prefer to have a separate journal for each card.

All DoD guidance and regulations indicate that sales of merchandise or services to an authorized customer using a credit card should be recorded as a receivable.

When categorizing credit card payments: Ensure payments are categorized as transfers to the credit card liability account, not as expenses.