Form 8594 With The Irs In Chicago

Category:

State:

Multi-State

City:

Chicago

Control #:

US-00418

Format:

Word;

Rich Text

Instant download

Description

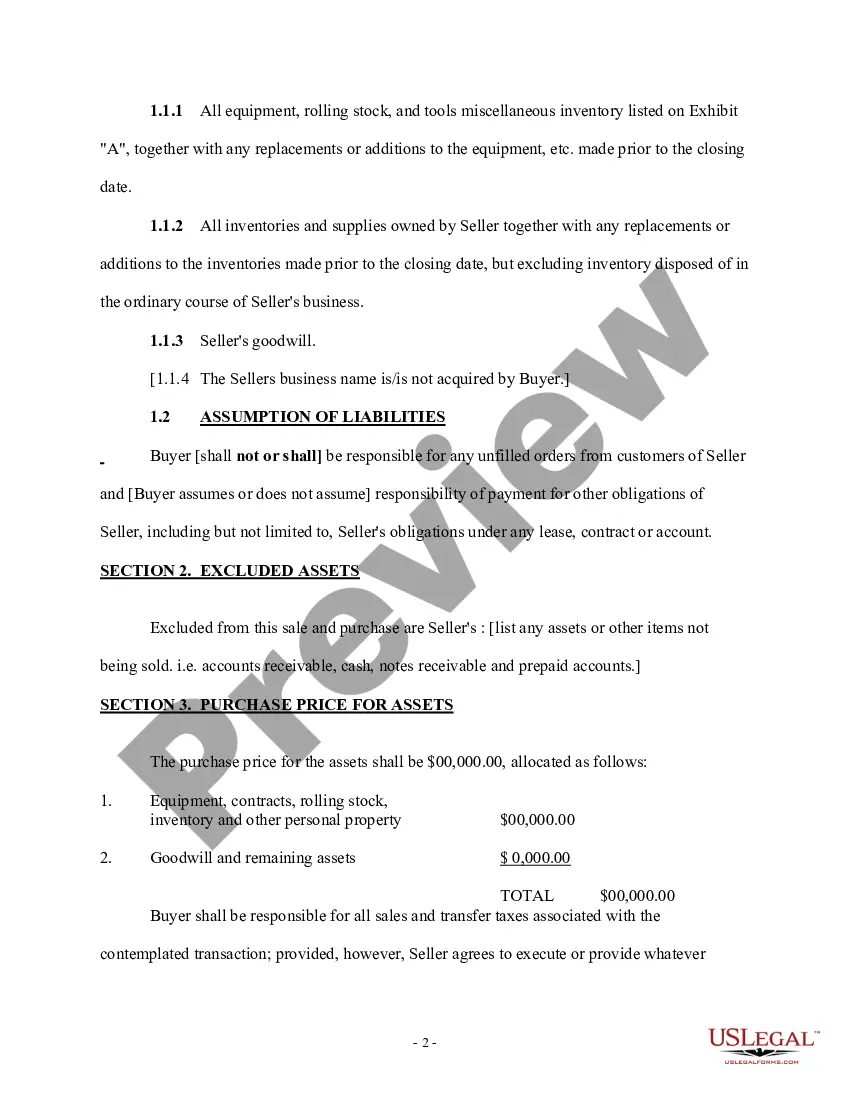

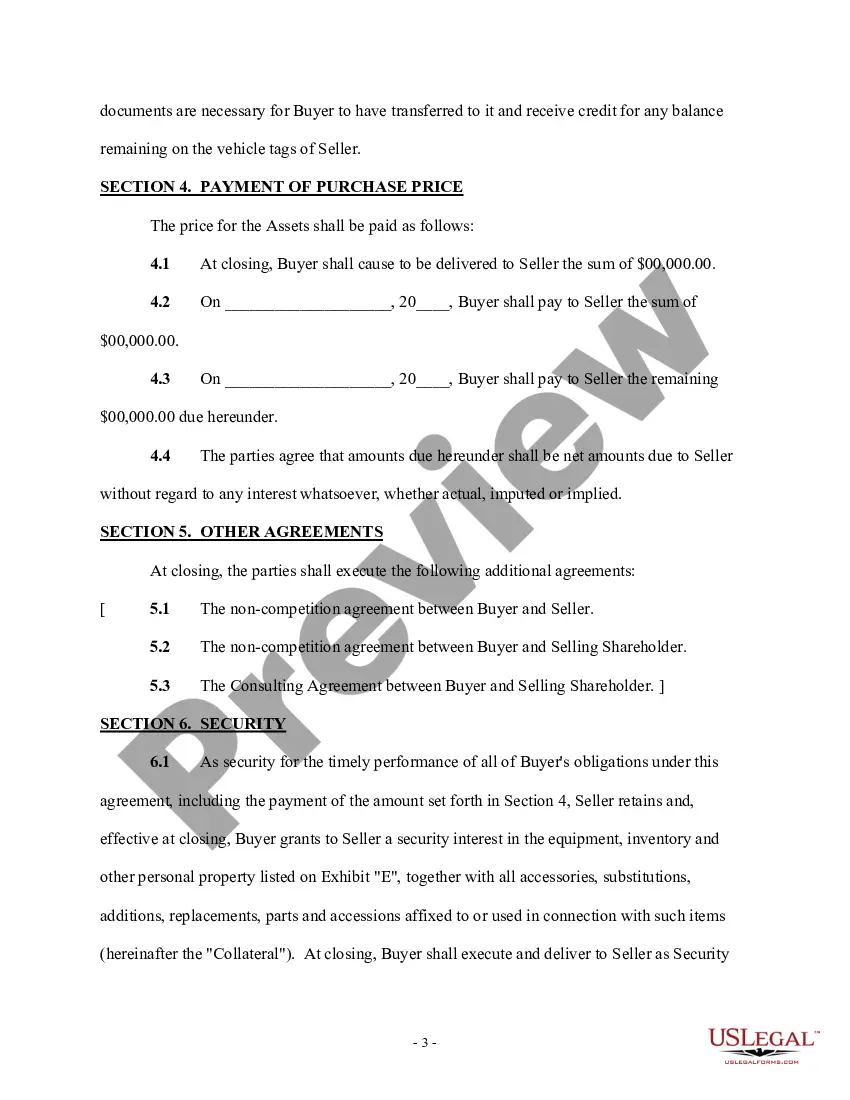

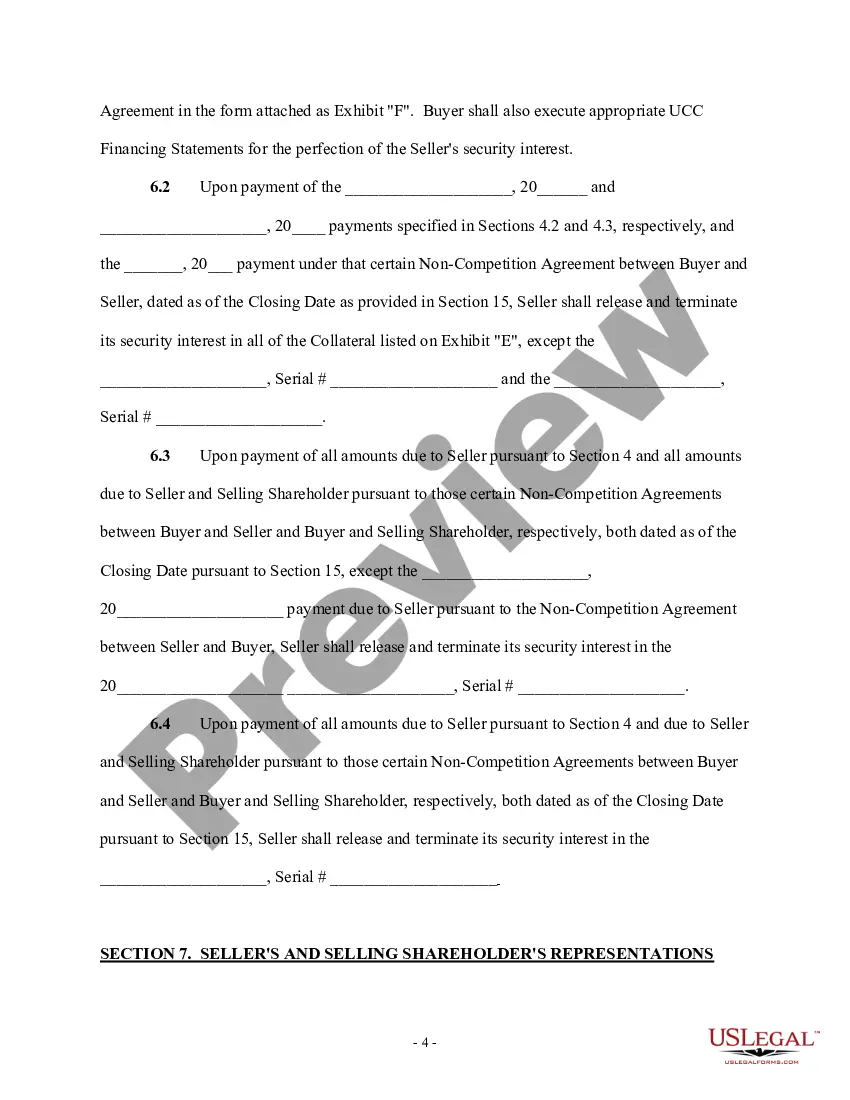

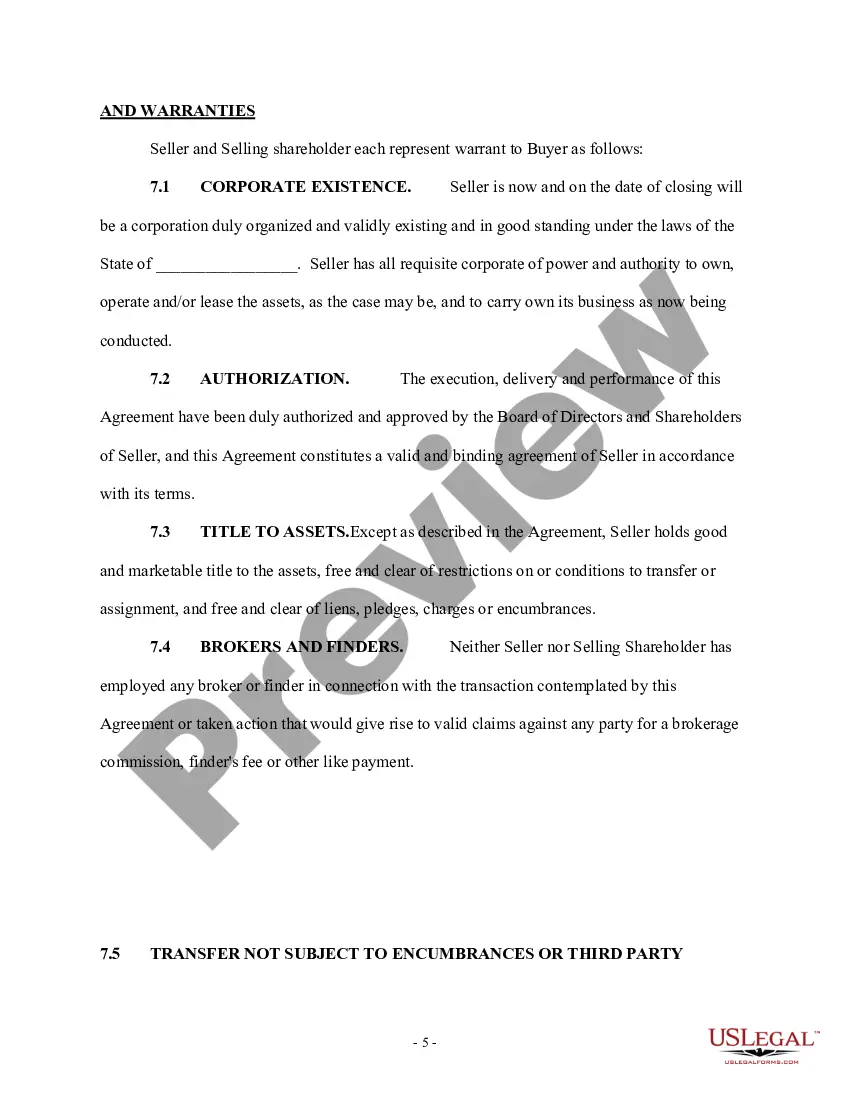

This form is an Asset Purchase Agreement. The buyer agrees to purchase from the seller certain assets which are listed in the agreement. The form also provides a listing of certain assets which will be excluded from the sale. The form must be signed in the presence of a notary public.

Free preview