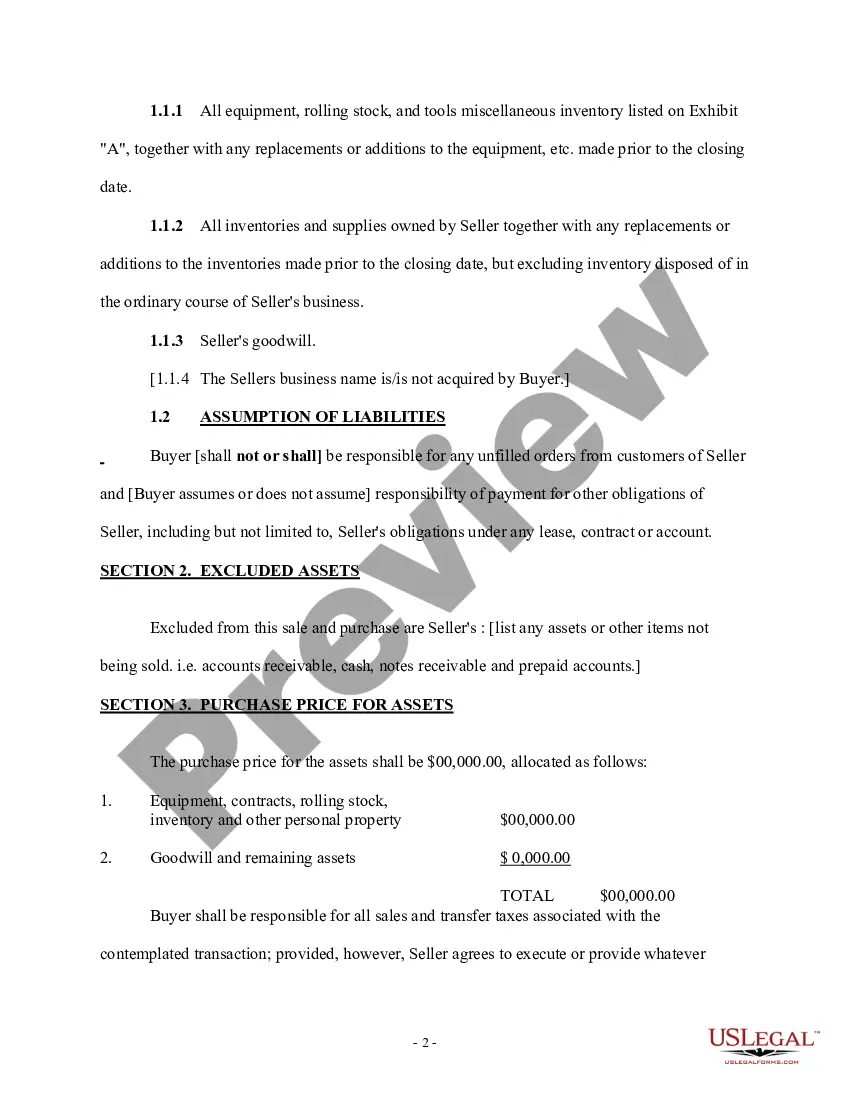

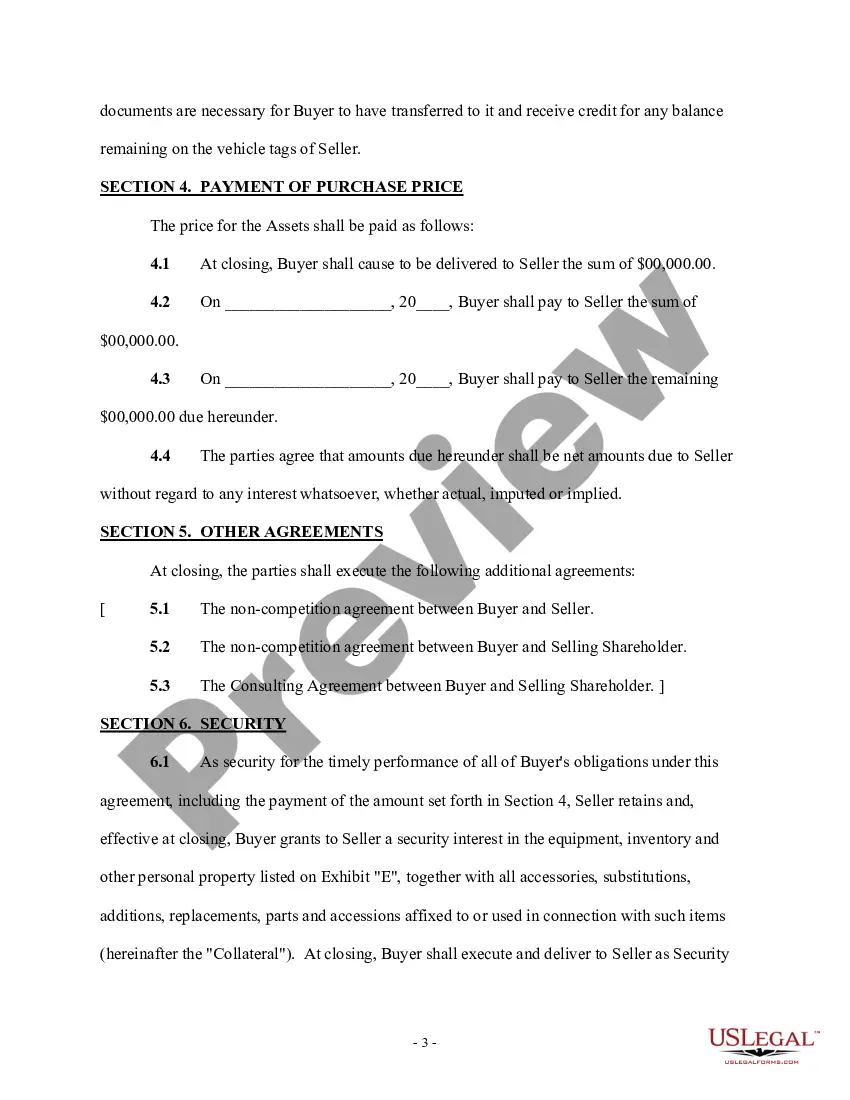

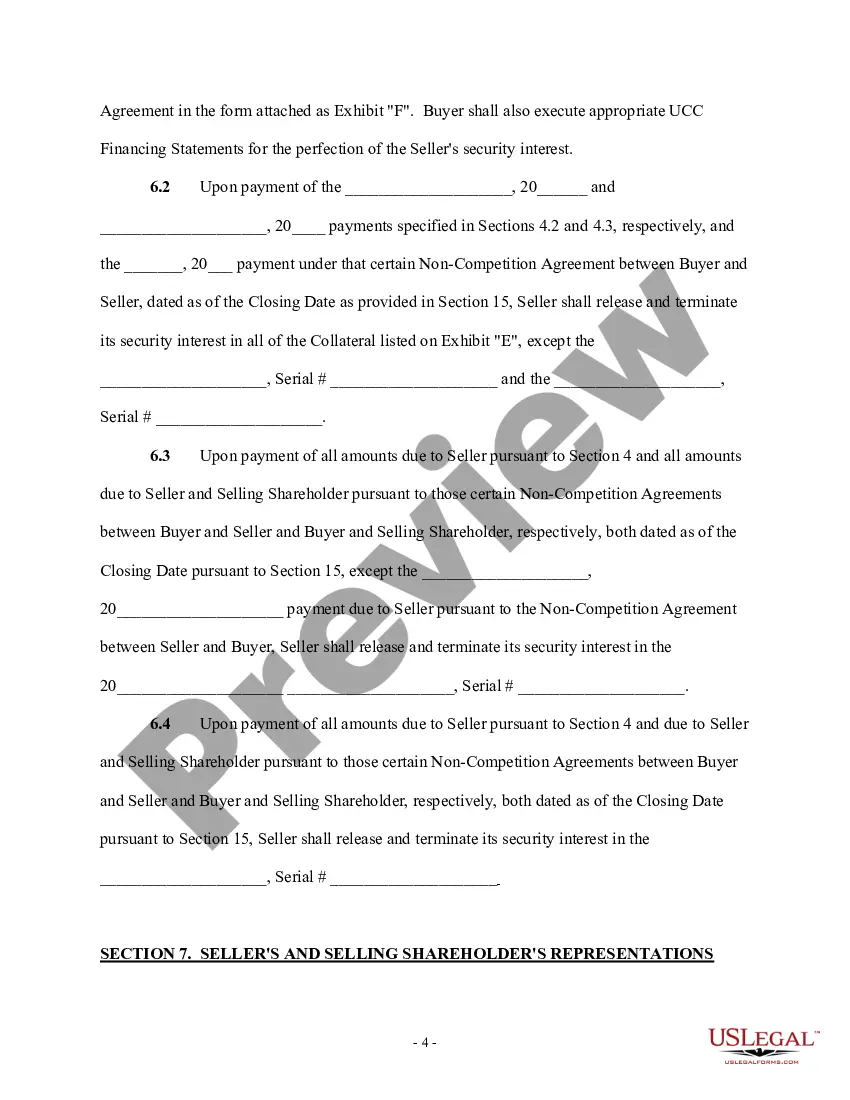

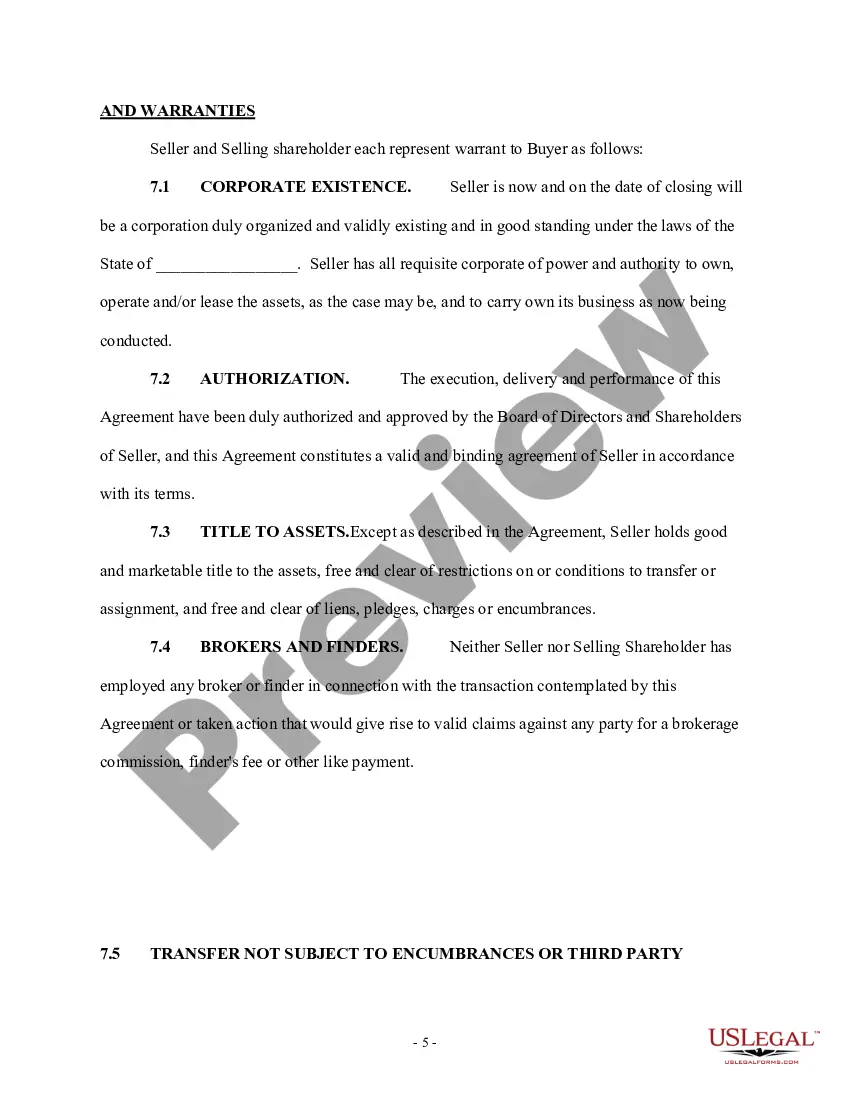

This form is an Asset Purchase Agreement. The buyer agrees to purchase from the seller certain assets which are listed in the agreement. The form also provides a listing of certain assets which will be excluded from the sale. The form must be signed in the presence of a notary public.

Form 8594 Foreign Buyer In Maryland

Category:

State:

Multi-State

Control #:

US-00418

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

A penalty may be imposed for failure to file Form 8804 when due (including extensions). The penalty for not filing Form 8804 when due is usually 5% of the unpaid tax for each month or part of a month the return is late, but not more than 25% of the unpaid tax.

Sellers usually prefer to allocate as much as possible to capital gain assets and intangibles rather than ordinary income assets, whereas buyers typically want to allocate to assets they can depreciate rapidly. Therefore, the allocation is often a negotiated component of a sales agreement.

More info

Generally, both the purchaser and seller must file Form 8594 and attach it to their income tax returns (Forms 1040, 1041,. A taxable asset purchase allows the buyer to "step up," or increase, the tax basis of the acquired assets to reflect the purchase price.Today's goal is to help you understand the importance of IRS Tax Form 8594 in preparing for sale of your business to a third party… Learn how to file form 8594 and when to file. We offer several ways for you to obtain Maryland tax forms, booklets and instructions. You can also file your Maryland return electronically online.