Charitable Remainder Trust With Real Estate

Description

Form popularity

FAQ

Yes, a trust can invest in real estate, which may provide significant advantages for the beneficiaries. By incorporating real estate into a Charitable Remainder Trust, you can create a sustainable income stream while simultaneously supporting charitable causes. This strategy not only preserves the property's value but also allows for potential tax benefits. For assistance in structuring this investment, consider using uslegalforms to simplify the legal requirements.

A Charitable Remainder Trust can invest in a variety of assets, including stocks, bonds, mutual funds, and real estate. This diverse investment spectrum allows the trust to generate income for beneficiaries while fulfilling charitable goals. When you consider setting up a CRT with real estate, the property can effectively appreciate over time, contributing to the overall value of the trust. Utilizing platforms like uslegalforms can streamline the setup process and ensure compliance with investment regulations.

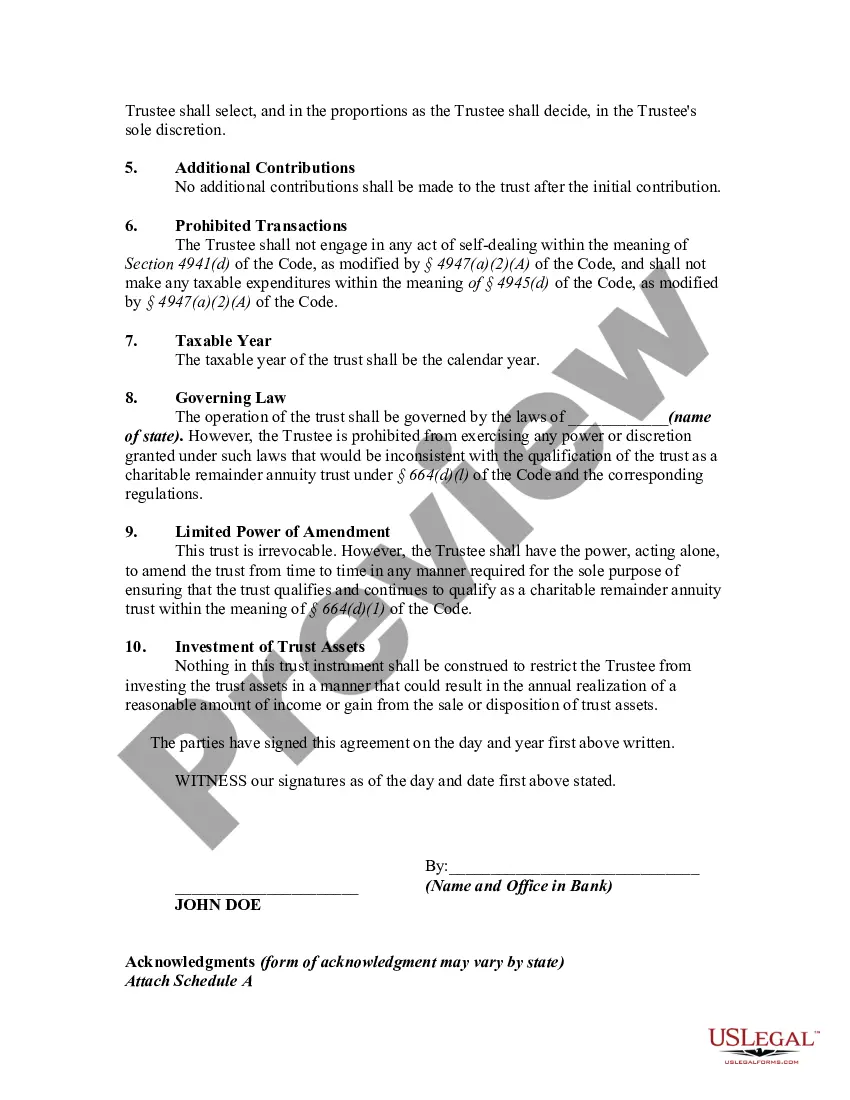

The 5% rule in a Charitable Remainder Trust refers to the requirement that the trust must distribute at least 5% of its assets annually. This rule ensures that there is a reasonable payout to beneficiaries over the trust's term. By adhering to this requirement, you maximize the advantages of setting up a CRT with real estate, balancing immediate income needs with charitable intentions. Understanding this rule helps in effective financial planning.

A Charitable Remainder Trust (CRT) is generally not subject to estate tax during the owner’s lifetime. When you set up this type of trust with real estate, it removes the asset from your estate, which can help minimize tax liabilities. Consequently, the beneficiaries of the trust can potentially receive greater financial benefits. Consulting with a tax professional can provide personalized insights into your specific situation.

A charitable remainder trust generally is not included in your taxable estate. This is beneficial for individuals looking to reduce their estate tax liability. However, any income generated by the trust could have tax implications. Consulting with professionals, like those at uslegalforms, can provide more guidance on how a charitable remainder trust with real estate fits into your estate planning.

Absolutely, a charitable trust can own real estate. This arrangement can leverage investment properties to generate income for the trust while supporting charitable causes. As you consider this option, remember that proper management and alignment with your charitable goals will enhance the overall effectiveness of holding real estate within the trust.

Yes, a Charitable Remainder Unitrust can hold real estate, making it an attractive option for many donors. This allows you to contribute appreciated property while potentially avoiding capital gains taxes. However, ensure the property is managed properly to generate income for beneficiaries and fulfill the charitable intent of the trust.

A Charitable Remainder Unitrust (CRUT) primarily focuses on investments that generate income for its beneficiaries. The IRS imposes certain restrictions, such as not allowing investments in life insurance or collectibles. Importantly, keep in mind that any investment should align with the goal of benefiting both the trust and the designated charity. Understanding these guidelines helps maximize the potential of your CRUT with real estate assets.

A Charitable Remainder Trust with real estate is generally not included in your estate for estate tax purposes. This is because you effectively give up ownership of the assets in the trust. However, the income generated from the trust may still be subject to certain tax implications, so it’s wise to consult a tax professional for personalized advice.

While a Charitable Remainder Trust (CRT) with real estate can offer tax benefits, there are some downsides. One major consideration is the irrevocable nature of the trust, meaning you cannot change it once established. Additionally, the trust may incur administrative costs and fees that could outweigh the tax advantages. It's essential to weigh these factors against your financial goals.