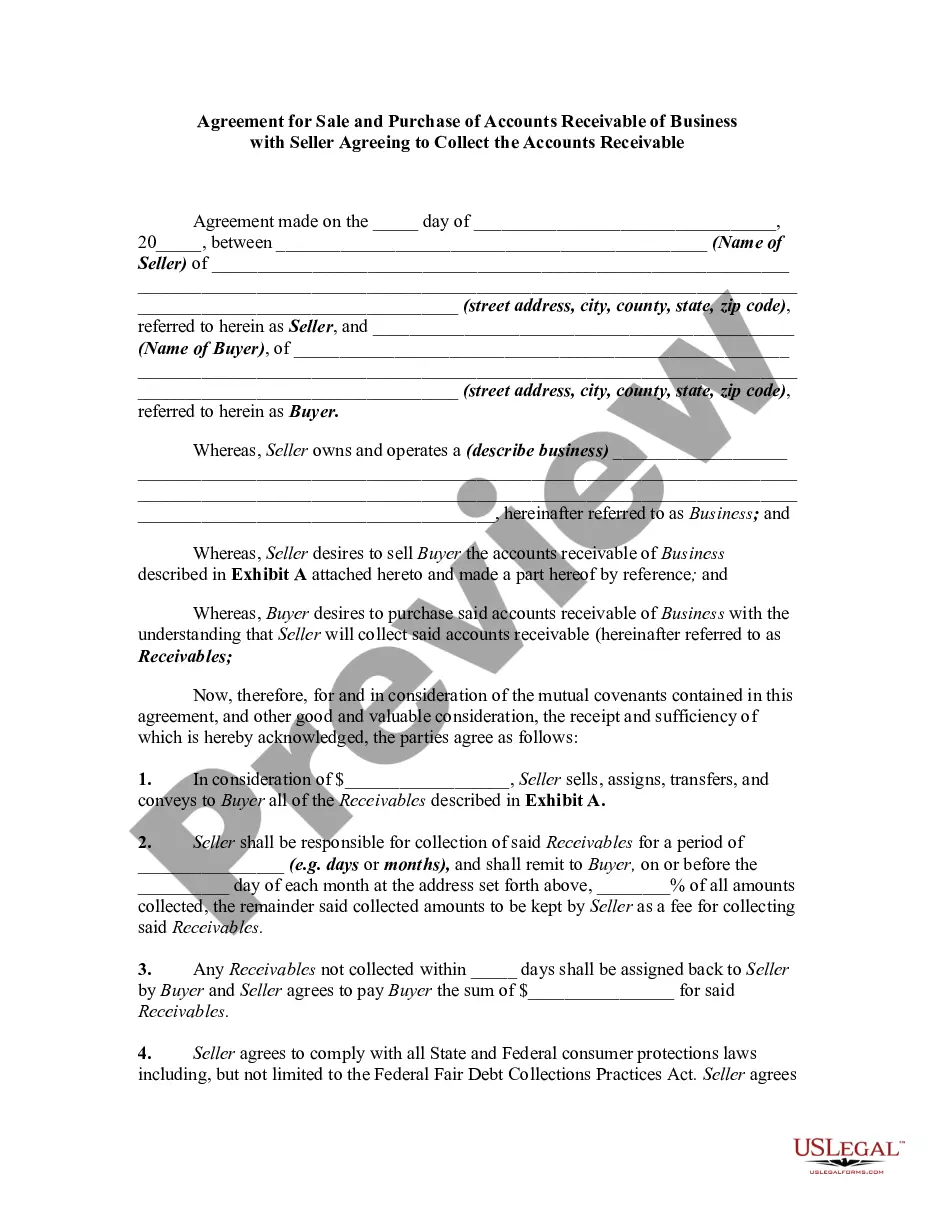

With regard to the collection part of this form agreement, the Federal Fair Debt Collection Practices Act prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representations are forbidden, such as representing that the debt collector is associated with the state or federal government, stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

Agreement Of Purchase And Sale Form

Category:

State:

Multi-State

Control #:

US-01280BG

Format:

Word;

Rich Text

Instant download

Description Agreement Purchase Business Document

Free preview Receivable Purchase Agreement

How to fill out Sell Collect Accounts?

How to get professional legal forms compliant with your state regulations and prepare the Agreement Of Purchase And Sale Form without applying to an attorney? Many services on the web provide templates to cover different legal occasions and formalities. Nonetheless, it may take time to find out which of the available samples satisfy both use case and juridical requirements for you. US Legal Forms is a trustworthy service that helps you locate formal papers composed according to the most recent state law updates and save money on juridical assistance.

US Legal Forms is not a regular web catalog. It's a collection of more than 85k verified templates for different business and life situations. All papers are organized by field and state to make your search process faster and more hassle-free. Additionally, it integrates with robust tools for PDF editing and electronic signature, enabling users with a Premium subscription to quickly complete their paperwork online.

It takes minimum effort and time to get the required paperwork. If you already have an account, log in and make sure your subscription is active. Download the Agreement Of Purchase And Sale Form using the related button next to the file name. If you don't have an account with US Legal Forms, then follow the guide below:

- Go over the web page you've opened and check if the form suits your needs.

- To do this, use the form description and preview options if available.

- Search for another sample in the header providing your state if needed.

- Click the Buy Now button once you find the appropriate document.

- Pick the best suitable pricing plan, then log in or pregister for an account.

- Opt for the payment method (by credit card or via PayPal).

- Change the file format for your Agreement Of Purchase And Sale Form and click Download.

The acquired templates remain in your possession: you can always get back to them in the My Forms tab of your profile. Subscribe to our platform and prepare legal documents by yourself like an experienced legal specialist!